Lesson 1: Don’t Confuse Tooltip AI with Trustworthy AI

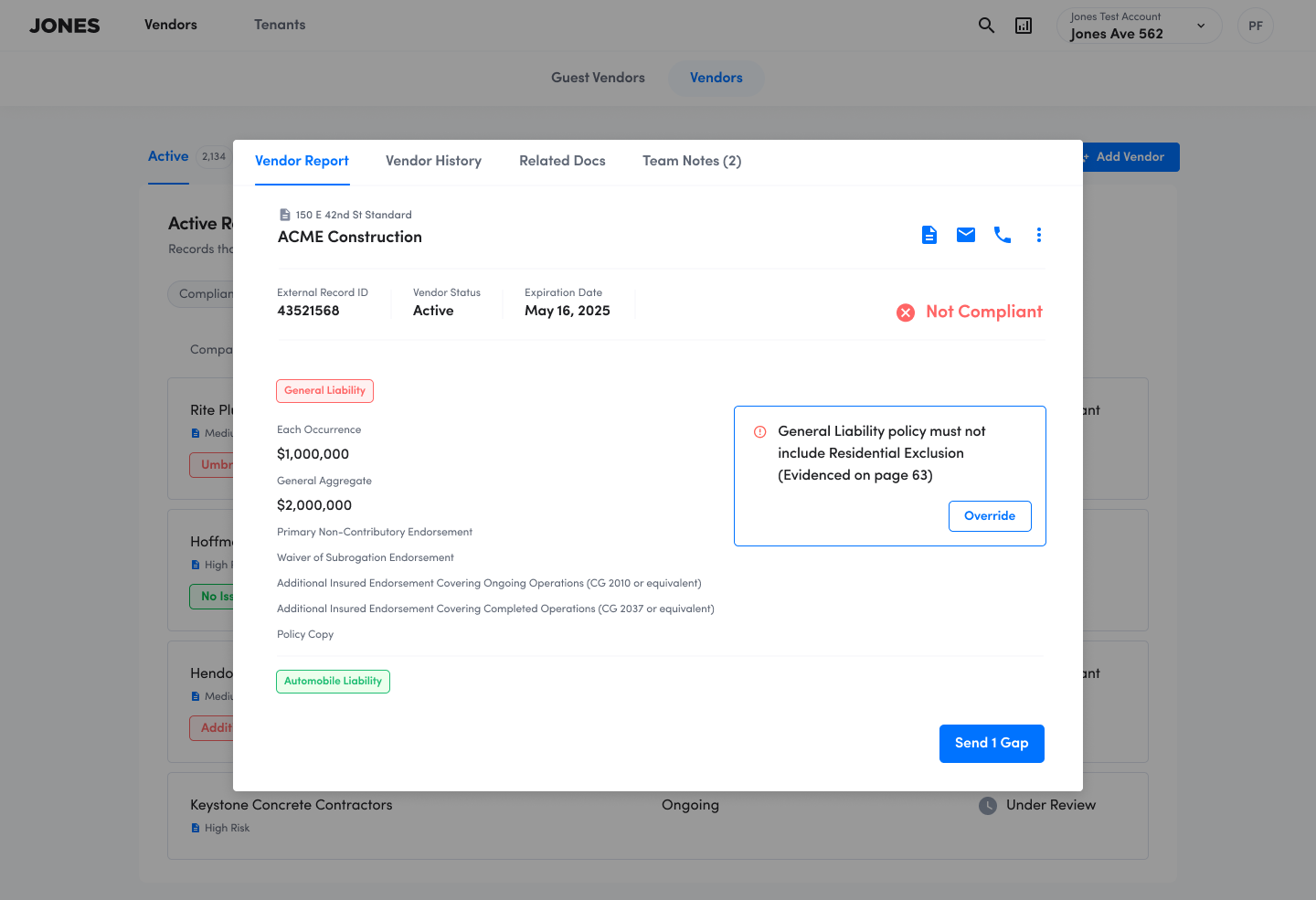

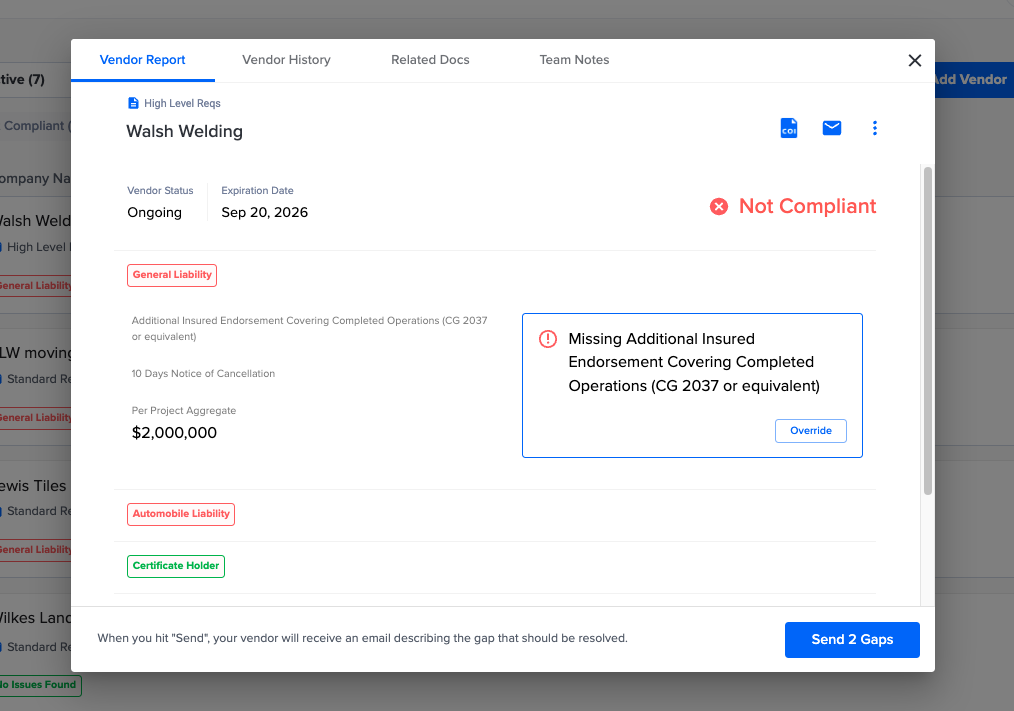

In a rush to join the AI conversation, some platforms have shipped lightweight features that mimic intelligence but deliver little substance. For example, we’ve seen interfaces where a user clicks a small icon next to a COI field to receive AI-generated commentary on that field. At a glance, it appears helpful—the AI explains what “general liability” means or flags that a date is expired.

But these features rarely integrate into the platform’s core compliance logic. They don’t actually assess whether a vendor meets requirements across the board. They don’t recommend actions. They don’t notify stakeholders when policies lapse.

These tooltip-like experiences give the illusion of intelligence but ultimately ask the user to do the hard interpretive work. They create a false sense of coverage.

What to do instead: Embed AI at the heart of the insurance operations engine. It should power the extraction, structuring, validation, and auditing of COI data. It should compare insurance policies against project requirements in real time. And it should escalate intelligently when something is missing or wrong.

When used well, AI isn’t just a helper. It’s a second brain. But only if it’s doing the work that actually matters.

Note: Ready to explore how Jones can streamline your COI management process? Talk to our team of experts today!

Lesson 2: Don’t Hand Off Complexity in the Name of PLG

The rise of product-led growth (PLG) has inspired many platforms to build self-serve onboarding flows. The idea is simple: let users sign up and configure the platform themselves without having to talk to sales.

But compliance isn’t a simple problem. We’ve seen onboarding flows that ask users to define insurance requirements, set up audit logic, and even classify vendors—all before they’ve seen value from the product. One platform launched a “streamlined” sign-up experience, only to quietly pull it after users struggled to understand what they were being asked to do.

