How Jones Reviews Insurance Documents

The process our team of insurance document reviewers follows while checking COIs and endorsements sets us apart from our competitors. Part one of this blog covered the review of COIs and their limits for compliance, but didn’t cover endorsements. During the COI review process our auditors may see endorsements evidenced on the COI in various places, like checkboxes in the policy rows or in the description of operations (DoO) free text section.

Some of our customers do not accept the checkboxes or DoO for endorsements depending on their unique risk tolerances. In these cases they require copies of the endorsements. Fortunately, the Jones team are experts at reviewing endorsements for compliance. Their secret weapon? An index that makes quickly checking endorsements’ coverages simple, built out from years of handling insurance documents for customers.

The Jones Endorsement Index: Making Insurance Document Review Easier

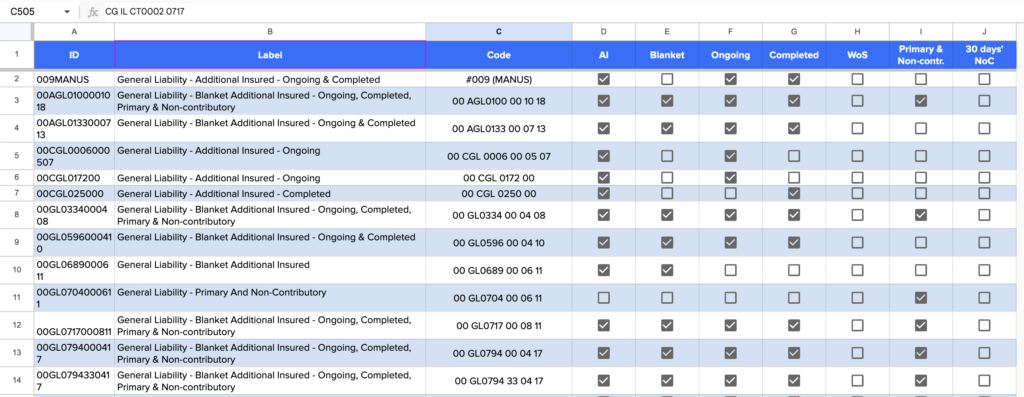

The Jones Auditing Team maintains an up to date endorsement index containing over 1,300 Commercial General Liability (CGL) insurance endorsements and their equivalents, broken down by whether they suffice for requirement types including Additional Insured, Waiver of Subrogation, blanket, ongoing and completed operations, Primary and Noncontributory, and 30 days Notice of Cancellations. Jones also tracks over 200 business owner policy, 300 automobile, and 30 Workers’ Compensation endorsements. This massive library of endorsements and their equivalents mean that no endorsement is too obscure for our team to quickly read and check for compliance.

Jones also works with our largest GC clients to build out organization-specific endorsement indices, broken down by insurance carrier, endorsement code, acceptability for the client, and additional auditing comments. Our level of familiarity with the standards of specific accounts means we always audit to the level of accuracy that our customers have come to expect from us, and our tracking system ensures that our no matter which one of our auditors is handling the account that they have relevant information at their disposal.

Equipped with this index, let’s follow Hisrain Reis, Insurance Policy Analyst at Jones, as he reviews a few tricky endorsements attached to a subcontractor COI for a GC client.

