Here’s the criteria we evaluated each subcontractor compliance management tool on:

—Product Features

—Industry Specializations

—Customer Support

—Integrations

—Quality of Insurance Review

The Final Verdict

—Jones is the top overall subcontractor compliance management tool, with the highest standards of document review, frictionless no-login document uploads, and the only embedded Procore integration (read more about embedded integrations here). However, Jones only serves GC and CRE, so companies from other industries need to look elsewhere.

—myCOI brings years of experience to the table, but reportedly has struggled to review documents in a timely manner over the last 9 months to a year. It does serve more industries than its competitors, so anyone looking to manage insurance for trucking, waste management, commercial marijuana sales, or aviation may want to choose this option.

—Trustlayer has good customer support and manages the collection and review of insurance documents end to end, but minimal reporting options and confusion over requirements make acting on compliance issues difficult.

In this guide

—Features to Look for in a Subcontractor Compliance Tool

—Comparing Three Top Subcontractor Compliance Management Software Tools

—Crowning the Best Subcontractor Compliance Management Tool

Note: interested in exploring how Jones can help you automate your subcontractor compliance management end-to-end and de-risk all your projects? Talk to our team of experts today!

Features to Look for in a Subcontractor Compliance Management Tool

Not all subcontractor compliance solutions created equal. Ask about these 5 key criteria when you’re choosing the right subcontractor compliance management tool for your GC.

Fast COI and Endorsement Review Times

Slow insurance document review that prevents subcontractors from quickly getting to work spurs many GCs to begin searching for a subcontractor compliance tool. Ask the subcontractor compliance tool vendor what their average turnaround time is for a COI and endorsement review. If their average review time is over 24 business hours, look elsewhere.

TL;DR: If a subcontractor compliance tool can’t commit to sub-24 hours document review times you should look elsewhere.

Ease of Use for Subcontractors

If your subcontractor compliance management tool makes it difficult for subcontractors to upload their documents by asking them to create an account and password, they’re going to be less likely to submit their documents and less likely to want to work with you in the future. No-login flows are the lowest friction option.

TL;DR: Look for a solution that has an easy document upload flow and requires minimum input from your subs.

Built for the Needs of the Construction Industry

Most of the COI trackers available today are industry agnostic and capable of serving a wide variety of different companies. As a GC, that should be a red flag. Construction takes risk exponentially more seriously than most other industries, and there are many industry-specific concepts, coverages, forms, and certificates that your software should be familiar with. Make sure the tool you choose supports GC specific workflows and is capable of sorting subcontractors on both a global and project level.

TL;DR: If a subcontractor compliance tool boasts about serving over 20 industries, you can be almost certain that it’s not a specific enough platform for the high risk world of construction.

Bonus: Embedded Integration with Procore

If your organization uses Procore, ensuring the subcontractor compliance tool you choose has an embedded integration with Procore should be nonnegotiable. With an embedded integration, users don’t need to constantly switch between Procore and an App in order to perform core tasks. An embedded Procore integration is capable of both pushing information to and from another system, so your subcontractor compliance tool should both be able to push and receive data to and from Procore. Otherwise you’ll be stuck having to manually update Procore every time you collect a new set of subcontractor insurance documents, and manually update your compliance software every time you create a new project.

TL;DR: If the subcontractor compliance tool you choose doesn’t integrate with Procore and the other software in your stack, you’re going to be stuck with a lot of additional manual data entry.

Comparing Three Top Subcontractor Compliance Management Tools

Now that we’ve discussed the must-have features of any subcontractor compliance tool, let’s go over three of the leading players in the space: Jones, myCOI, and Trustlayer. Each solution has pros and cons that make them right for the needs of different organizations.

Jones: The Top Overall Subcontractor Compliance Management Tool

Jones is the top subcontractor compliance management solution on the market, bringing GC specific workflows and high quality of document reviews to the table as well as an embedded integration with Procore. However, it’s only an option for brands in the GC and CRE spaces.

