Mistake 1: Endorsements ≠ Provisions

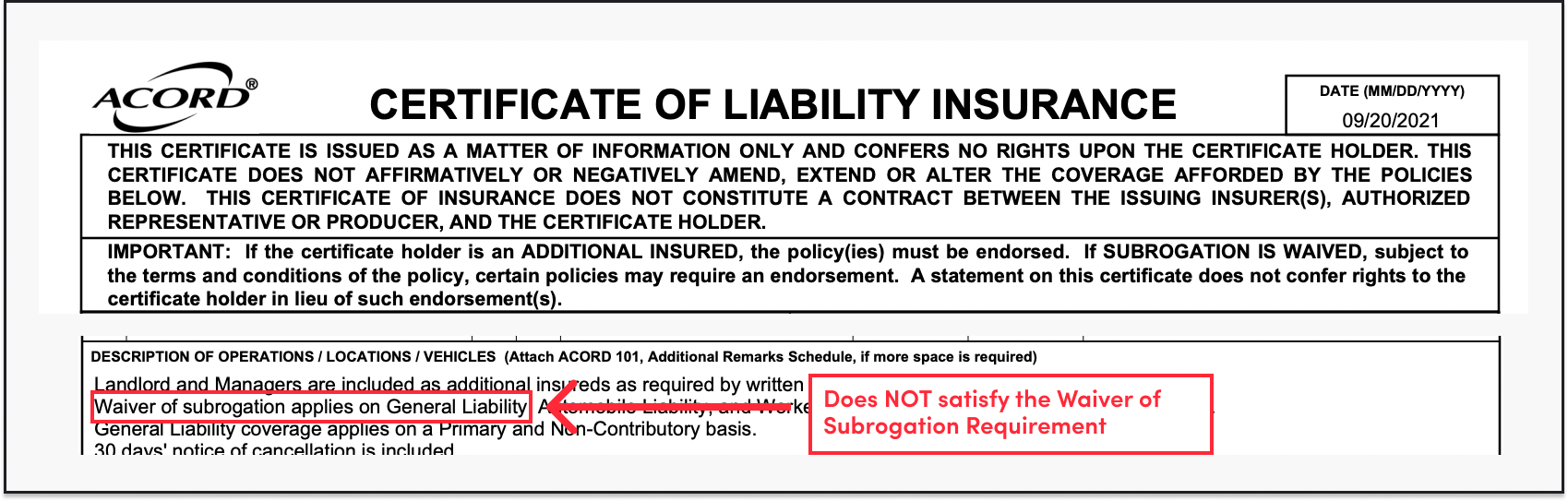

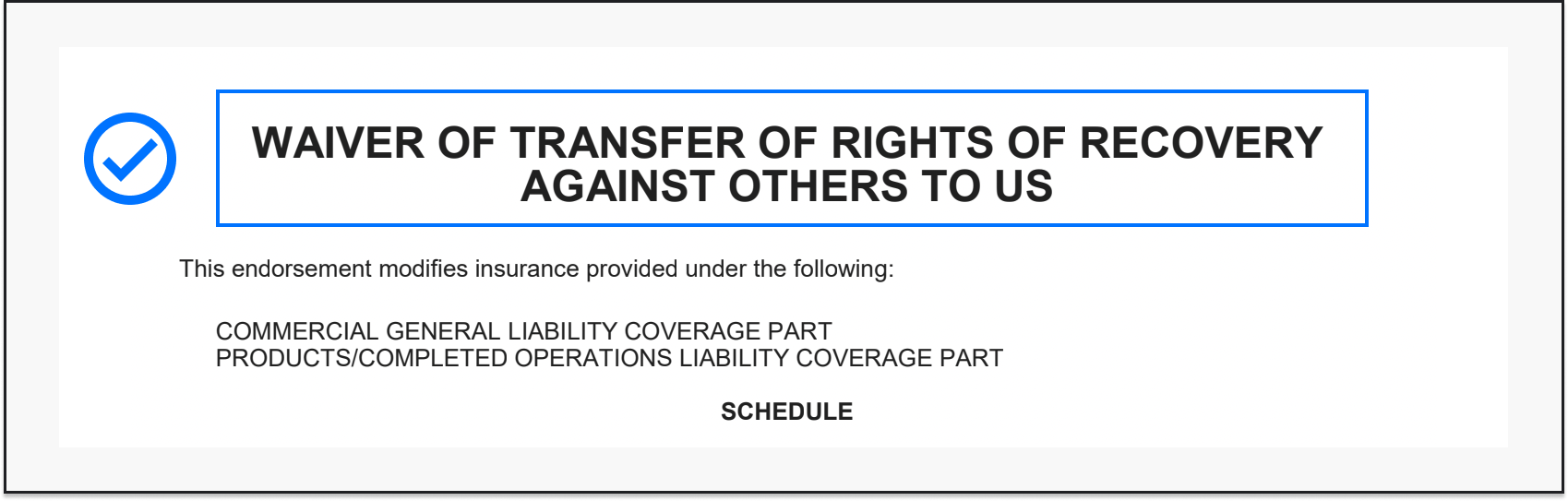

Scenario: Your building requires a Waiver of Subrogation endorsement.

❌ Don’t: Search for it in a COI document.

✅ Do: Look for a separate page that references a Waiver of Subrogation.

Even if the check box for waiver of subrogation is checked and the description of operations says “Waiver of Subrogation,” if an endorsement document is required, this will not suffice. The same