Welcome and thank you for everyone joining us today. This is another webinar in a series of educational and informative sessions around various insurance topics. This one is about COIs versus policies—why verifying policies for exclusionary language matters. The panel includes the Director of Risk and Compliance at Jones, who oversees auditing operations and training, and an Insurance Policy Analyst who leads the charge on reviewing full insurance policies and exclusions.

We’re now talking about policy verification a lot. Over the past few years, this wasn’t coming up in customer conversations, but now it’s becoming natural—often initiated by customers themselves because they’re realizing that verifying COIs alone is not sufficient. Companies are including policy verification in their risk and insurance programs because they understand the COI only provides a summary of coverage. The full policy reviews detailed coverage, conditions, potential gaps, and limitations that the COI simply does not show.

Here’s the flow: A COI is provided by a subcontractor, reviewed, and becomes compliant. You hire that subcontractor to perform work. Then an accident happens—maybe an employee falls off a ladder during the project. A claim happens, and when that claim happens, people don’t go back to the COI. That’s not how claims are settled. They go to the policy. The policy is reviewed, and a lot of coverage is revealed. Many times, unpleasant surprises come up. Imagine you realize that subcontractor had a policy with a height exclusion stating that any work in a building or structure over 3 feet is not covered by that CGL policy. They had all the limits you wanted, all the language, all the endorsements—but none of them mattered because they had an exclusion related to the type of work being performed. You’re left with no coverage at all.

It’s happening more and more often. A year and a half ago, we started building the knowledge and product to support policy review because we were seeing opportunity—people were talking about these claims where they had compliant COIs, were doing their job tracking certificates, but still that wasn’t sufficient to protect them. This significantly improved when we started working with more general contractors, where claims happen all the time. We realized this is a big pain point that a lot of people are facing.

There are endorsements that are typically part of COI review—Additional Insured endorsements, Waiver of Subrogation, Primary and Non-Contributory. These are common in contracts and people are used to providing them attached to a COI. However, if you ask for a Designated Work endorsement or Limitation endorsement, they’re not going to know what that is because that’s not typical practice to provide with a COI. These endorsements are part of the policy, but they’re not going to provide endorsements that exclude coverage. The COI states what applies—it doesn’t state what the policy doesn’t cover.

