Real estate property managers unanimously agree that maintaining insurance compliance for tenants and vendors is critical. However, they often express concerns about having the time and expertise to effectively review contractual requirements, insurance certificates (COIs), endorsements and other documents to make informed decisions.

We put together this little guide to shed light on some of the most common compliance issues you are likely to encounter as a Property Manager as well as some helpful tips to consider.

General Overview of Key Coverages and Terms:

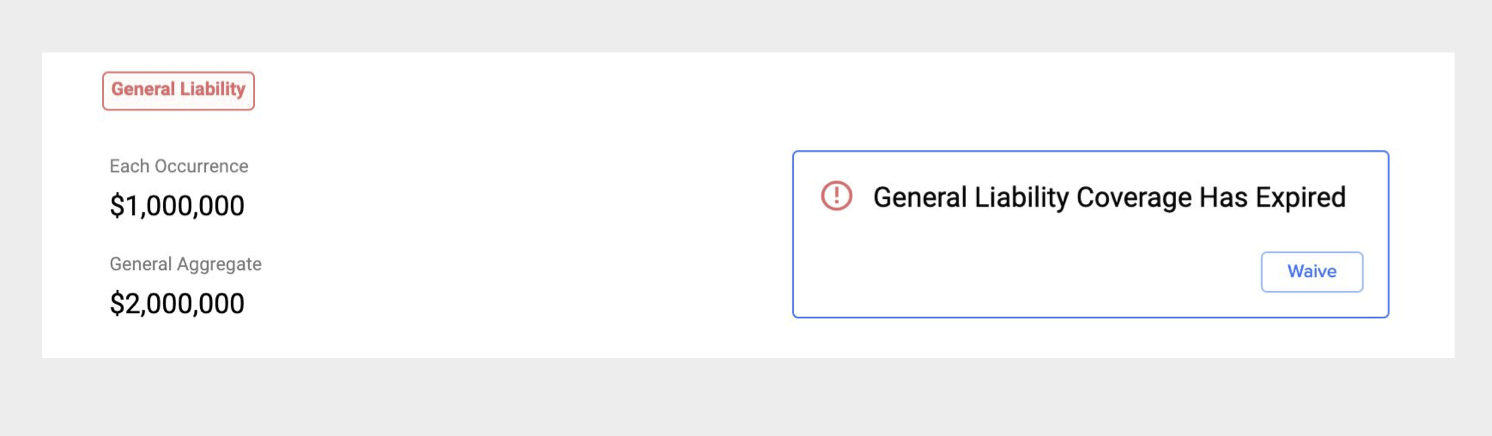

General Liability

- What it is: General Liability is a line of insurance that covers an insured’s third party liability claims for bodily injury or property damage.

- Things to Consider: General liability insurance doesn’t cover employee injuries, auto accidents, punitive damages, workmanship, intentional acts or professional mistakes.

Auto Liability

Auto Liability

- What it is: Commercial Auto Liability policies protect an insured from third party liability claims of bodily injury or property damage caused while operating vehicles used during business operations.

- Things to Consider: Vendors and tenants may be required to cover a specific class of vehicles, such as owned autos, hired autos, non-owned autos, scheduled autos, or all of the above. If no vehicles are used in the operations of their business or if the required category of vehicles is not applicable, they may request a waiver of the Auto Liability requirements from the property manager or landlord.

Umbrella Liability

- What it is: Umbrella Liability policies (also known as Excess Liability policies) are supplementary policies meant to cover for any shortfall in the limits of General Liability, Auto Liability, or Worker’s Compensation policies. Once the limits of any of the three aforementioned insurance lines are exhausted, the Umbrella Policy kicks in.

- Things to Consider: While Umbrella Liability policies may help supplement the limits of other policies, other policies may not be used to supplement Umbrella Liability. If an Umbrella Liability policy is $1 million short of the required limit, for example, adding an extra $1 million to General Liability cannot make up for that shortfall.

Worker’s Compensation

- What it is: Worker’s Compensation insurance helps protect businesses from liability for any work-related injury or sick suffered by its employees.