Advantages of Jones as a Subcontractor Compliance Management Tool

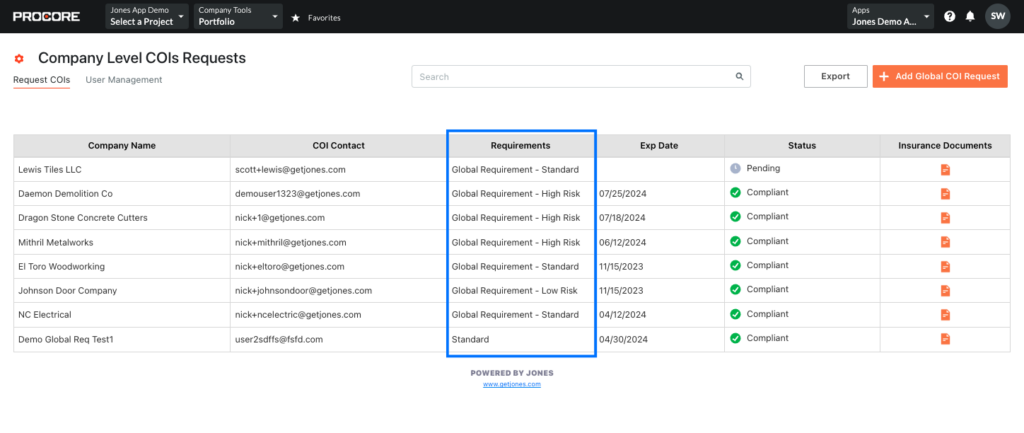

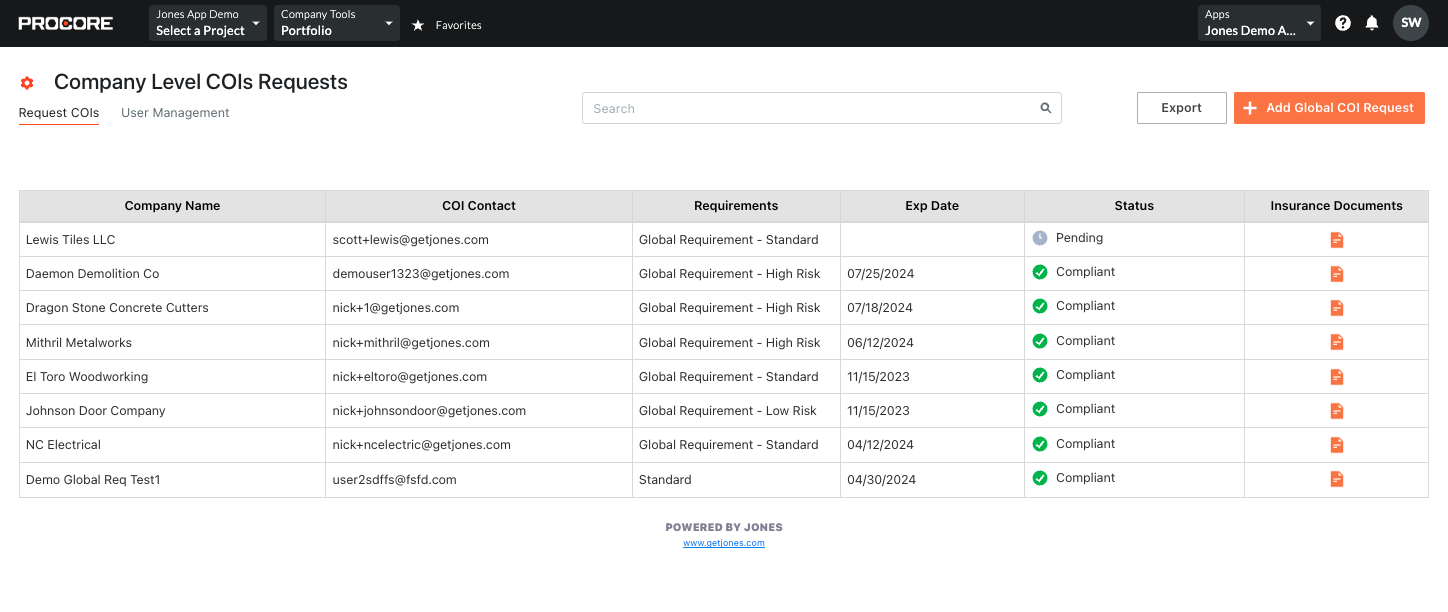

Commitment Triggered COI Requests and Global Insurance Requirements via Procore Integration

Jones is the only subcontractor compliance management tool with an embedded Procore integration. Jones eliminates all confusion over COI collection by sending automatic notifications whenever new commitments are created in Procore, making it nearly impossible to miss requesting COIs. Jones also makes managing Global Insurance Requirements directly in Procore simple, with categorization capabilities to differentiate global-level subs from project specific subs.