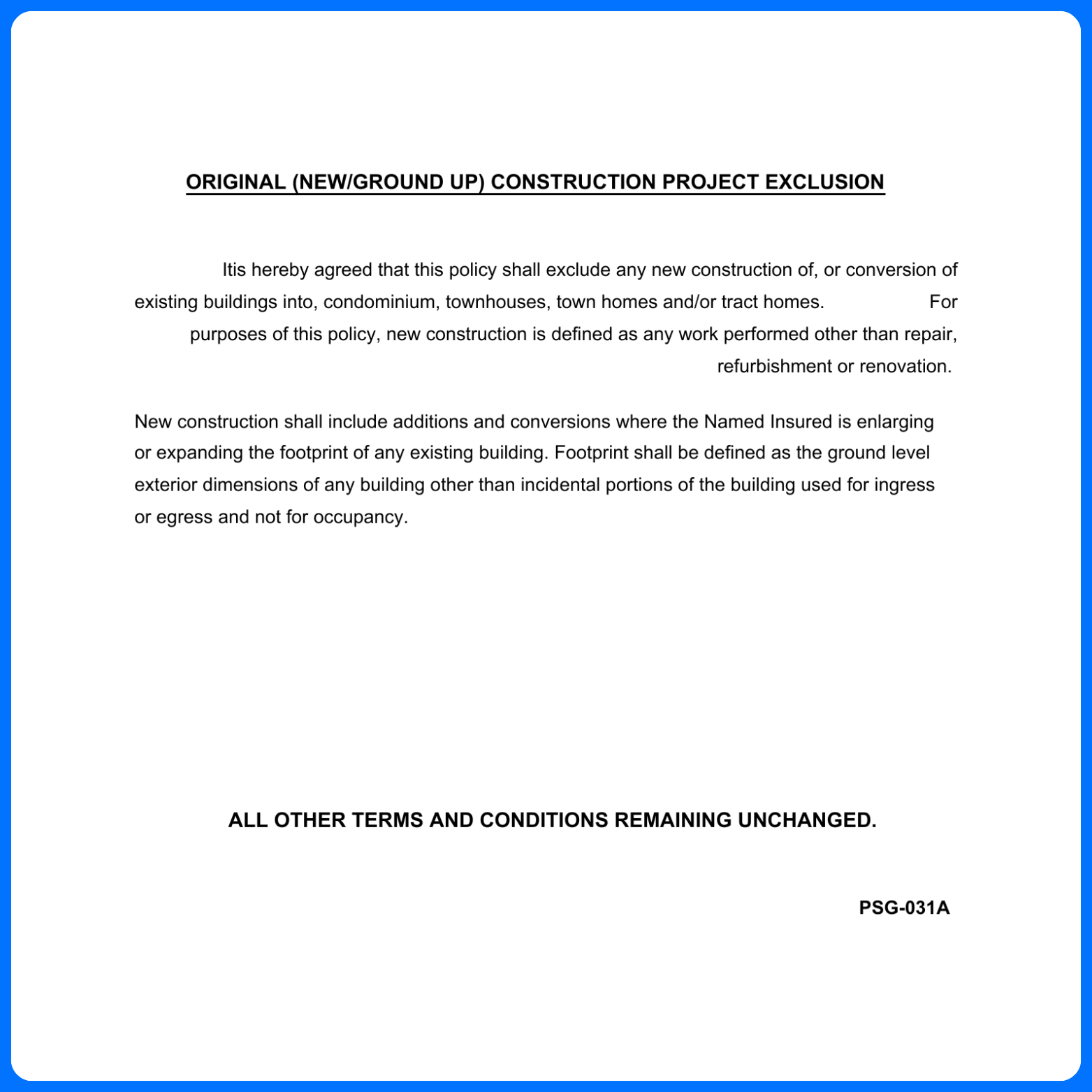

We have real examples from the Jones system. A construction company had requirements for $1M CGL, Primary, Waiver of Subrogation, and Additional Insured endorsements. They got compliant with that. The COI showed CGL, Auto, Umbrella, Workers Comp—all limits were perfect, dates were good, language was necessary, endorsements were attached. Perfect. They were compliant. This was for a home building general contracting company customer. They got approved and were likely hired. Once this GC started doing policy review, we noticed they had a problematic gap. When we reviewed the policy, we found a residential exclusion evidenced on page 63. The exclusion stated: “This insurance does not apply to bodily injury, property damage, or personal advertising injury arising from your work performed by the policyholder or anyone they hire—on a townhome, residential cooperative, residential condominium project, or residential housing project if the total number of individual residential units is greater than 25.” Coverage is excluded for this specific situation. Even though they have all the limits, all the Additional Insured endorsements, all the relevant provisions—if they’re working on projects with individual residential units over 25, they have no coverage.

