A Policy that Expired 1 Day Before an Incident Occurred

A real estate company in Houston, Texas had an insurance policy that covered burglary. However, the policy ended on March 27th and was not promptly renewed. On March 28th, a large-scale burglary occurred on the property. Due to the fact that the insurance policy expired the previous day and was not renewed in time, the insurance company has no obligation to cover this claim.

Key Takeaway: It can be easy to overlook or forget about an expiring insurance policy, but any lapse of time in coverage creates a tremendous amount of risk. As seen from this incident, it’s imperative for insurance policies to be renewed on-time.

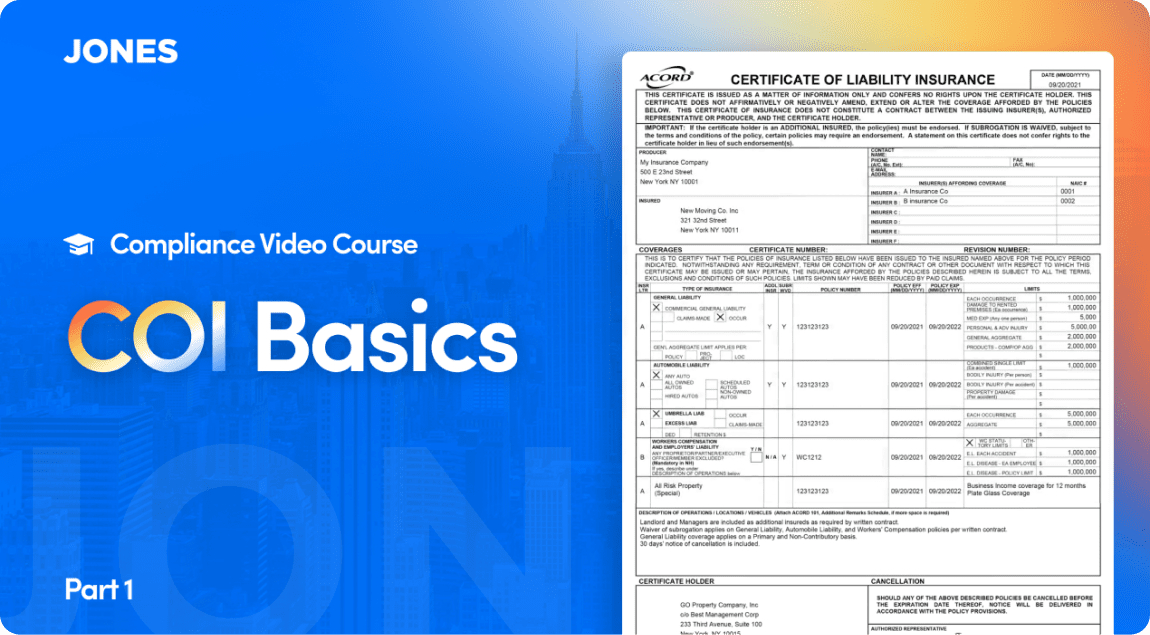

This is where the expiration date of a policy can be found on a COI

Incorrect Additional Insured Listed on a Policy

A Colorado-based property management company was seeking coverage for an incident, but cannot do so because it was never listed as the insured party on the professional liability policy. A similar name was listed, but the exact name of the property management company was not listed. Because of this, the insurance company does not need to cover the claim.

Key Takeaway: It’s very important to make sure the correct names are listed as additional insured on all policies. If this is overlooked, the company may not be covered by the policy. You can learn more about the “Additional Insured” term here in Part 3 of the Jones Compliance Course.

This is the most common place to find the ‘additional insured’ on a COI

A Policy that Does Not Protect a Contractor From a Claim

A contractor in Georgia was sued by a real estate company for $250,000 due to issues arising from their work. The contractor was hired to repair and replace stucco on many buildings within a portfolio. They created widespread hairline cracks in the stucco, applied failed sealants, and created multiple fit and finish issues. The contractor’s insurance provider told the Georgia federal court that it has no duty to cover this claim because the commercial general liability policy it issued contained multiple exclusions barring coverage for property damage arising out of its work. The real estate company who hired the contractor for this work may be stuck with the burden of paying the hefty bill to repair these damages.

Key Takeaway: It’s very important to understand the exact language and coverage amounts of the insurance policies that all contractors and vendors have.

The damage from the contractor may not be covered by their general liability policy

Being proactive instead of reactive with COI management would have saved all of these companies a large amount of time, stress, and most importantly: money.

Through advanced compliance dashboards, AI driven auditing, and COI workflow automation, Jones could have helped prevent each of these incidents.

Ready to protect your company from risk and completely automate your COI management process?

Fill out the form below to get started!