Checking General Liability Endorsements

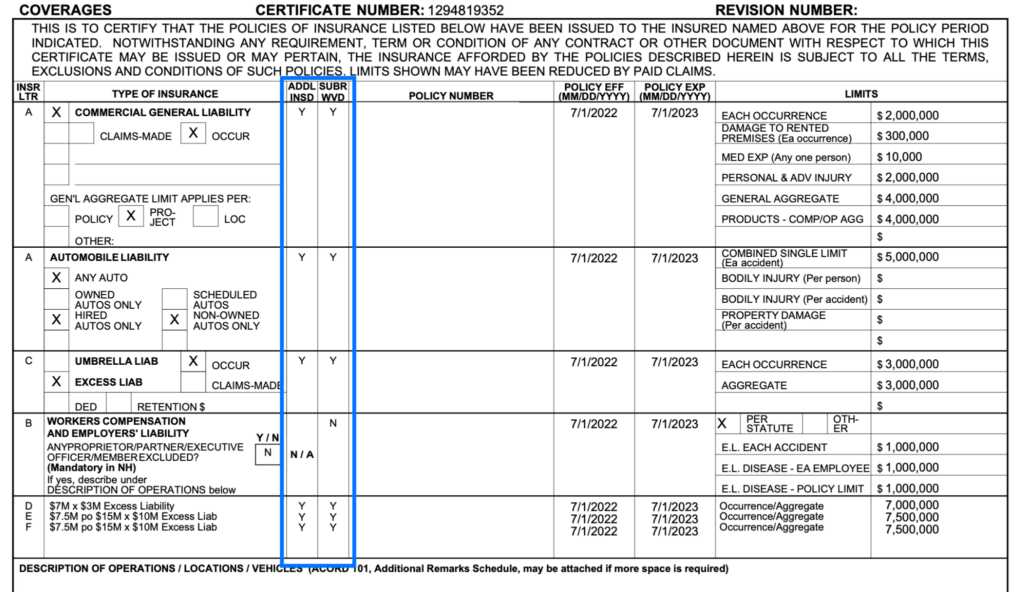

To set the stage, Hisrain has already reviewed the COI against insurance requirements, finding all the limits, insured name, certificate holder, and addresses compliant. The customer has a few specific requirements when it comes to endorsements that Hisrain is going to have to look out for as he checks them. For commercial general liability the customer requires:

Additional Insured for CGL

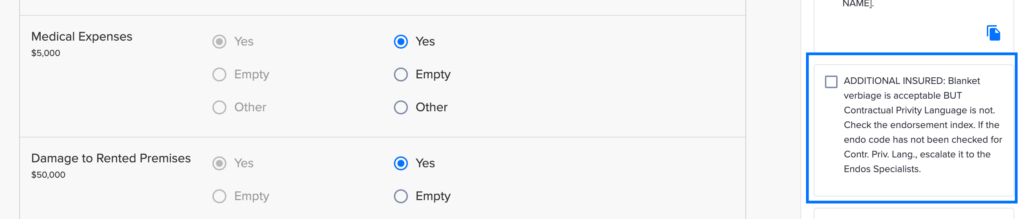

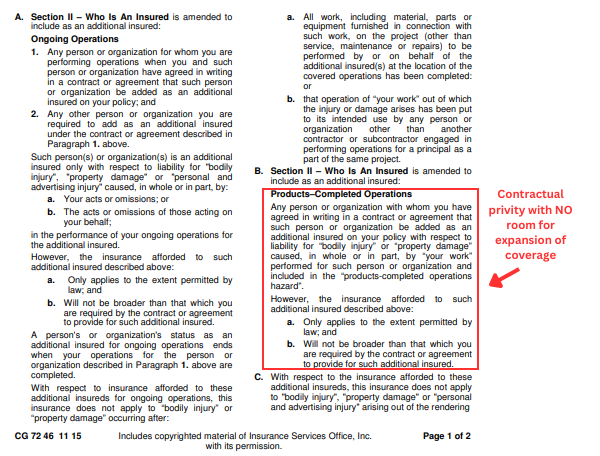

Additional Insured status is a key component of contractual risk transfer, and refers to the extension of coverage to a party not initially covered under the insurance policy. It is common practice for GCs to require that Additional Insured status on their subcontractors’ policies be extended to both them and the project owner. As evidence of the required Additional Insured status for this GC and owner the subcontractor provides Jones with a CG 72 46 11 15 endorsement.

Hisrain knows that this GC customer is very particular about contractual privity.

Contractual privity verbiage refers to language in endorsements that confers Additional Insured status to organizations that are parties on a written contract as “agreed in writing in a contract or agreement that such person or organization be added as an additional insured on your policy.” While this allows a GC to effectively transfer risk by being included in a subcontractor’s policy, it can leave a project owner at risk as they generally will not sign direct contracts with subcontractors. With that in mind, let’s look at this CG 72 46 11 15.

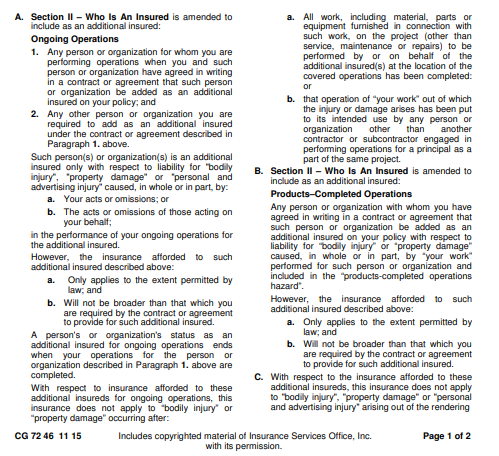

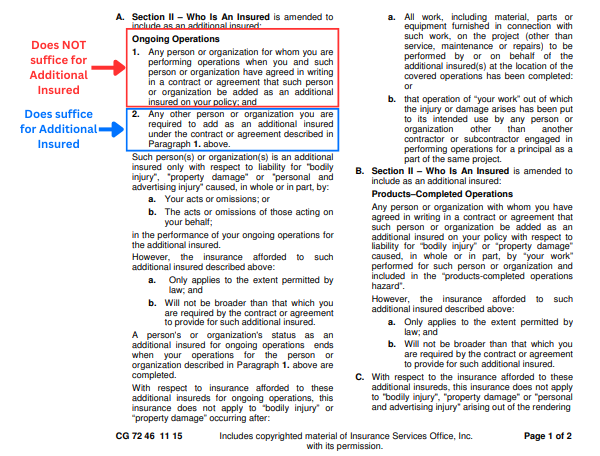

What jumps off the page at Hisrain? First section A. 1 makes reference to Additional Insured being conferred via contractual privity which is NOT good enough for the GC. Fortunately, A.2 of that section means Hisrain is able to mark COMPLIANT for Additional Insured for ongoing operations.

