We’ve found that it’s because a lot of PMs don’t understand the reason for certain insurance requirements. In this edition of the Jones Insurance Insider, we’ll bust a few myths so you can understand what your insurance requirements are (and aren’t) doing for your company.

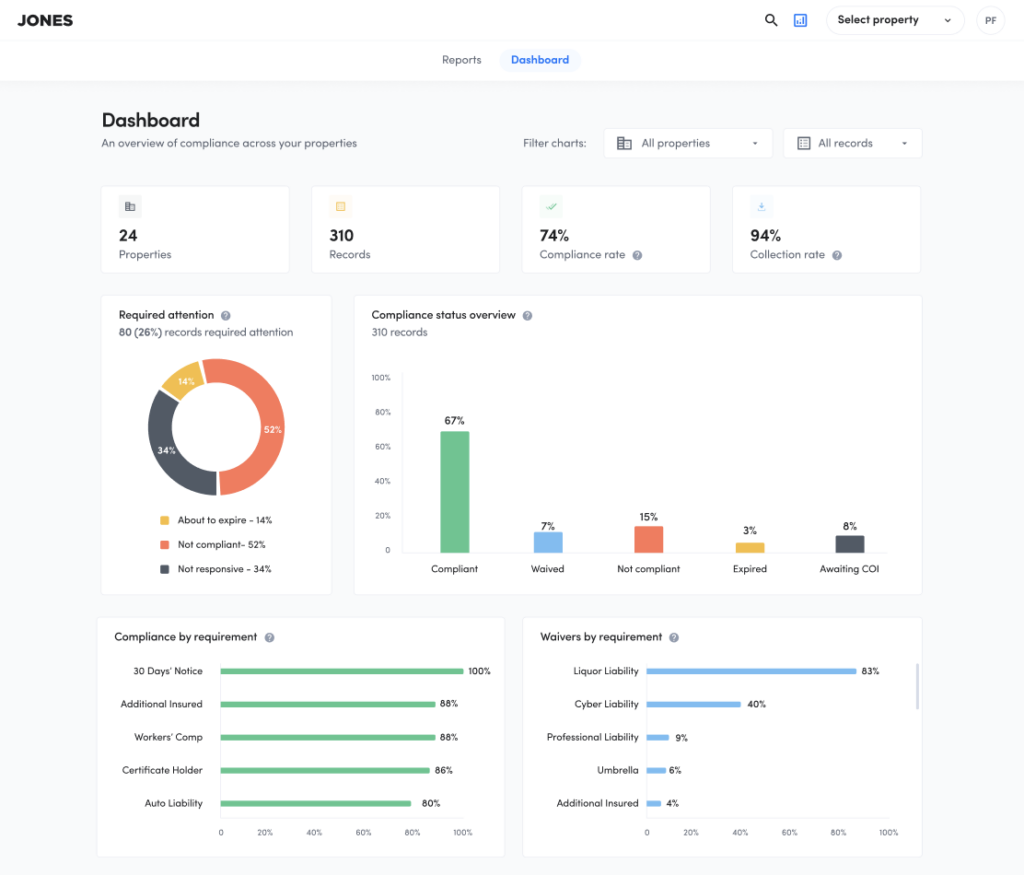

One West Coast based full-service real estate company enhanced their insurance compliance program by bringing Jones on to manage the collection and review of their vendor and tenant insurance documents. Collection rates were up, compliance data was available for review in one centralized platform, and members of the property management team were spending far less time managing insurance documentation. However, three items were still being flagged as non-compliant on more than 40 percent of total vendor and tenant COIs: Certificate Holder name, 30 Days’ Notice of Cancellation, and Additional Insured status.

Luckily, the Jones Risk and Compliance team is available in situations like this for insurance risk strategy sessions, where they offer suggestions for improving compliance rates based on Jones data and best practices. Let’s follow Jessica Lopes, Director of the Risk and Compliance team, as she diagnoses the issues facing this portfolio.

