What Is a COI in Construction?

A certificate of insurance is a summary document issued by an insurance broker that shows proof of insurance coverage. In construction, it’s typically required from subcontractors, vendors, and any third parties working on a job site.

It includes:

- The name of the insured (your subcontractor or vendor)

- Types of coverage (e.g., General Liability, Workers’ Comp, Auto)

- Policy numbers and insurance carriers

- Effective and expiration dates

- Coverage limits

But here’s what it doesn’t do: guarantee compliance.

The COI is only a summary. It doesn’t prove that the required endorsements are in place. It doesn’t confirm that the owner or GC has been added as an Additional Insured (unless that status is backed by a formal policy endorsement, such as a blanket Additional Insured endorsement). It doesn’t show exclusions that might gut coverage. And yet, it’s the most relied upon document in insurance compliance workflows.

This reliance on an incomplete document is one of the biggest pitfalls in construction compliance. Without supporting endorsements or policy details, teams are making approval decisions based on surface-level data – a risky move when millions of dollars are on the line.

Jones helps solve this by complementing COI management with full policy verification (e.g. flagging exclusions like Height or EIFS), reviewing endorsements, checking AM Best Ratings to ensure carrier solvency, and incorporating Indemnification Agreement workflows to strengthen risk transfer.

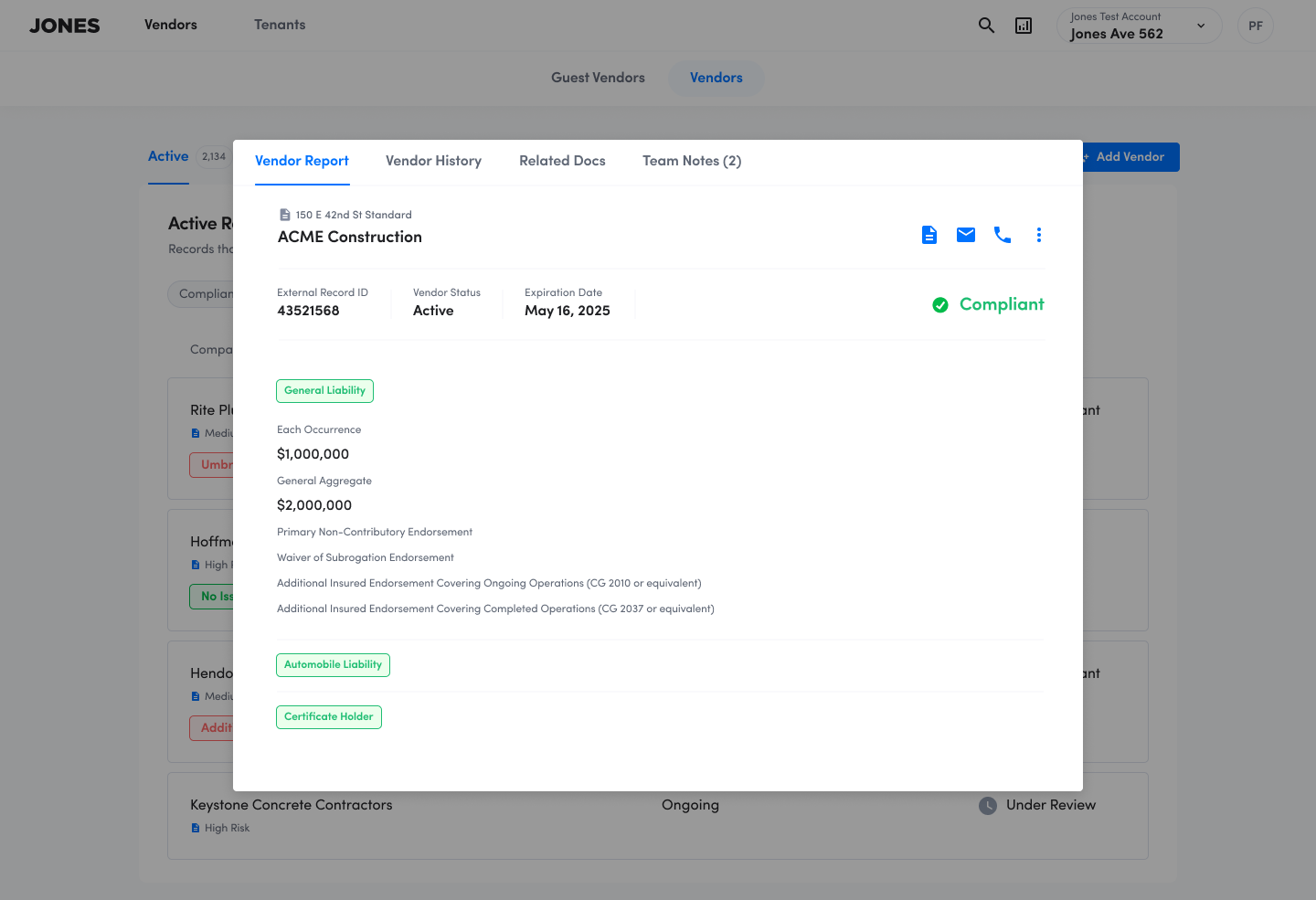

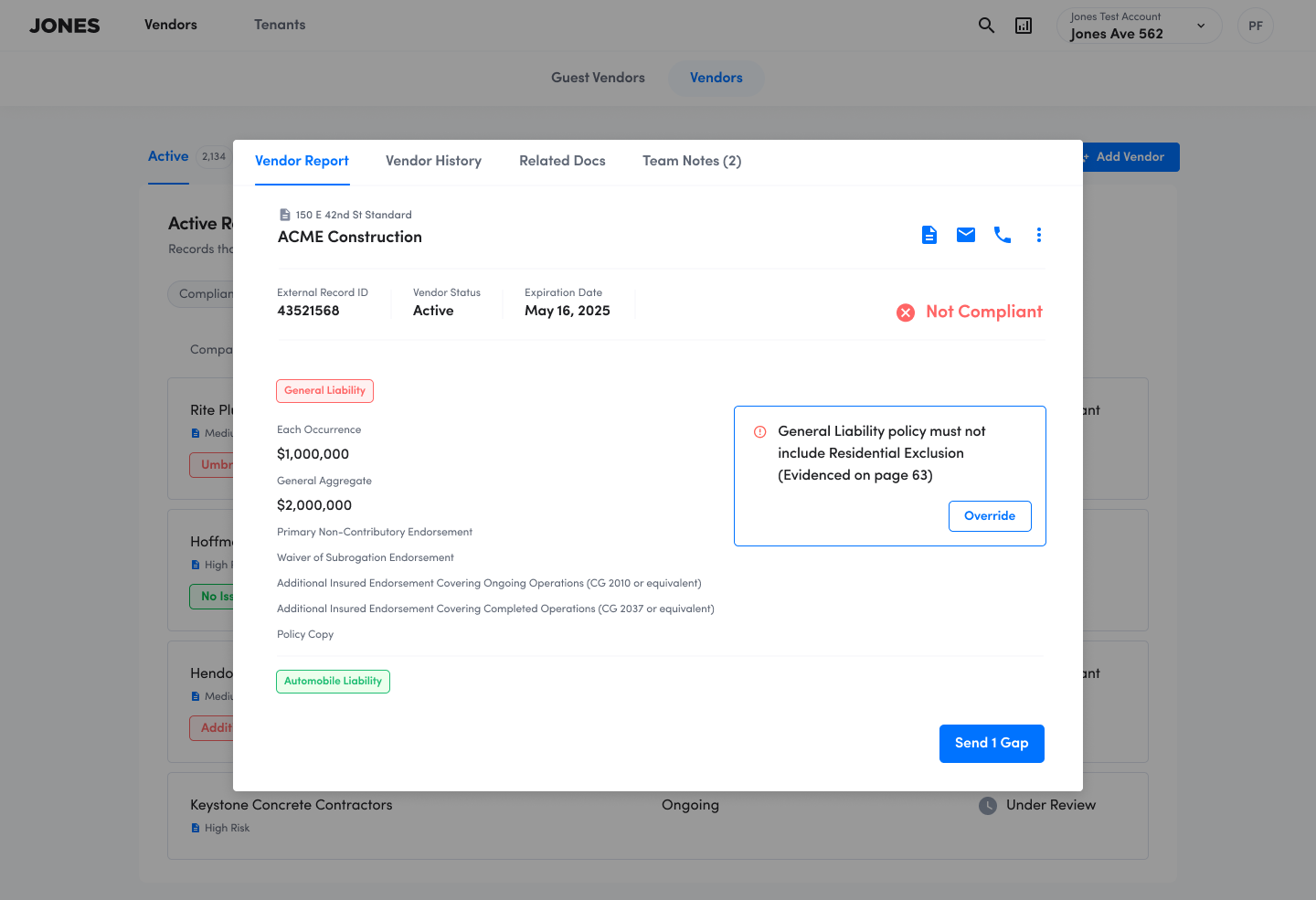