But wait- what about completed operations?

As we can see, the same contractual privity verbiage exists in the endorsement. However, while Section A.2 confers Additional Insured status to the project owner, the lack of a similar extension for completed operations means Hisrain is going to mark this NONCOMPLIANT for missing Additional Insured for completed operations for the owner. The coverage gap of not extending the Additional Insured to the owner for completed ops is not a tolerable gap for the GC.

Waiver of Subrogation for CGL

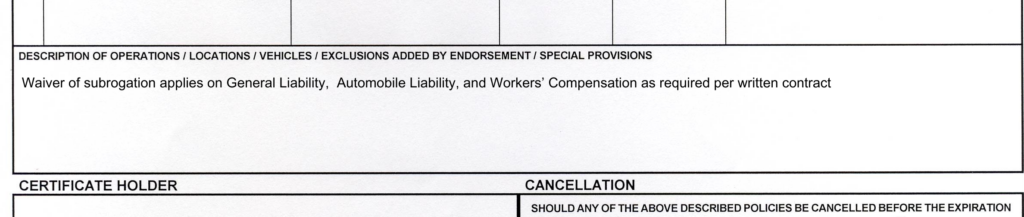

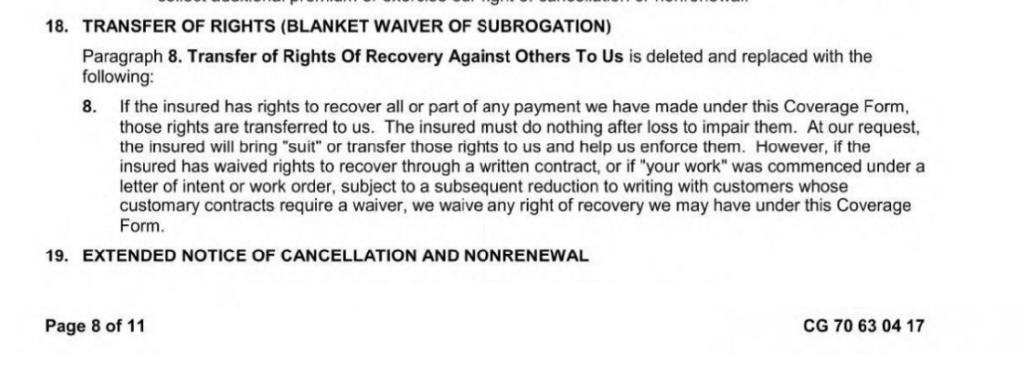

A WoS endorsement prevents an insurer from seeking recovery from a third party for damages paid in the event of a claim. Most GCs require waiver of subrogation provisions in subcontractor insurance policies to insulate themselves from risk. As evidence of a WoS the subcontractor in today’s example has provided Jones with a CG 70 63 04 17.

Hisrain checks the endorsement index and sees that this suffices the requirement for a WoS. The verbiage in the following section waives the right of the insurance carrier to seek redress or seek compensation for losses from a negligent third party as per the customer’s requirement, so Hisrain marks it COMPLIANT.