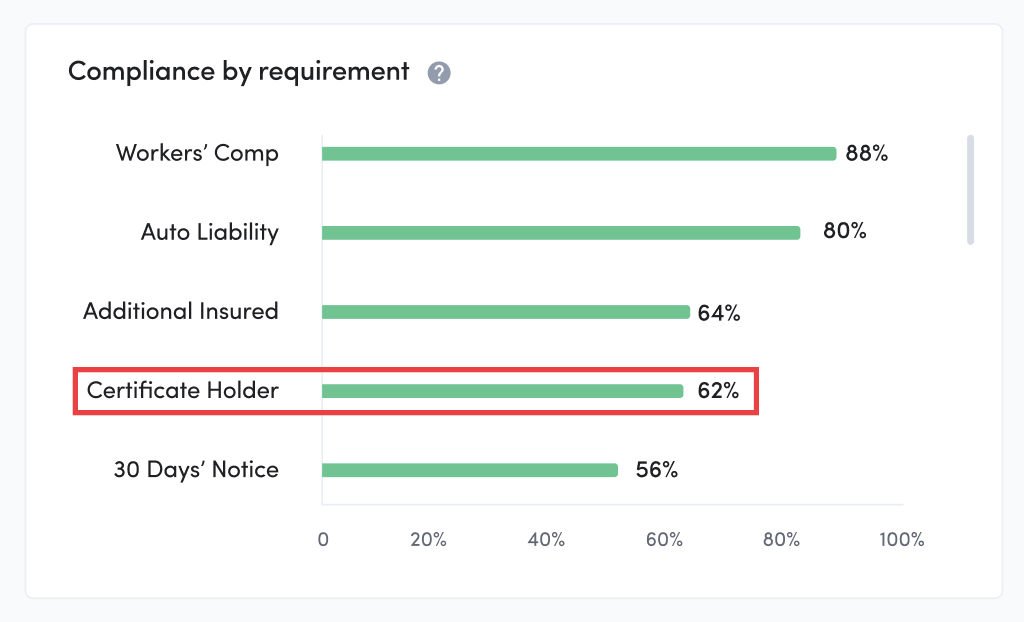

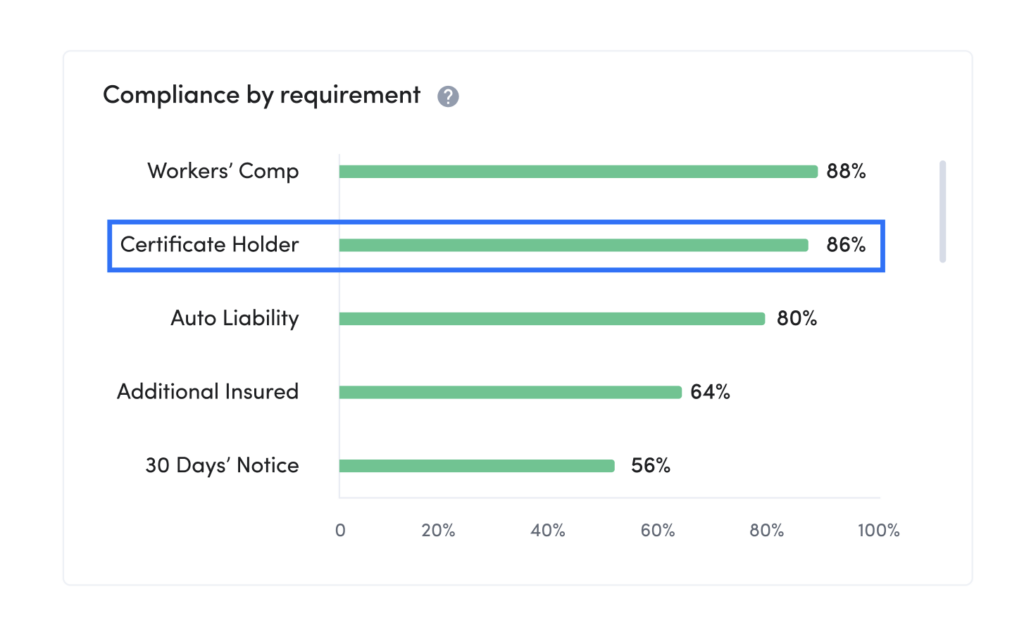

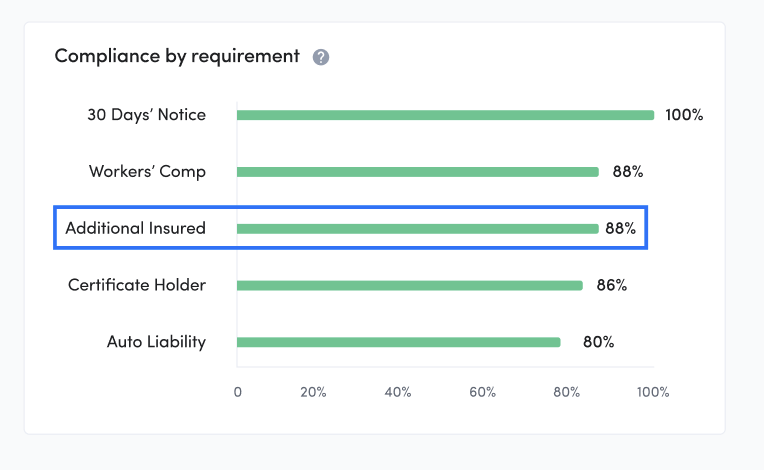

How Their Initial Portfolio Compliance Looked

After reviewing their overall compliance numbers, Jessica next drilled down into the specific causes for noncompliance for Certificate Holder, 30 Days’ Notice, and AI. Here’s what she found.

Issue #1: Lots of Errors in Certificate Holder Name

Jessica noticed that most of the Certificate Holder gaps were small typographical errors or omissions. Some of the Certificate Holder names were missing the “LLC” at the end of the property management company’s name, while others were missing a floor number or suite number. Others listed the name of an individual property manager rather than the management company itself. The property management team was very strict when it came to marking these mistakes, thinking Certificate Holder status was very important to protect them from risk.

Myth Busted: Having Certificate Holder status does NOT protect you

Many property managers are under the impression that being listed as a Certificate Holder in some way helps them transfer risk, or grants them coverage under the policies on the COI. This is not the case. Listing a Certificate Holder is an administrative formality without legal implications. It even says so right on top of the standard ACORD 25 form!

![]()

Suggestion: Change CH Name to Jones

Jessica suggested changing the Certificate Holder name to Jones.

By switching the Certificate Holder to Jones (who were already collecting and reviewing their COIs) the property management company removed the unnecessary administrative burden of chasing down incorrect Certificate Holder names, eliminating another barrier to insurance compliance. Now, vendors and tenants, regardless of what property they are in from the portfolio, only have to list the same Jones name and address for all their COIs.