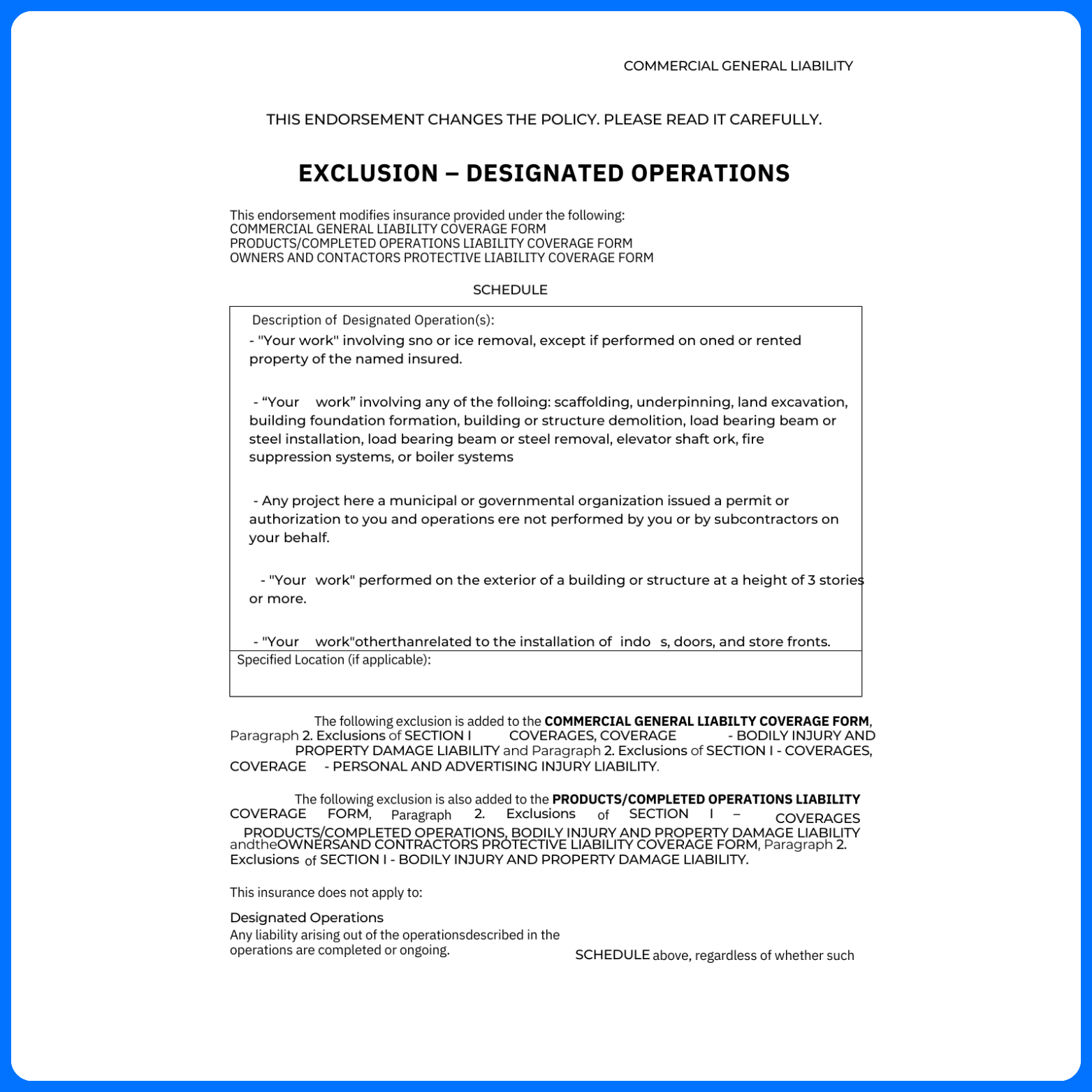

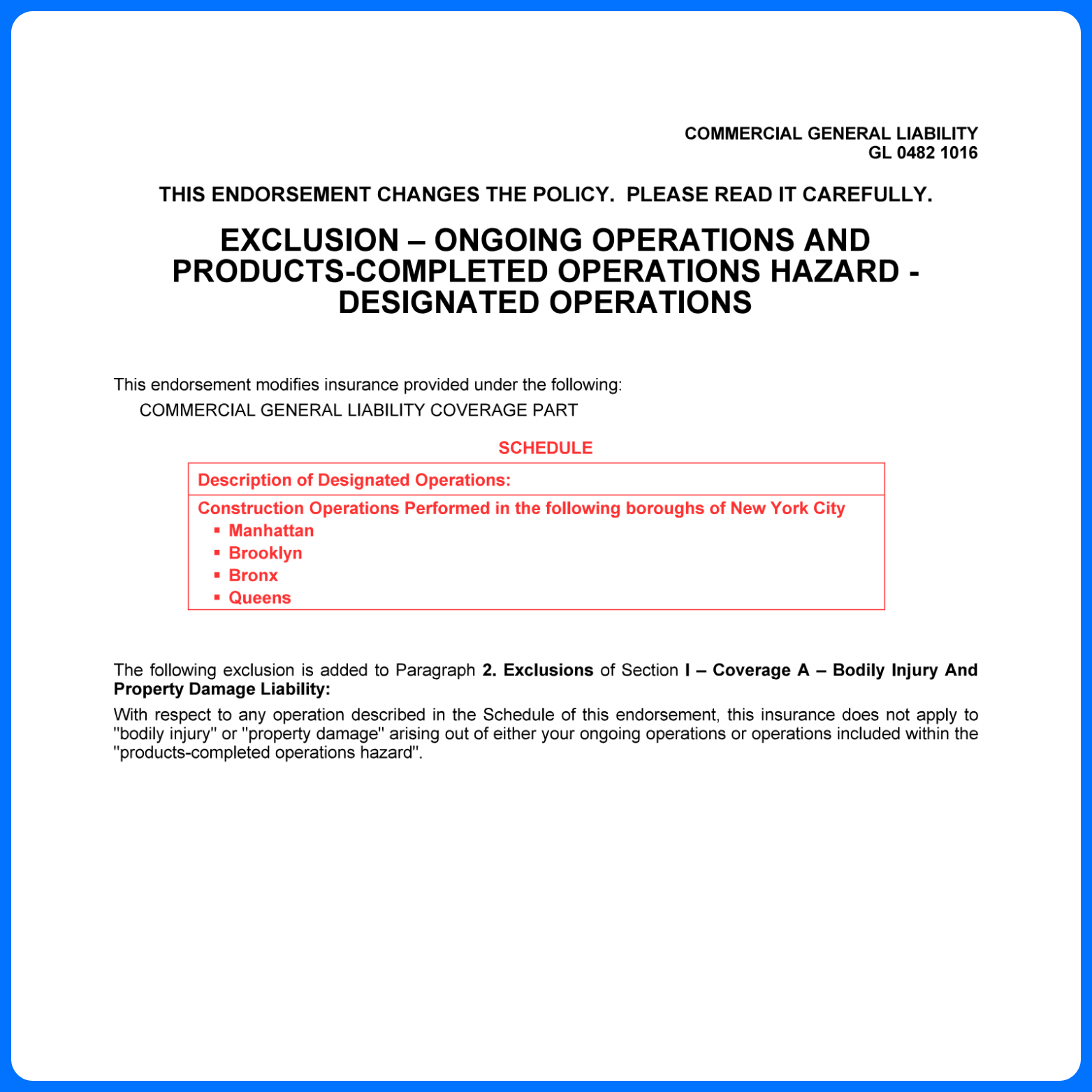

An installation and contracting company—a subcontractor involved in a high-risk project—had a compliant COI. GL, Auto, Workers Comp, Certificate Holder, Additional Insured, all perfect. When we reviewed their policy, we were surprised with a couple of gaps. In the general liability policy, they had a height restriction and an EIFS exclusion—both big deals for this type of company. The COI showed everything perfectly, but the policy had these exclusions. On page 73, we found a Designated Operations exclusion. In the schedule box, they were describing “any exterior work on any building or structure which requires work in excess of 30 ft from exterior grade.” Any work related to this level of height is excluded from coverage.