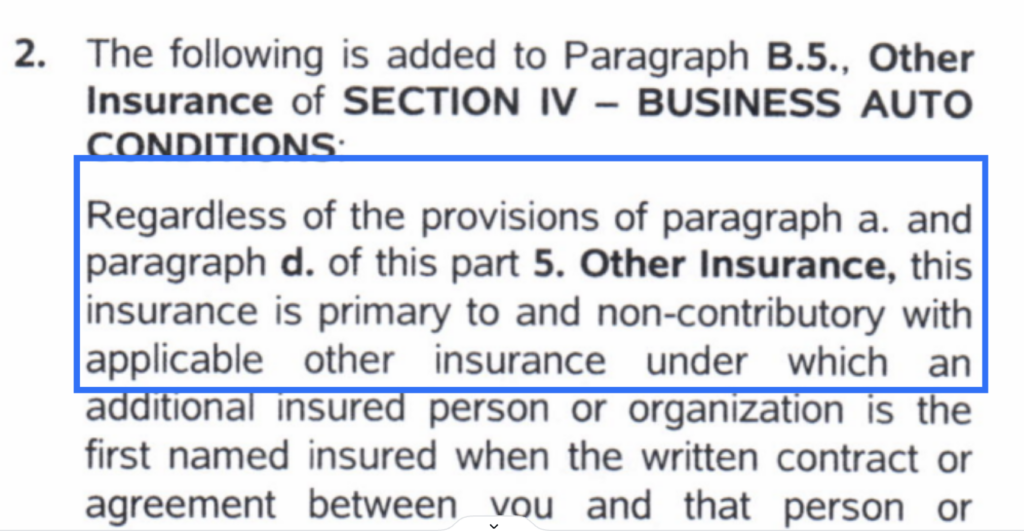

Primary and Noncontributory for CGL

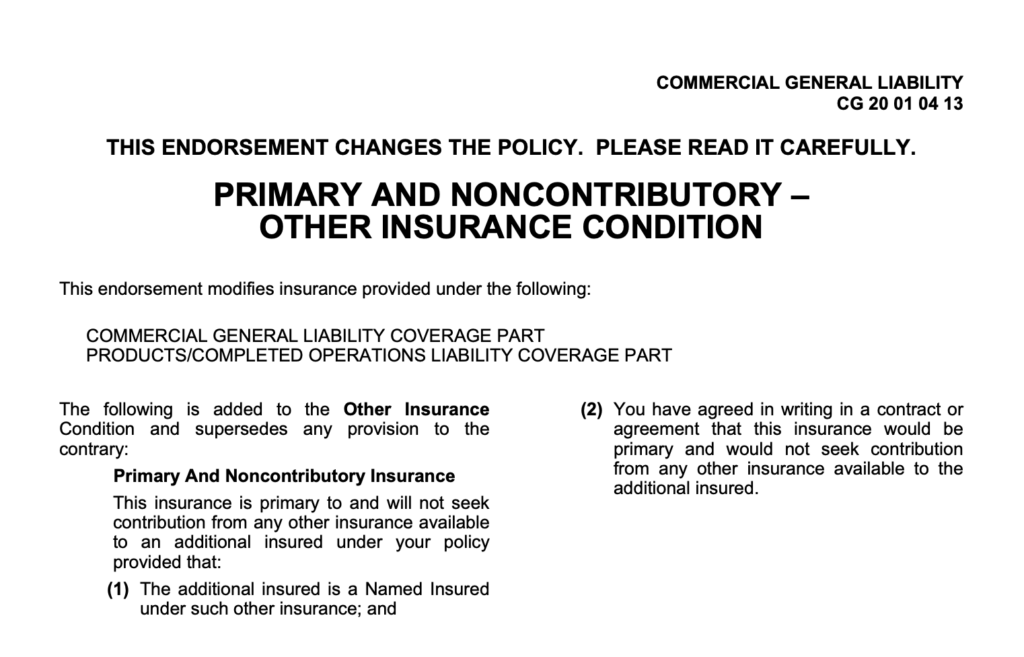

Requiring subcontractor insurance policies to be PNC allows GCs to effectively transfer risk downstream by ensuring the subcontractor’s insurers are first to pay (primary) in the event of a claim, as well as pay without seeking contributions from the GC’s insurer (noncontributory). To evidence this the subcontractor has provided a CG 20 01 04 13 endorsement for Hisrain to check.

This endorsement is relatively straightforward and simple so Hisrain has no problem marking it COMPLIANT.

So, to summarize the endorsements for general liability:

- Additional Insured endorsement CG 72 46 11 15 is COMPLIANT for ongoing operations and NONCOMPLIANT for completed operations

- WoS endorsement CG 70 63 04 17 is COMPLIANT

- PNC endorsement CG 20 01 04 13 is COMPLIANT

Now that he’s finished reviewing all the CGL endorsements for compliance Hisrain is going to move on to the endorsements to umbrella liability.

Checking Umbrella Liability Endorsements

Umbrella liability helps protect GCs from claims by providing additional coverage in the event that the primary coverage, whether it was CGL, automobile, or Workers’ Compensation, exhausts its limits. In this case, umbrella coverage would then cover any additional claims or fees up to its own limits. Like CGL, umbrella liability can also be altered or amended by endorsements. We don’t see many endorsements for umbrella liability, and generally changes to umbrella policies will be indicated either on the COI itself or via a follow form endorsement. In today’s simulated document review the GC customer requires several alterations to the subcontractor’s umbrella liability, including:

- Waiver of Subrogation

- Primary and Noncontributory

- A follow-form endorsement

Hisrain starts with the WoS endorsement.

Waiver of Subrogation and Primary and Noncontributory for Umbrella Liability: What do we do now?

Our customer requires a WoS and PNC for subcontractor insurance policies. When Hisrain goes to review the endorsements he finds that only one has been attached to the COI for umbrella liability and that there are no specific endorsements for either WoS or PNC. Does this mean Hisrain is going to mark them noncompliant? First, let’s turn to the one endorsement that was included for umbrella.