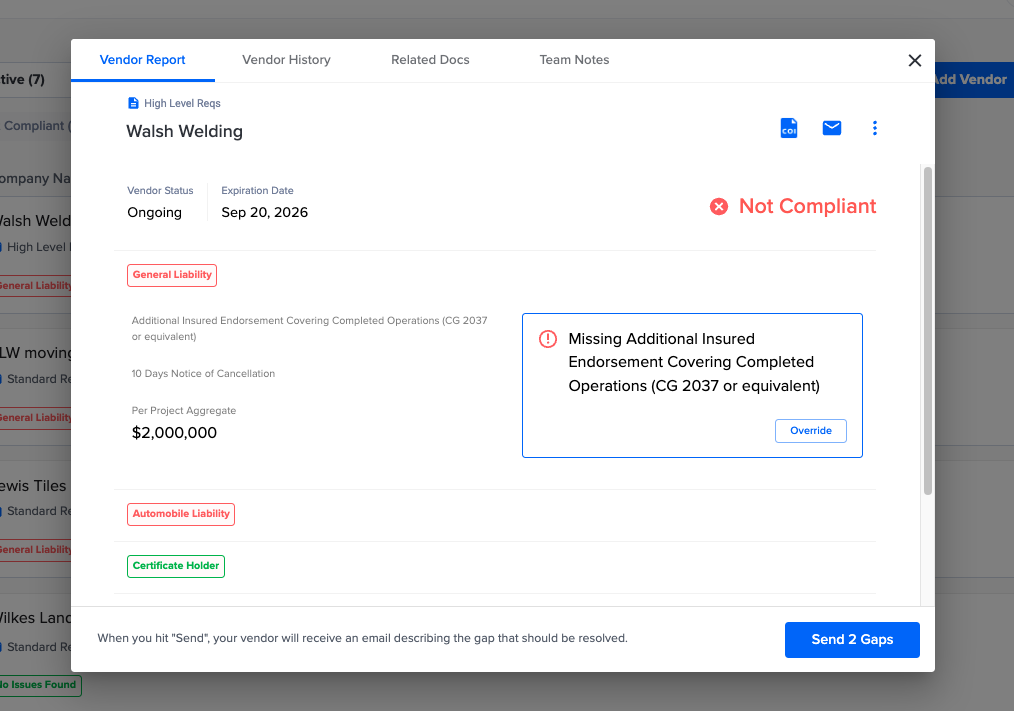

Fast and Accurate Document Review

Jones maintains a sub-24 hour standard document review time, with 99.6% accuracy over the course of 1.5 million COI and endorsement reviews. The combination of review accuracy and speed is one of the primary selling points of the Jones platform. Customers have reported a significant increase in document review quality and efficiency when switching to Jones from myCOI and Trustlayer.