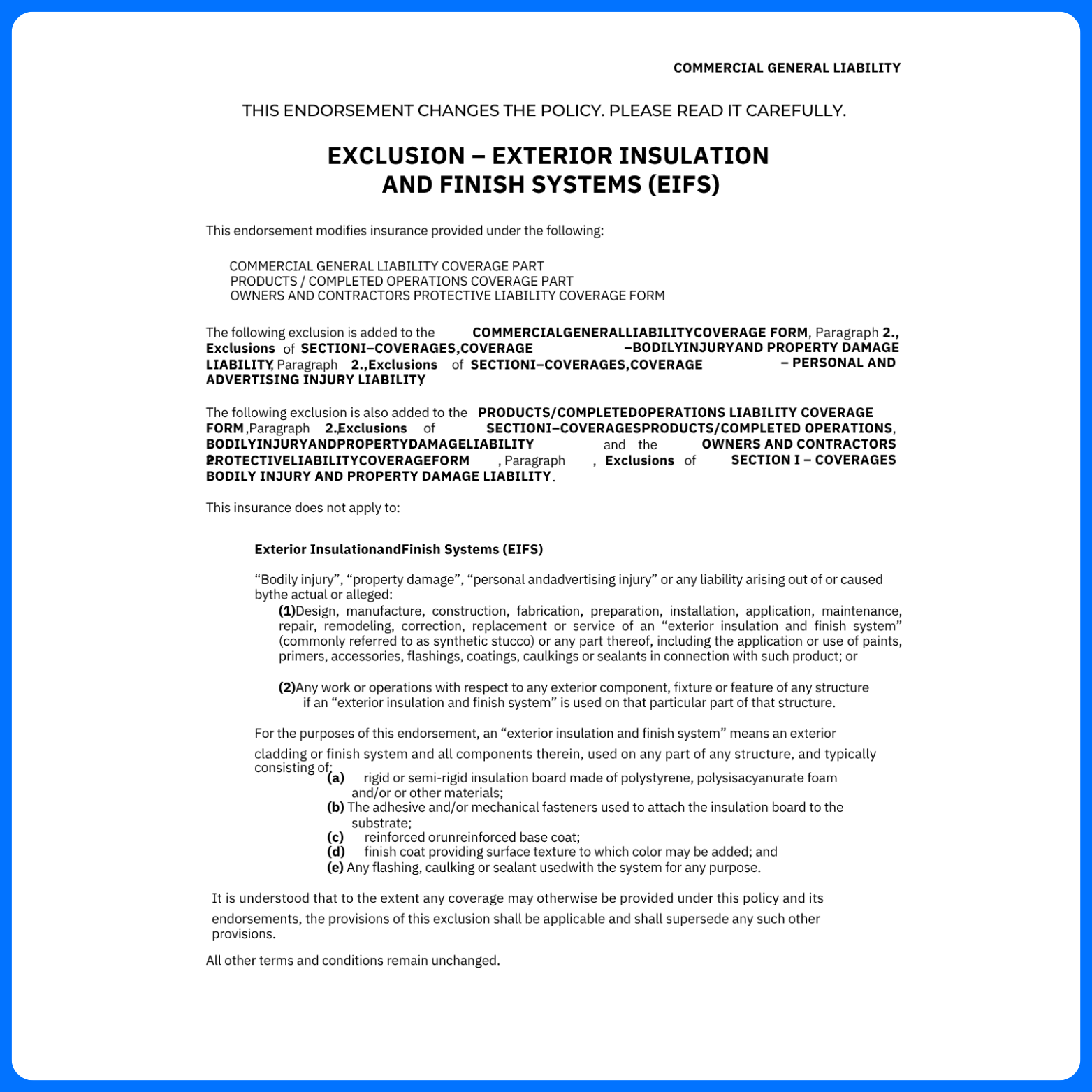

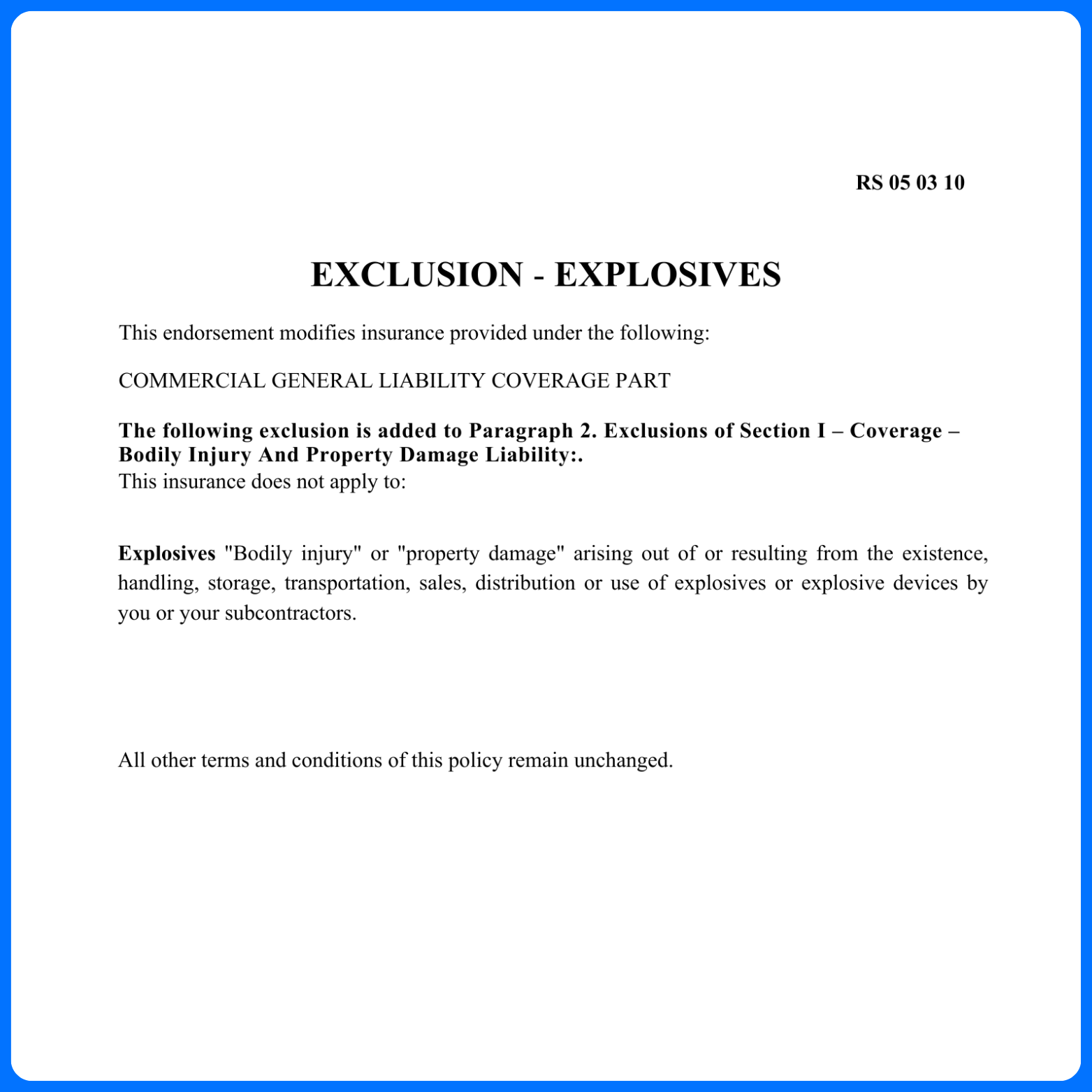

On page 75, we found the Exterior Insulation and Finish Systems exclusion. This is very common but might not apply for all subcontractors. For this specific one working with installation, it really applies. The insurance does not apply to bodily injury or property damage if the work is directly related to the exterior insulation finish system—design, manufacture, construction—or if you’re working with any exterior component used in a structure where exterior insulation and finish system exists. It’s not only if you’re working directly with EIFS, but if you’re also doing work on a structure that has it, that’s also a problem.