Follow Form Endorsements for Umbrella Liability

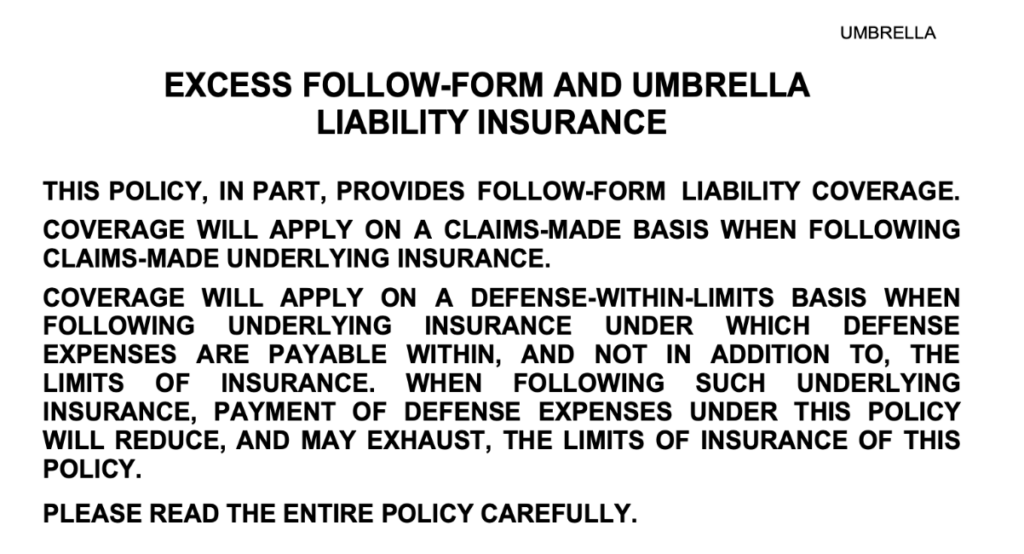

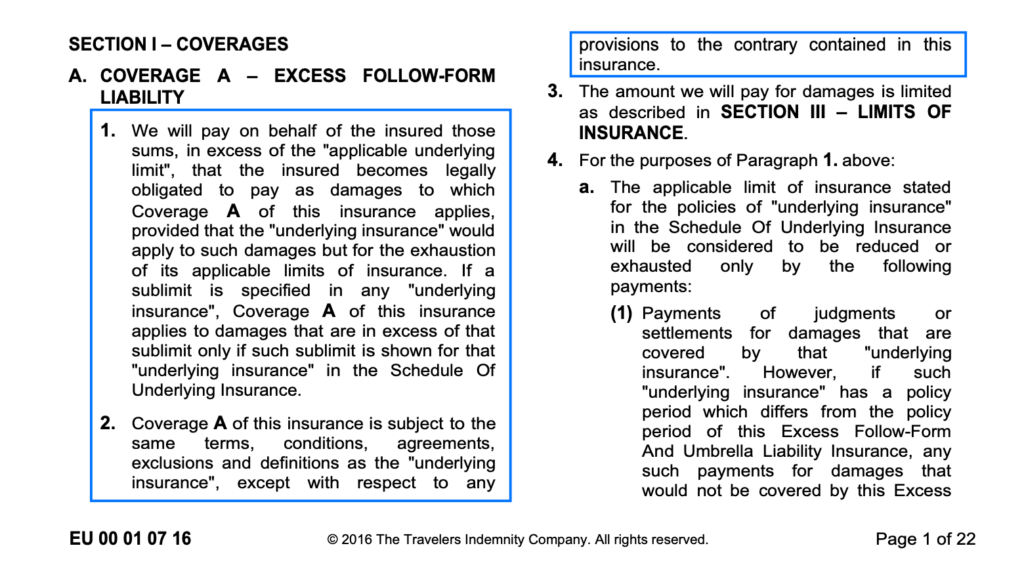

Hisrain is well acquainted with the one endorsement the subcontractor provided, a EU 00 01 07 16, and knows that it will help him resolve compliance for all the endorsements required for umbrella liability. That’s because the EU 00 01 07 16 is what’s known as a follow-form endorsement, one that amends the scope of coverage to exactly cover the “underlying insurance” that it’s extending.

Follow-form endorsements are a useful tool to ensure the coverage of the umbrella or excess liability perfectly fits over the other coverages it’s supplementing, either CGL, automobile, or workers’ compensation. The way it refers to the “underlying insurance” indicates that any damage that would be covered by that insurance but extends beyond the limits of coverage would subsequently be covered by the excess liability. This endorsement changes the verbiage of the umbrella policy to exactly follow the verbiage of the policy it is serving to extend the coverage limit of.

The existence of the follow-form endorsement indicates to Hisrain that the umbrella liability contains a WoS as well as is PNC due to the fact it follows the form of the CGL policy and its previously reviewed endorsements. With this in mind, Hisrain is going to mark all required endorsements for umbrella liability COMPLIANT.