- Things to Consider: Landlords often require that vendors and tenants maintain Workers Compensation policies that meet statutory limits (ie. as required by the state). That means the policy complies with minimum limits mandated by state law. Fulfillment of the requirement is indicated in the Per Statute checkbox on a COI.

- COVID-19 Considerations: Most states took action via executive order or amended law requiring insurance carriers to recognize COVID-19 as an illness covered by Worker’s Compensation. However, given that state laws vary, the issue has become what categories of work are covered under the law changes. Some states are only taking action to extend workers’ compensation coverage to include first responders and health care workers impacted by COVID-19. Other states are extending coverage to all workers otherwise covered under Workers Compensation Furthermore, the burden of proof is on the employer and insurer to prove that the infection was not work-related making it easier for those workers to file successful claims.

Property Insurance

- What it is: Commercial property insurance protects an insured’s physical assets from fire, explosions, burst pipes, storms, theft and vandalism. This is distinct from General Liability which covers damage to a third party’s property but not the property of the insureds.

- Things to Consider: Earthquakes and floods are typically excluded from commercial property insurance, unless purchased separately as an extended coverage.

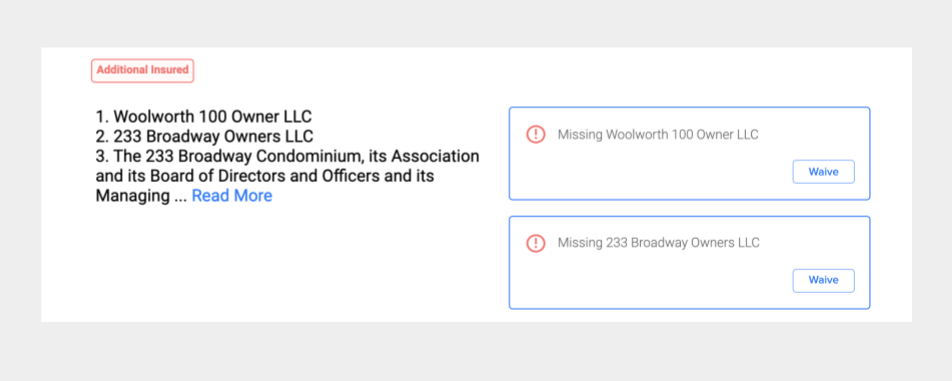

Additional Insureds

- What it is: Additional Insured status extends the coverage of a policy to persons or organizations apart from the Named Insured. This is usually conveyed in the Description of Operations of a COI or added to the policy as an Additional Insured endorsement.

- Things to Consider: There are two types of Additional Insured endorsements. Scheduled Additional Insured Endorsements confer coverage to persons or organizations listed out in a written schedule whereas Blanket Additional Insured Endorsements confers coverage to anyone who fits a certain class description, such as property managers, owners or lessors.

Waiver Of Subrogation

- What it is: A Waiver of Subrogation is a provision that prohibits an insurance carrier from recovering the money it paid on a claim where the parties held liable include not just the Insured but also other third parties not covered on the policy. In other words, it prevents the insurance company (who steps into the shoes of the Insure) from suing the other party to the contract – which likely caused the loss.. Landlords often require this provision from their vendors and contractors insurance carriers to avoid being held liable for claims that occur on their property.

- Things to Consider: Waivers of Subrogation apply on a per policy basis. A waiver of subrogation on one policy will not carry over to another policy from the same broker, for example, unless explicitly stated in the insurance certificate or endorsement/s

Primary and Noncontributory

- What it is: Landlords often require that contractor’s insurance be held on a Primary and Noncontributory basis. This relates to cases where multiple insurance policies could cover a claim. When a policy is held on a Primary and Noncontributory basis, it means the insurance carrier agrees to pay out the claim acting as the primary source of coverage or whatever claim may arise up to the policy limit without seeking any form of contribution from the other policies.

- Things to Consider: Primary and Noncontributory can usually be found either in the Description of Operations of a COI or in an accompanying endorsement.

We hope that this guide will be a resource for you as you work to ensure that you and your landlord are protected. For any further questions or to learn more about how Jones may be able to help streamline insurance compliance at your property visit www.getjones.com.