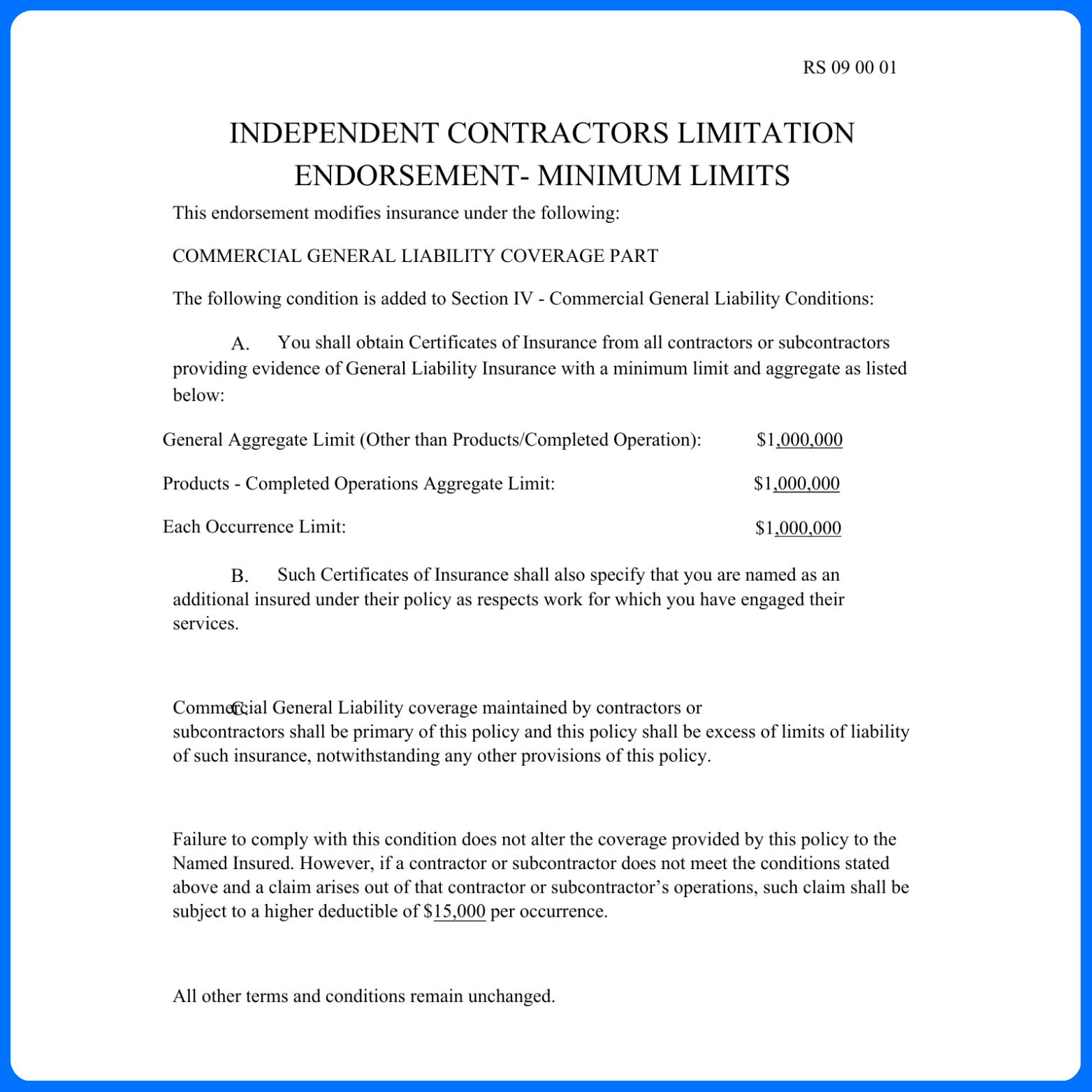

We have two ways of addressing policy review. Full policy verification means reviewing everything—telling you they have maybe 10 exclusions. It doesn’t mean for every project these exclusions are problematic. We’re giving you everything we find in the policy that’s problematic—any exclusions, provisions, clauses, even definitions. We review the whole thing, and if it limits coverage for the additional insured, we flag it as a gap. Customers have the ability to override exclusions that don’t present material risk to the project or job scope. When we’re doing full policy verification, we’re looking at everything—over 30 items for sure. Partial policy verification is a more strategic way. We’re collecting full policies, but customers pick up to five items—five exclusions or endorsements they want us to review.

Sometimes exclusions lurk in a small sentence here and there and change entire coverage. The normal ISO EIFS exclusion states: your product or work with respect to any exterior component, fixture, or feature is excluded if any exterior insulation finish system is used on that part of the structure containing the component you used. But the absolute one changes—any work or operations with respect to an exterior component, fixture, feature of any structure if EIFS is used on any part of that structure. You don’t need to be working directly in the part that has EIFS—if EIFS is anywhere on that structure, coverage doesn’t apply to that work.