- WoS, follow-form, and PNC are COMPLIANT due to endorsement EU 00 01 07 16.

From here, Hisrain progresses to reviewing automobile liability.

Checking Automobile Liability Endorsements

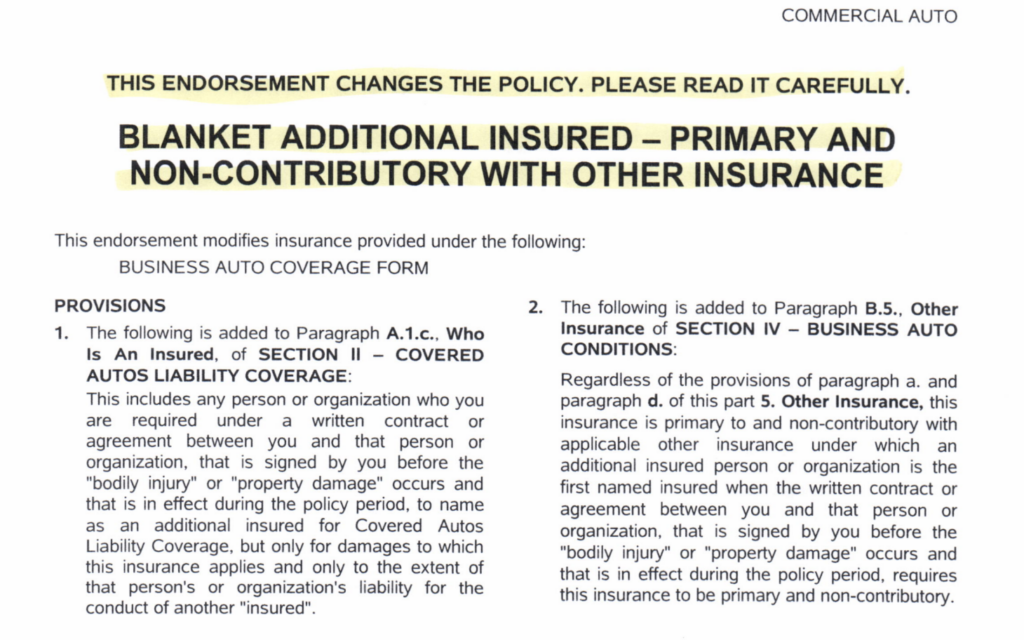

Automobile liability coverage covers the usage of vehicles in commercial operations, as opposed to personal usage of a vehicle. These coverages generally have higher limits than personal automobile liability, and cover a wider variety of vehicles, like hired, owned, and non-owned autos. Hisrain has already ensured the automobile liability coverage evidenced on the COI surpasses all the required limits, as well as meets the category requirements as provided by our GC customer. As was the case with umbrella and CGL, our customer has specific requirements for automobile liability endorsements. In this case they require:

- Additional Insured status for them and the project owner

- Primary and Noncontributory

- Waiver of Subrogation

To provide evidence of these the subcontractor has provided a CA T4 74 02 16 endorsement.

The blanket Additional Insured verbiage featured in this example is by default not accepted by Jones insurance document reviewers, as accepting this broad extension of Additional Insured does not fit the unique risk appetites of certain customers. However, the GC Hisrain is reviewing insurance documents for today is willing to accept this verbiage as they find it an effective method to reduce risk while boosting compliance rates and minimizing impact on day to day business operations.

After confirming that this endorsement is COMPLIANT for Additional Insured Hisrain moves onto PNC. He quickly finds verbiage indicating that the policy is in fact PNC, and marks that COMPLIANT as well.

However, upon finishing review of the endorsement Hisrain notices that it lacks a WoS, or any verbiage suggesting the insurer will relinquish the right to seek recovery from a third party for damages paid in the event of a claim. A quick review of our endorsement index confirms that it lacks a WoS, so Hisrain marks that gap.

-

- Additional Insured and PNC are COMPLIANT from endorsement CA T4 74 02 16

- WoS is NONCOMPLIANT on endorsement CA T4 74 02 16

From here Hisrain will move onto the last policy he needs to check endorsements for, Workers’ Compensation.

