Last month we held a webinar called “To Waive or Not to Waive: A Crash Course on Insurance Policy Gaps and What They Mean.” We discussed handling common insurance gaps property managers run up against every day. Catch the full replay of the webinar here.

We got a lot of questions about Property Insurance: what it is, what it does and doesn’t cover, and how to handle coverage gaps.

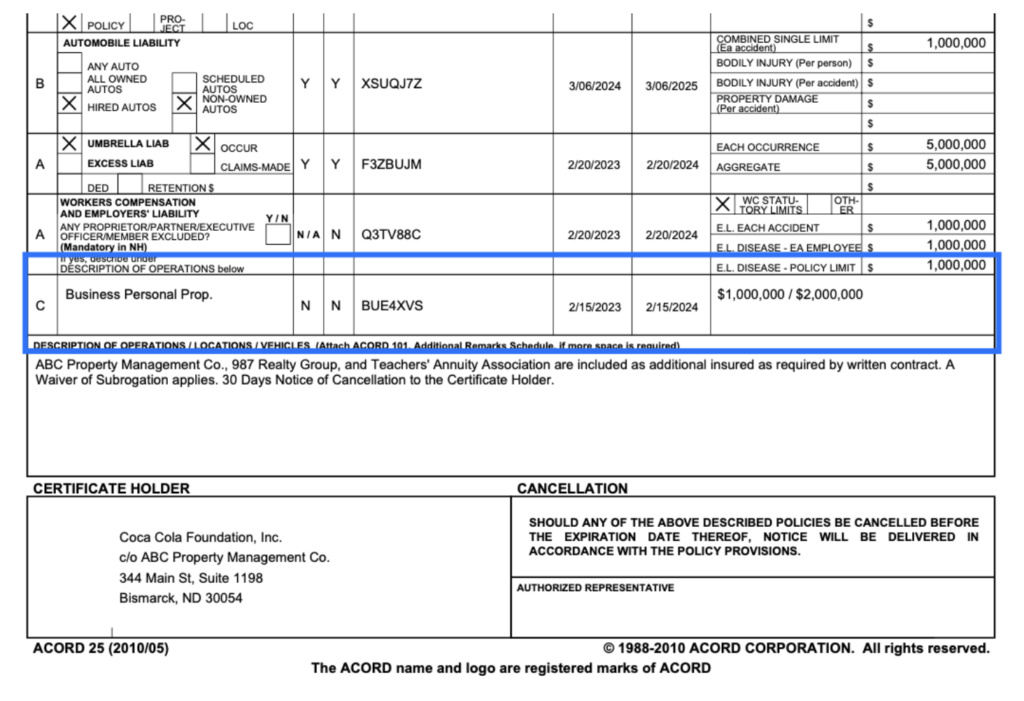

Where Can You Find Property Insurance on a COI?

If you’re looking at an Acord 25, Property Insurance can either be found in the section underneath Workers’ Compensation, or in the Description of Operations section.

Acord 24s, 27s, and 28s also contain specific information about property insurance. If your tenant or vendor submits one of these, check there for property insurance.

First-Party vs. Third-Party Insurance

General liability has a property damage component. Does that mean a vendor doesn’t need to evidence Property Insurance if they have General Liability? Not quite.

GL property damage coverage protects a vendor or tenant from liability in the event they cause damage to the property of others, but doesn’t cover their own equipment or property. It’s an example of third-party liability insurance, or insurance for damage caused to a third-party. Property insurance, on the other hand, is first-party, meaning it covers damages the vendor or tenant suffered to their own property.

Real Property vs. Personal Property

Landlords insure the building itself, known as real property, while tenants and vendors must insure their personal property, including equipment, furniture, and non-structural items. This arrangement protects the landlord or property manager from liability for damage to tenants' or vendors' property.

Note: interested in exploring how Jones can help you automate your compliance management end-to-end and de-risk your building? Talk to our team of experts today!

Basic, Broad, and Special Form Coverage

You might see “Special Form property insurance” as a requirement and have no idea what sort of “special form” you should be looking for. It’s a misnomer – Special Form has nothing to do with a physical form! It refers to what’s covered. Let’s break it down:

- Basic Form only covers specific types of exposure specifically named in the policy, like fire, lightning, smoke, or vandalism.

- Broad Form covers all the perils included in Basic Form policies plus several additional perils, including burglary, falling objects, and water damage.

- Special Form policies list which perils are NOT covered. They cover risks that are difficult to anticipate, while excluding things like floods, earthquakes, and nuclear hazards.

One of the requirements we see most frequently requested of vendors and tenants is Special Form + flood and earthquake coverage. That way, a property management team doesn’t end up in this situation.

Waivers of Subrogation

Require a Waiver of Subrogation for property insurance? It’s going to be pretty hard to get one considering no such endorsement exists! Rights of recovery are often waived by lease wording. The lease itself fulfills a WoS requirement.

If this is a gap you’re seeing frequently, talk to your risk team because you’re never going to get a WoS endorsement for property insurance.

Common Gap Waivers

Not all insurance risk is created equal. Data of waived property insurance gaps for PM teams using Jones shows this. Here are the three most and least waived property insurance gaps in Jones:

Most waived:

- Missing terrorism coverage: 50%

- Missing flood insurance: 64%

- Missing earthquake insurance: 75%

Least waived:

- Property insurance expired: 8%

- Missing plate glass insurance: 14%

- Missing special form: 16%

That’s it for us this week. Want to improve the way you manage vendor and tenant insurance compliance? Get in touch with us via the form below.