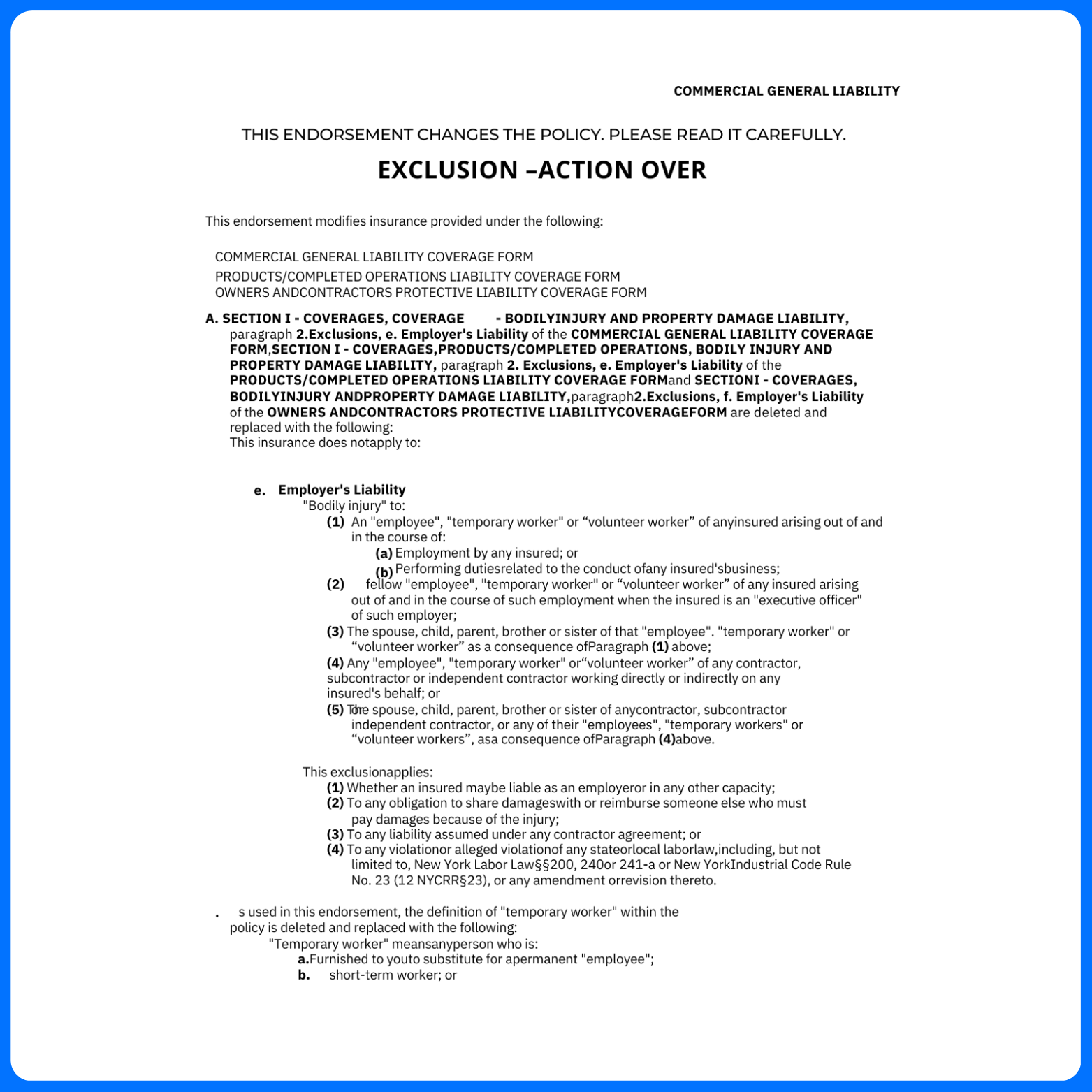

Most exclusions say it applies to the insured or anyone working on behalf of the insured—subcontractors, sub-subcontractors, independent contractors. Sometimes there’s a warranty endorsement asking the sub-subcontractor to comply with a series of insurance requirements. The carrier asks for a COI with specific limits and endorsements, and if that sub-subcontractor is not compliant, work is not going to be covered by the policy. Because the general contractor doesn’t have a contract with that sub-subcontractor and can’t know the requirements of the carrier, you have no control on whether those sub-subcontractors are compliant. More often we’re seeing that coverage does not apply—it’s full exclusion of coverage if they’re not compliant.

When you go into a general liability policy, there’s going to be classification of work performed by the subcontractor. Let’s say the classification is for interior painting, and if you’re not looking closely, they end up doing more than interior painting—they do exterior painting as well. Sometimes they have a classification limitation saying this insurance applies to your ongoing operations and completed operations only for specific work as described and scheduled below. If the subcontractor is not doing the work specifically described in the schedule of their classification, coverage is not going to apply.

We consider schedule of forms part of the policy review process. When you’re looking at schedule of forms, you’re identifying all these endorsements that could be problematic and have a sense of where you need to look. However, schedule forms could hide a bunch of scary exclusions that you’re not going to see the name there in the title. Example: the umbrella policy said “height restriction,” but the title was not height restriction—it was Designated Work. You would only see in the schedule of forms “Designated Work Exclusion” but you need to go into the policy and into the schedule box of the endorsement to find out there’s a height restriction.

We’re talking about policies and why reviewing policies is important, but we need to think about the process of transferring risk. The first thing you do is identify in your projects where you have exposure, where you have liability. It doesn’t matter if you’re reviewing policies and COIs if you’re not doing the second step: creating written contracts with hold harmless agreements, indemnification statements, and insurance provisions. A lot of the language in COIs and policies is important to vet, but a lot of that language goes back to the contract. If the contract doesn’t exist, it opens people to liability. There are different levels of effort to manage risk. It’s important you understand that having that certificate of insurance with the language you wanted, with the names of the additional insured, does not actually protect you as you think if you don’t have a written agreement.