Checking Workers’ Compensation Endorsements

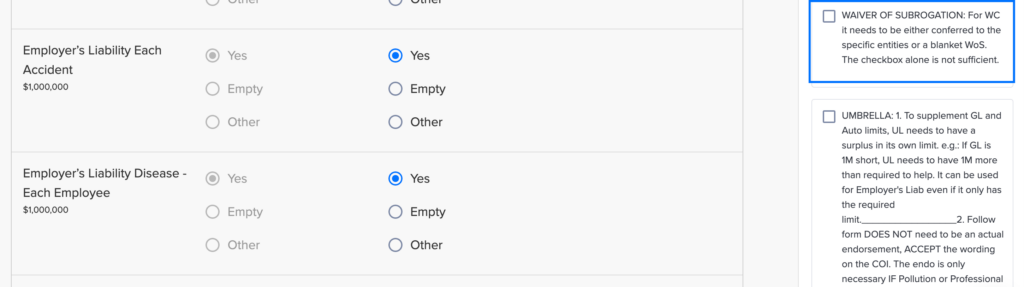

Workers’ Compensation covers employees’ lost wages and medical expenses due to injury on the job, ensuring that injured or sick workers are able to receive the wages they need without negatively impacting business operations. This coverage is no fault, and statutory limits for minimum coverages are generally defined on a state to state basis. Hisrain has already confirmed that the limits meet the statutory limits, so he’s going to move onto the endorsements required. For Workers’ Compensation, our customer is strict when it comes to their WoS and will not accept the checkbox as evidence.

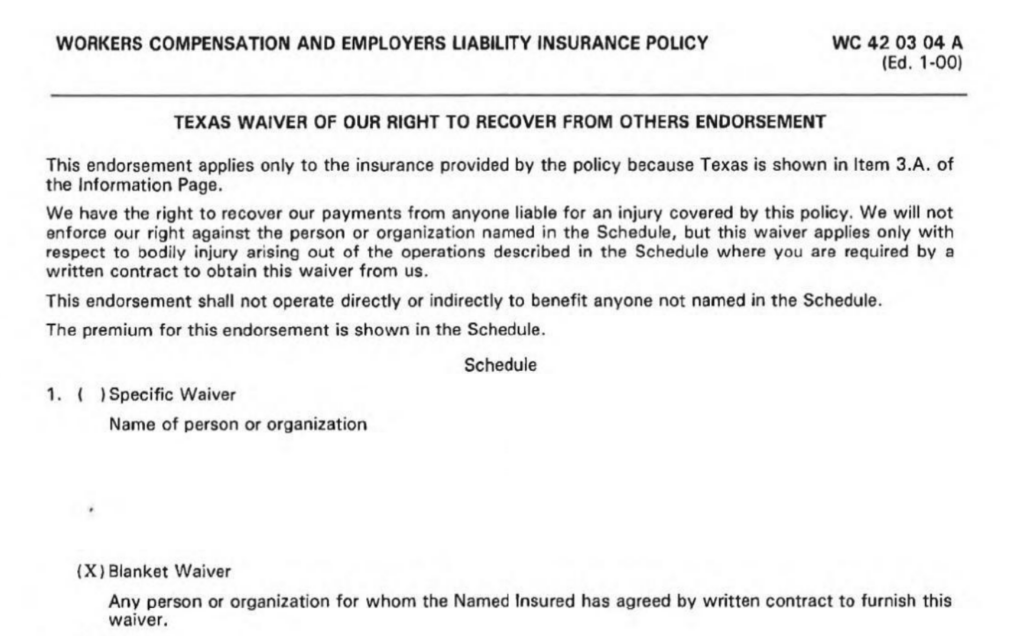

Hisrain turns to the provided WC 42 03 04 B to check it for compliance.

Waiver of Subrogation

The WC 42 03 04 B endorsement provided by the subcontractor is a Texas specific endorsement as Workers’ Compensation is regulated on a state by state basis as discussed prior.

As Hisrain can see from this endorsement, the subcontractor has extended Workers’ Compensation as required via a blanket waiver. This does suffice for the WoS requirements as the customer defined with Jones, so Hisrain goes ahead and marks it COMPLIANT.

- Workers’ Compensation endorsement WC 42 03 04 B is COMPLIANT for waiver of subrogation.