This self-serve friction is more than a UX problem. It puts the burden of accuracy on the very people trying to offload it. In a field where a missed checkbox can lead to real-world liability, asking clients to configure insurance workflows themselves is irresponsible.

What to do instead: Design product-led experiences around outcomes, not configuration. Use AI to intelligently pre-fill requirements based on project type. Offer templates that reduce the risk of human error. And guide users with clear explanations, rather than dumping them into a dashboard.

Self-serve should not mean self-support. In compliance, the goal isn’t just usability—it’s confidence.

Lesson 3: Don’t Forget That Brokers Are Partners—Design for Them

There’s a perception in the compliance world that brokers are gatekeepers or friction points. But this view misses the bigger picture.

Brokers are a critical link in the insurance data supply chain. They are responsible for issuing and maintaining accurate certificates, and they carry professional liability (E&O) exposure if they provide bad data. That means their incentives are aligned with compliance platforms and clients alike: they want the data to be right.

The real issue isn’t misalignment—it’s enablement. Most compliance platforms don’t design for broker adoption. They expect brokers to navigate clunky portals or one-off email workflows. Unsurprisingly, engagement is low.

What to do instead: Build lightweight, broker-friendly interfaces that make it easy to upload, update, and verify policies directly from their preferred operating system. Offer integrations that minimize double-entry. Allow brokers to see which policies are still in review and where gaps exist.

Compliance is a team sport. If you want accurate, up-to-date insurance data, design for the people who own it.

Lesson 4: Don’t Rely on Legacy Systems to Become Your System of Record

Many platforms today try to build bridges to legacy insurance systems—carrier portals, broker databases, and static policy PDFs. The thinking is: if we can just plug in, we can synchronize data at scale.

But these systems weren’t built for structured, real-time verification. They weren’t designed for interoperability. In some cases, the “integration” amounts to scraping PDFs or emailing policy admins for updates. This introduces latency and fragility into the very foundation of compliance.

What to do instead: Become the source of truth. Build a system of record that ingests insurance data directly from vendors and brokers, structures it, verifies it, and maintains it over time. Offer a digital profile that follows the vendor across projects.

When the industry moves to digital insurance (and it will), only the platforms that own the structured, verified data will matter.

Lesson 5: Don’t Treat Trust Like a Feature—It’s the Foundation

In this category, the end user isn’t just looking for a tool. They’re looking for confidence. They want to know: Are we covered? Did we miss anything? Can I trust this system when something goes wrong?

We’ve seen AI features that promise the moon but crumble under edge cases. We’ve seen platforms optimize for growth at the expense of reliability. But the most dangerous thing a compliance platform can do is fail quietly.

What to do instead: Make trust your north star. Build transparent audit trails. Create AI systems that show their work. Offer human-in-the-loop safeguards and escalation paths. And most importantly, be willing to guarantee outcomes.

Shameless plug: Our new Jones Operator offering does exactly that. We don’t just process COIs—we take accountability for making sure our clients stay compliant, and we guarantee the outcomes (or your money back!). Because in the world of insurance, the cost of getting it wrong is too high to settle for half measures.

Final Word: Building the Right Way

Insurance operations is not just a workflow problem. It’s a risk problem. It’s a trust problem. And as AI transforms how we work, we must remember that transformation without accountability is just noise.

If you’re building AI in this space, we hope these lessons help you skip some of the pain. And if you’re buying AI-driven compliance tools, ask the hard questions: Does this system stand behind its work? Will it still perform under pressure? Can I trust it when it matters most?

Because at the end of the day, that’s what compliance is really about: not doing the work, but knowing it’s done right.

Tired of Reviewing COIs and Endorsements Manually?

Jones automates the collection and review of COIs for property management companies, owner-operators, and general contractors across the US. Reach out to us via the form below to find out more about how Jones can help your organization manage your insurance documents.