rule applies to any kind of endorsement. Noting this on a COI is not enough, search for a separate endorsement document.

Mistake 2: Workers’ Compensation ≠ Employer’s Liability

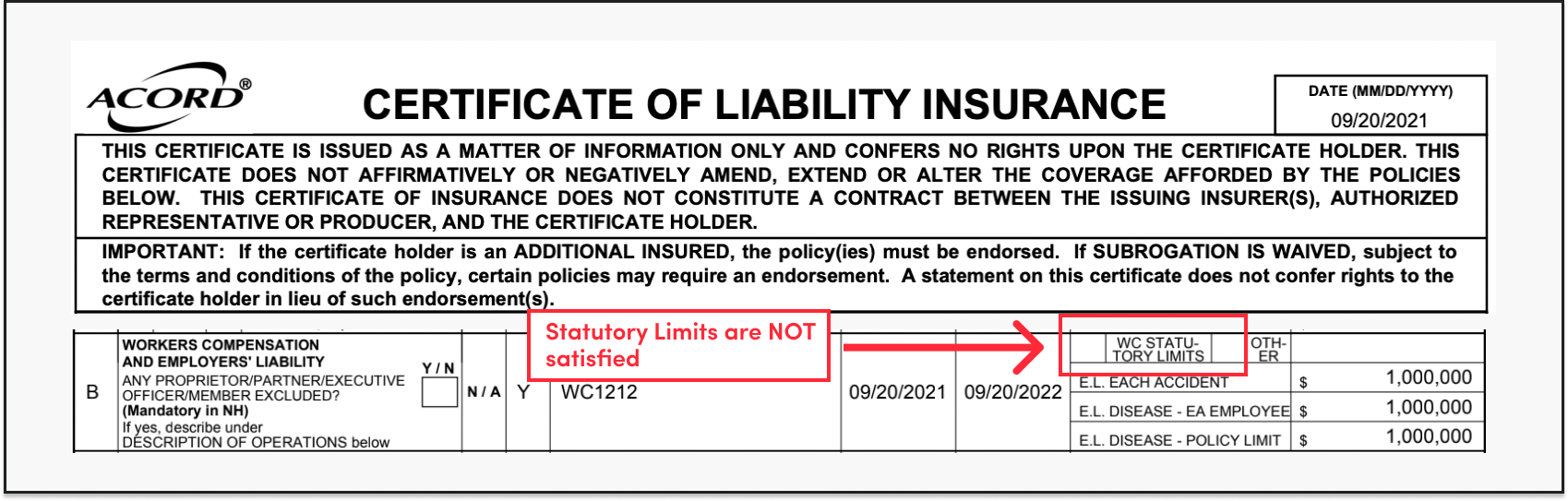

Scenario: the Employer’s Liability limits meet the required limits for Employer’s Liability.

❌ Don’t: Accept this as satisfying the required limits for Workers’ Compensation.

✅ Do: Check if the “Per statute” checkbox is marked above the Employer’s Liability limits on the COI.