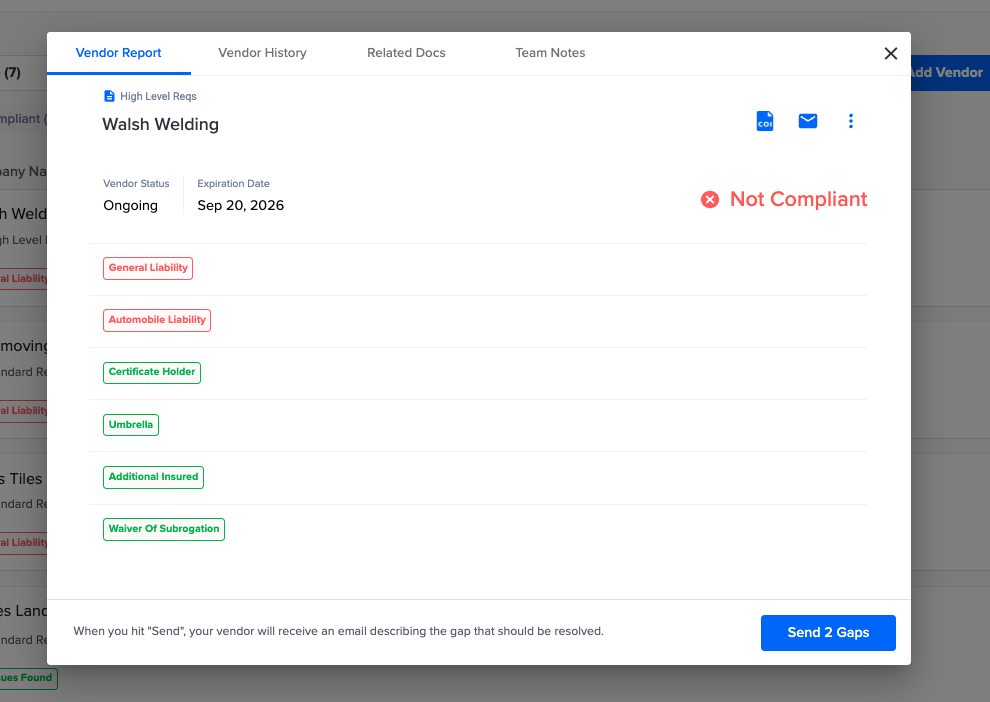

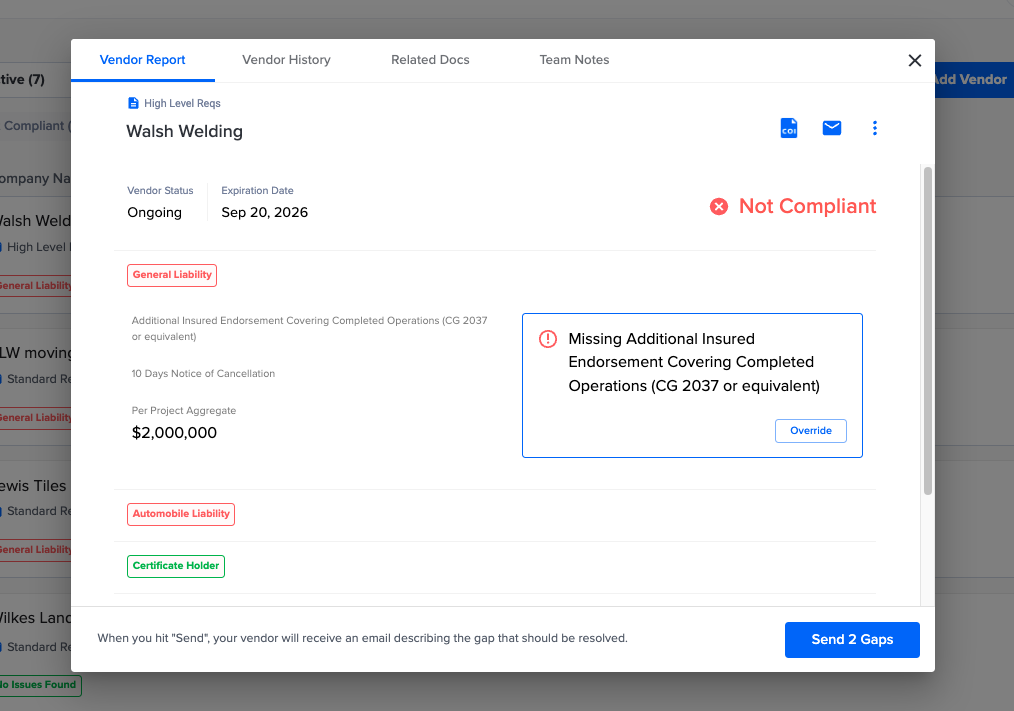

Communication of Gaps

Now that Hisrain has finished reviewing the endorsements attached to the subcontractor’s COI, he’ll go ahead and generate a report that highlights the gaps to the admin in charge of COIs at the GC. From there, they’ll have the option to waive, accept, or send gaps to the subcontractor. Jones’ easy to understand dashboard makes understanding and managing gaps far easier than manually tracking them in spreadsheets and emailing out gaps.

Why You Should Trust Jones with Your COIs and Endorsements

Our knowledge of GC specific workflows and ability to accurately review complicated endorsements makes Jones the best choice for risk-focused construction organizations. Trusting “the other guys” with the review of your insurance documents leaves your company exposed to risk due to the lack of granular COI and endorsement review standards. You need a COI and subcontractor compliance management tool that is willing to understand your unique risk tolerance and review documents to your required standards, not implement a one size fits all approach that fails to protect your company from claims. GCs like SavCon, Harvey-Cleary, Bulley and Andrews, Manhattan Construction and more have chosen Jones because of how we effectively bring together software and insurance expertise to help derisk their projects and support their insurance compliance strategies. Plus, faster compliance can improve construction accounts payable. Get in touch with us below to find out more about bringing Jones on to support your insurance risk strategy today.