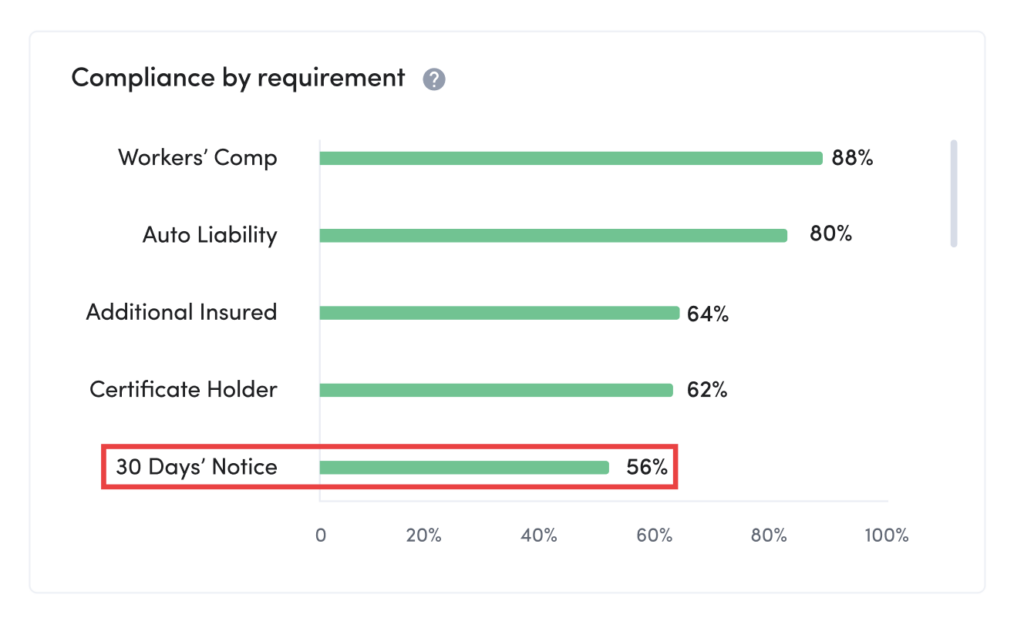

Impact on compliance:

Certificate Holder compliance rates went up from 62 percent to 86 percent.

Issue #2: Missing 30 Days’ Notice of Cancellation

Jessica noticed that the largest gap for 30 Days’ Notice of Cancellation was that it was completely missing. Many vendors and tenants weren’t providing this endorsement to the property management company.

Myth Busted: Insurance companies have no legal obligation to send a 30 Days’ Notice

Why would a property management company feel comfortable dropping an endorsement requirement that protects them from a vendor or tenant promptly canceling a policy that was evidenced on a COI? Well, there’s a good chance a notice of cancellation wouldn’t be sent in the event a policy is canceled. If you look at the fine text of many common notice of cancellation endorsements, verbiage like “failure to mail such notice shall impose no obligation or liability of any kind upon the company” demonstrates that they are low priority and difficult to enforce in most cases.

Suggestion: Drop 30 Days’ Notice of Cancellation requirement

With that in mind, Jessica and the Jones Risk and Compliance team recommended this requirement be dropped entirely.

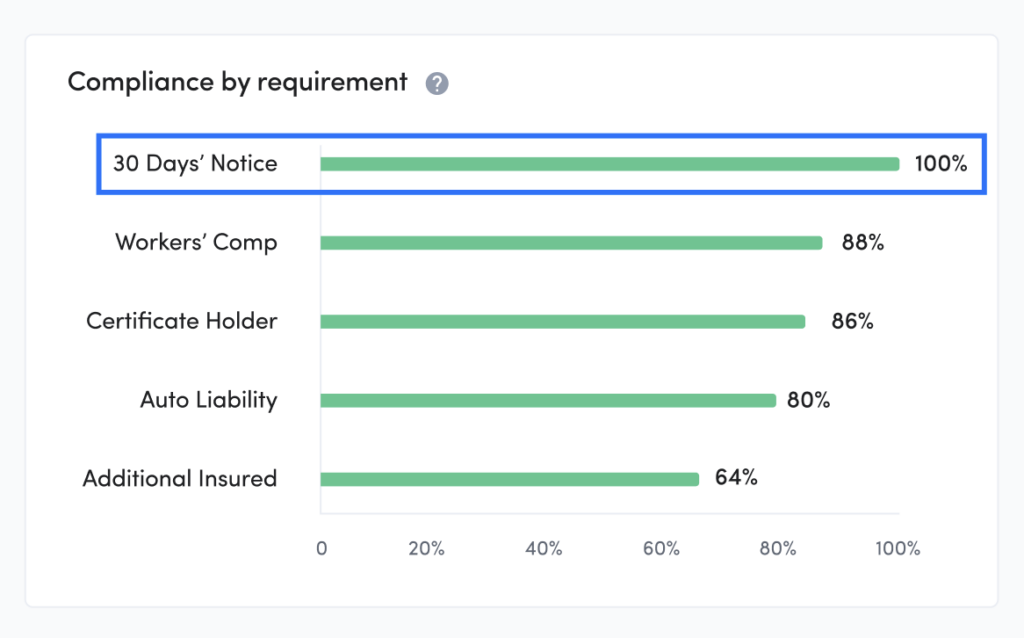

Impact on compliance:

30 Days’ Notice of Cancellation compliance rate went from 59 percent to 100 percent.

Issue #3: Incorrect Additional Insured Names

Due to the organizational structure of this property manager, with different owners for different properties requiring coverage, they required a wide variety of Additional Insured names. This led to confusion about who needed to be listed, spelling and abbreviation mistakes, and more.