While Employer’s Liability and Workers’ Compensation often come bundled together, they are two separate kinds of insurance that serve different purposes and have different limits.

Workers’ comp is a no-fault kind of insurance, which means that you as an employer, do not need to be liable for the policy to be paid out. If an employee gets injured, Workers’ comp will pay their medical bills and their lost wages, no questions asked.

The employer’s liability is fault dependent. You have to be liable for employer’s liability to kick in.

If you look at a COI, you will see three limits in the Workers’ compensation row that refer only to the employer’s liability. Meanwhile, there’s a checkbox for Workers’ compensation.

This checkbox indicates whether the Workers’ compensation limits meet the requirements of the state.

Insurance requirements will often specify limits that are required for employer’s liability, as well as per statute limits. Both requirements need to be met. One does not satisfy the other.

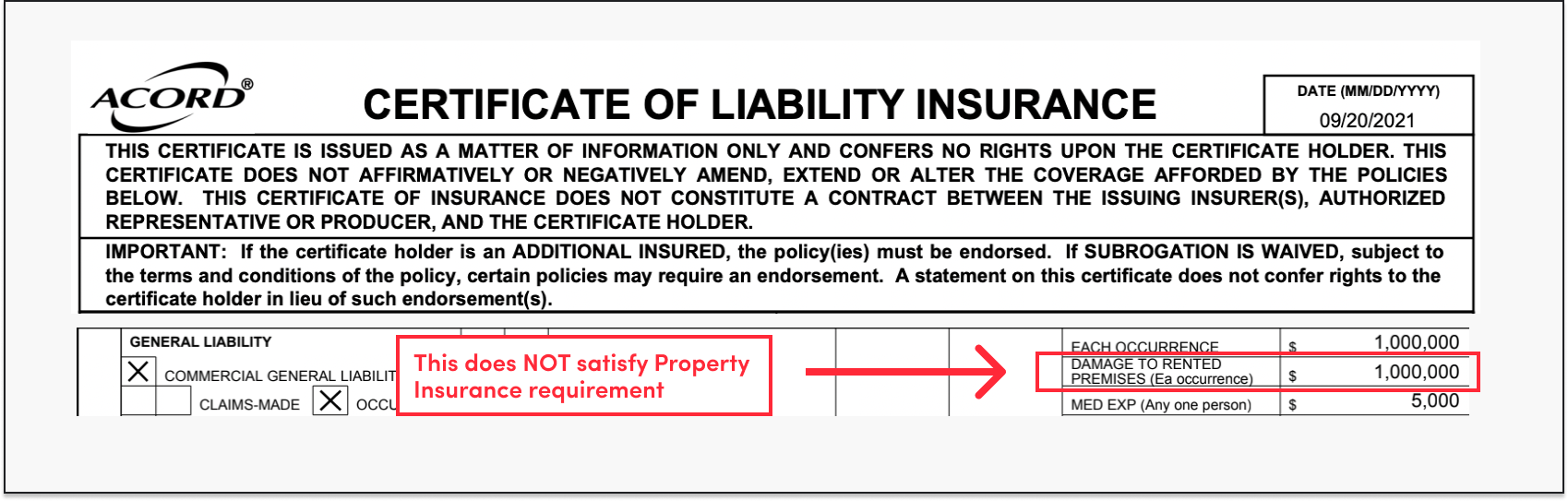

Mistake 3: General Liability ≠ Property Insurance

Scenario: Your building requires Property Insurance

❌ Don’t: Use any limit of General Liability to satisfy the Property Insurance requirement. Sometimes, we see property managers accepting the “damage to rented premises” limit in the General Liability row in lieu of Property Insurance. Don’t do this.