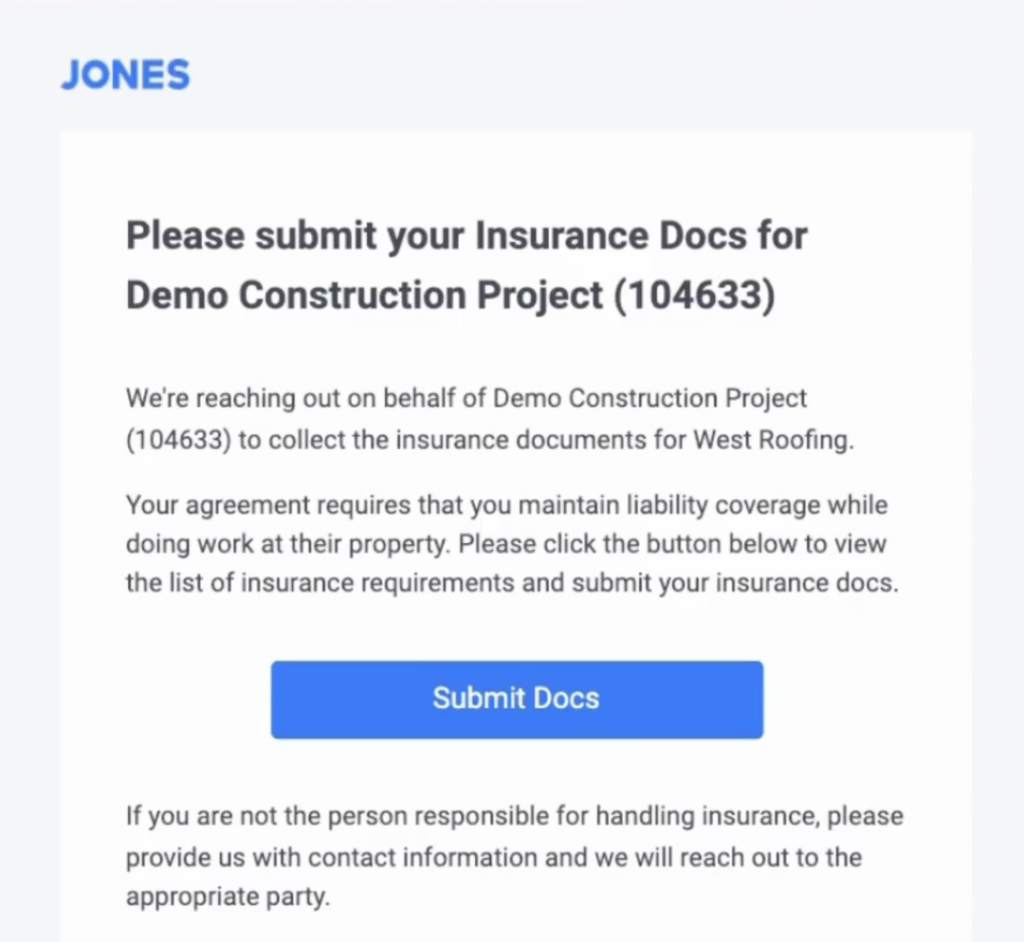

Login-Free Document Uploads

Jones allows subcontractors to upload insurance documents without creating an account. This increases collection rates by 2x and was a deciding factor for several clients who switched off myCOI early to migrate to the Jones platform who reported their subs “hated having to register to submit documents.”

Disadvantages of Jones as a Subcontractor Compliance Management Tool

Only Serves Two Industries

Unfortunately for non-GC and CRE companies looking for a subcontractor compliance tool, Jones isn’t best suited for them. As an industry-specific solution, Jones workflows are designed to fit the unique needs of the construction and CRE spaces.

Rigorous Auditing Standards Can Cause Initial Low Compliance

Jones customers are occasionally surprised at their initial low compliance numbers when onboarding onto the Jones platform. However, this is largely as a result of the fact that the company is only beginning to see the state of how their compliance really has been handled in the past. With some quick adjustments and revision of problematic requirements, customers are quickly able to boost their numbers on Jones.

myCOI: The Subcontractor Compliance Management Tool Serving the Widest Variety of Industries

myCOI is a legacy COI tracking tool that serves multiple industries including education, real estate, manufacturing, hospitality, cannabis sales, and more. They’re one of the original brands in the subcontractor compliance space. Let’s break down some of the pros and cons of the myCOI platform.

Advantages of myCOI as a Subcontractor Compliance Management Tool

Lots of Industries Served

As briefly mentioned before, myCOI can help organizations in a variety of industries with the management of their subcontractor and vendor COIs and endorsements. The industries myCOI offers their services to include those mentioned above, as well as government, waste management, and transportation. For companies in these spaces looking to manage their subcontractor compliance, myCOI is a good choice.

Over 15 Years in Business

As a legacy brand, myCOI has a long track record of delivering value to its customers. With fifteen years of experience in the subcontractor compliance industry, myCOI has proven that longevity isn’t a concern. If you opt to have myCOI manage your subcontractor compliance, you can rest assured that they’ll be around in the years to come. Considering claims can surface years after projects are completed, that’s key.