Myth Busted: There are other ways to grant Additional Insured status than listing entity names on a COI

Many property management teams assume that the COI needs to specifically list them as AIs to get coverage. However, tenants’ and vendors’ brokers don’t typically amend the policy by scheduling the owner’s and PM entity names. Instead, they list the entity names on the COI in blanket language (aka “any person is an additional insured as per written contract”). That’s why it’s always important to have contracts in place with every one of your vendors and tenants. When you have contracts in place, there’s a better way to transfer risk than listing AIs—Blanket Additional Insured language.

Suggestion: Adopt Blanket Additional Insured

The existence of contracts with vendors and tenants made this portfolio a great candidate for accepting Blanket Additional Insured language. This topic is enough for a newsletter all by itself, so check out our last issue for a full deep dive into the topic.

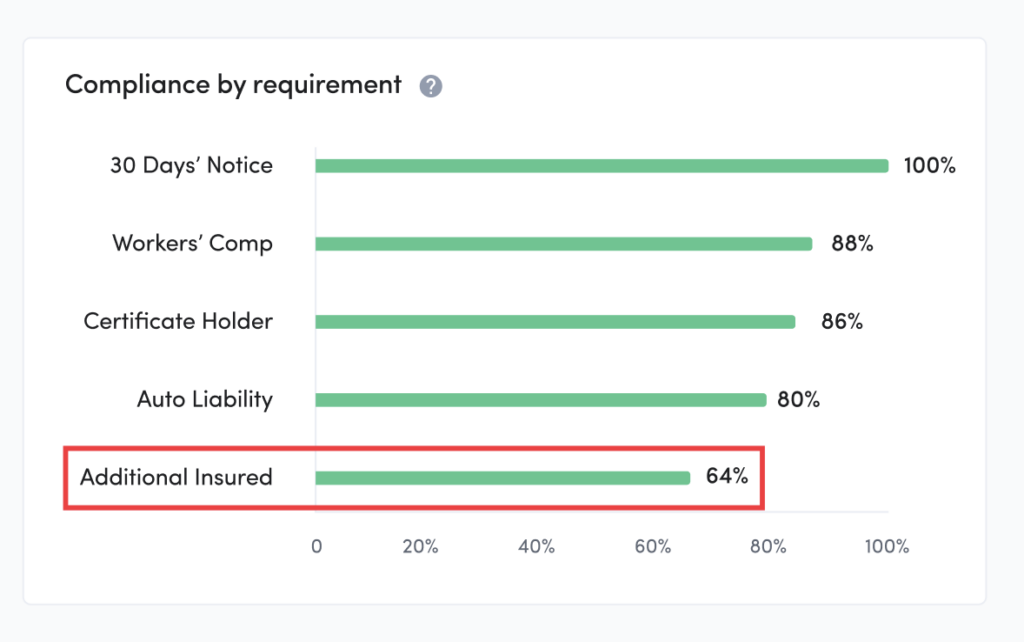

Impact on Compliance:

Additional insured compliance went up by 24%.

How Their Portfolio Compliance Looked After the Changes

After making these changes, the risk management team saw increases to insurance compliance rates across the board. By removing obstacles to compliance that provided limited to no extra protection for the property management company, they managed to improve the vendor and tenant experience while ensuring that they were still protected from insurance risk. Jones customers have also come to similar conclusions about the usefulness of these requirements. For example, we see them waive Certificate Holder gaps at a rate of over 50 percent. In this case, this property manager saved themselves unnecessary time chasing compliance that didn’t commensurately protect them from risk.

Want to learn more about how Jones can help you improve your insurance compliance rates with strategy sessions and better document review? Get in touch with us to learn more.