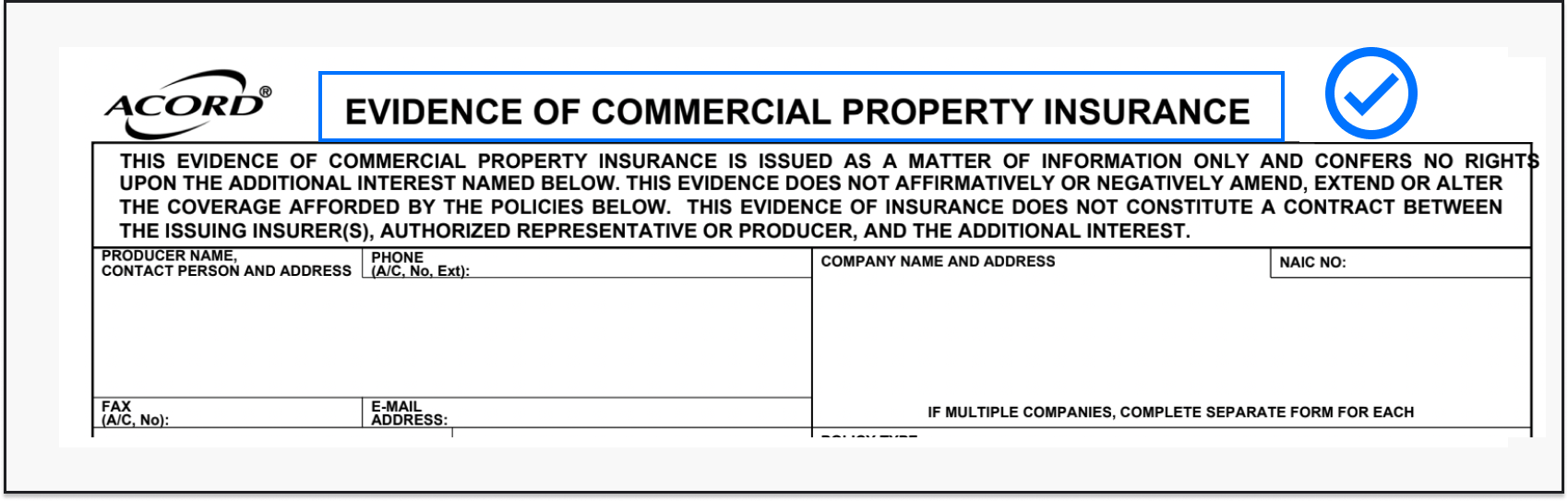

✅ Do: Look for Property Insurance on the bottom miscellaneous row of an Accord 25 where free text is written or on a separate COI specifically dedicated to property insurance.

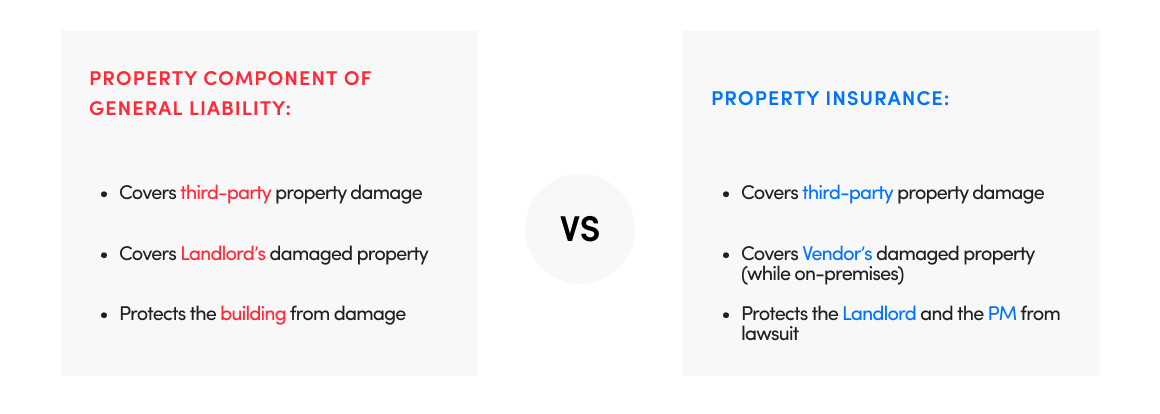

Here is why tenants and vendors need to have property insurance and why general liability doesn’t work in this case.

General liability, indeed, covers property damage—but only third-party property damage. For example, if a vendor accidentally damages a landlord’s property, the landlord is protected from loss.

However, if a vendor’s property ends up damaged while in the building, it would NOT be covered by General Liability, which, in turn, may result in a lawsuit against the landlord and property managers.

To avoid this, buildings often require first-party protection – which is a separate coverage referred to as Property Insurance. This will cover damages to tenants’ or vendors’ own property while on-premises.