Disadvantages of myCOI as a Subcontractor Compliance Management Tool

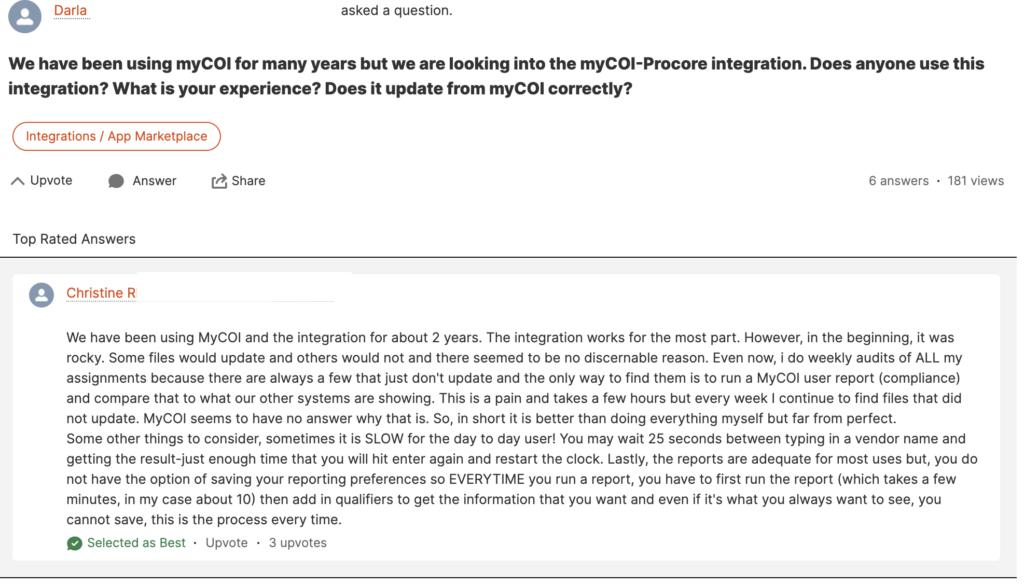

Slow Document Review

Customers have reported myCOI’s average document review time to range anywhere from several days to several weeks. We have heard from multiple former customers that myCOI has cited a “period of unprecedented growth” as the cause for delays in subcontractor COI and endorsement reviews. If they’re struggling to keep up with an influx of submissions, adding additional customers can only be expected to continue to increase the average time for myCOI’s document checks.

Limited Procore Integration Capabilities

myCOI does offer an integration with Procore. However, customer reports on the Procore forums indicate that the capabilities of the integration fall short of expectations. One customer reported that their Procore integration with myCOI failed to properly sync, with no explanation from myCOI. While still better than having to manually upload data, the fact their Procore integration is only a one way data connection greatly limits its capabilities compared to the embedded Jones Procore integration.

Upsells Insurance Products to “Noncompliant” Vendors

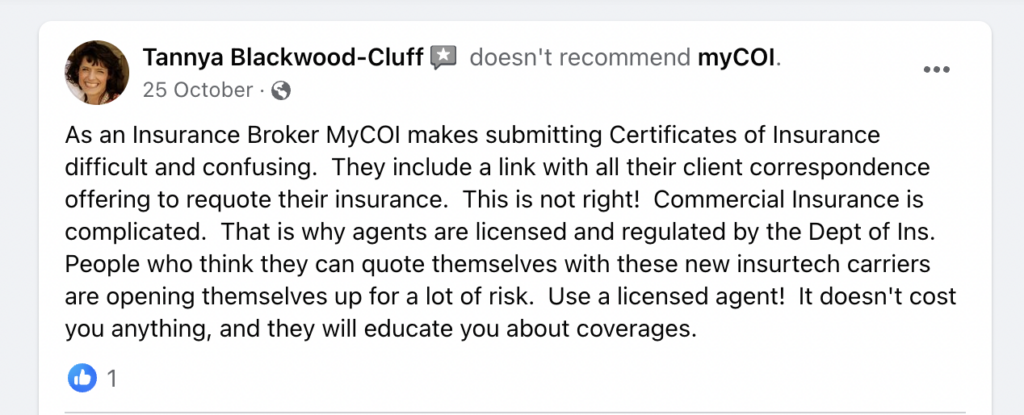

Recent online reviews of myCOI from licensed insurance brokers indicate that myCOI attempts to use noncompliant subcontractor records as an opportunity to upsell their own insurance products. Considering they are the arbiter of subcontractor compliance, trying to sell insurance based on judgements they issue is a precarious proposition. COI stands for “Certificate of Insurance”, but in the case of using compliance status to sell insurance products COI might as well stand for conflict of interest.

Trustlayer: Good Customer Support with Reporting and GC-Specific Shortcomings

Trustlayer is a newer company than myCOI, and brings high level customer support and an end-to-end process to the table. However, shortcomings in their document review capabilities and lack of reporting capabilities make taking action difficult.

Advantages of Trustlayer as a Subcontractor Compliance Management Tool

Good Customer Support

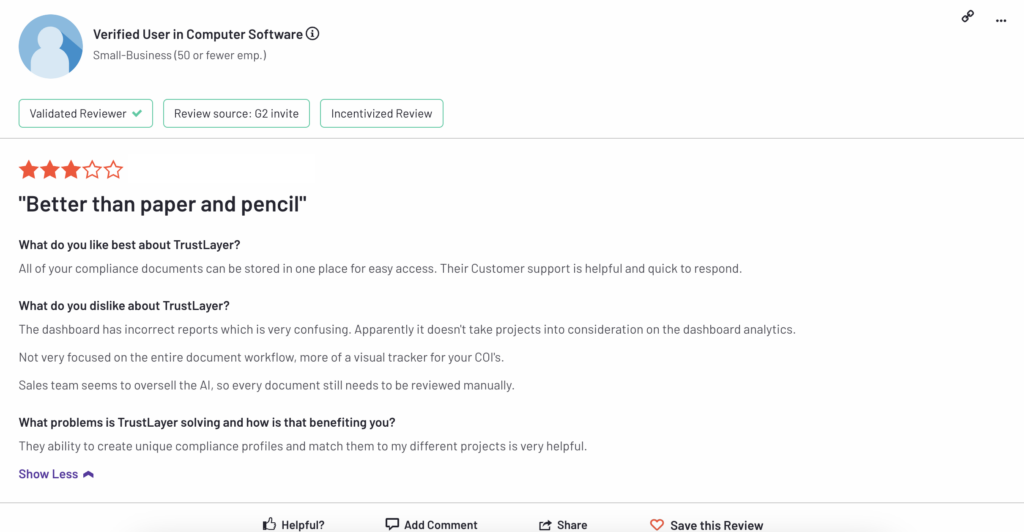

Reviews online highlight the high quality of Trustlayers’ customer service. One review indicated their customer support was the best part of the value proposition, while noting that their AI occasionally struggles to ready insurance documents. However, she mentioned that the CS team at Trustlayer helped overcome any product issues she had.

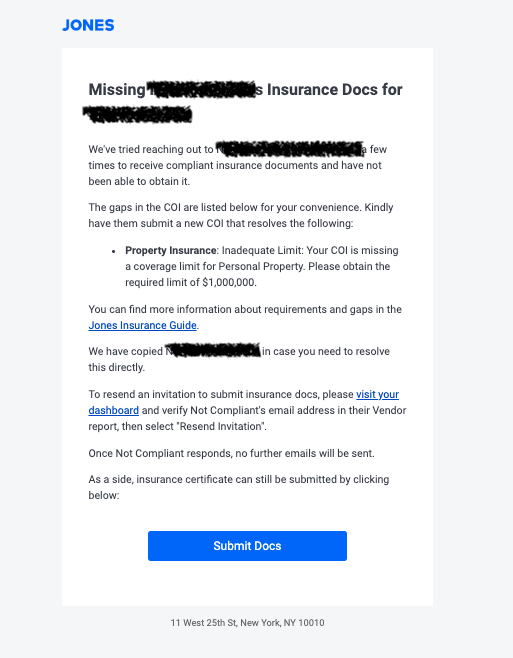

Handling Communication of Gaps to Subcontractors

By taking the communication of gaps off the GC’s plate, Trustlayer minimizes the need for back and forth conversations with subcontractors about insurance. This gives GC accounting and risk teams time back to handle other tasks.

Disadvantages of Trustlayer as a Subcontractor Compliance Management Tool

Procore Integration Can Only Track Subs on a Global Level

Conversations with former Trustlayer customers have indicated that Trustlayer is not able to store global-level subcontractors and project specific subcontractors separately with their Procore integration. As our guide to Global-Level Insurance Requirements showed, being able to distinguish these two groups is key. Unfortunately, it’s not an option in the Trustlayer platform.

Minimal Reporting Capabilities

A former Trustlayer customer reported in a call with us that “there are no reporting capabilities to help [them] figure out why vendors aren’t compliant without drilling down into every interaction they had with Trustlayer.” Another certified G2 review echoed these complaints, indicating that Trustlayer’s dashboards tools were a significant shortcoming of the platform. A lack of reporting options make visualizing compliance difficult, which is a concern for Trustlayer customers.

Confusion Over Requirements

If a subcontractor compliance management tool can’t get your requirements right it’s a massive issue, as you may not have the coverages required to protect your organization from risk. Former Trustlayer customers have reported that “oftentimes Trustlayer asks for requirements that [they] don’t mandate” and that subsequently it takes their team “far more effort than necessary to get vendors compliant.” Not being able to follow requirements is a major red flag for Trustlayer.

Crowning the Best Subcontractor Compliance Management Tool

All three of the tools listed have strengths and weaknesses, but it’s Jones that comes out on top after a head-to-head comparison. Whether it’s the Jones embedded Procore integration, the speed and accuracy of insurance document review, or the login-free document upload flow, Jones should be the subcontractor compliance management tool of choice for GCs. Get in touch with the Jones team via the form below to learn more.