In an example below, a COI appears as fully compliant with a company’s insurance requirements. However, upon checking the full policy, it’s clear that the subcontractor’s General Liability policy contains Residential exclusion.

ACME Construction’s insurance: only COI is checked for compliance

ACME Construction’s insurance: full CGL policy is checked for compliance

Note: Ready to explore how Jones can improve your COI management process? Talk to our team of experts today!

Why COIs Are Essential, But Not Sufficient

In a perfect world, every vendor would have a comprehensive policy tailored to your project’s needs. But in reality, insurance programs vary wildly. Some vendors work across states or trades. Others purchase cheap policies with narrow coverage to meet bid requirements.

The COI is the gatekeeper. If a subcontractor can’t provide a COI that aligns with your project’s contractual insurance requirements, they shouldn’t be on the job. That’s not legal paranoia. It’s a contractual obligation.

In fact, most construction contracts include specific insurance language, often requiring:

- $1M/$2M+ General Liability limits

- Commercial Auto and Umbrella/Excess coverage

- Workers’ Compensation with statutory limits

- Additional Insured status (CG 20 10 and CG 20 37)

- Waiver of Subrogation

- Primary and Non-Contributory language

These insurance requirements may differ depending on the subcontractor’s scope of work. For example, requirements such as Professional Liability or Pollution Liability only apply to subcontractors performing certain types of work.

Jones configures insurance requirements based on your company’s risk management strategy (e.g., one set of rules for Wrap subs and another for Non-Wrap subs). We will also conduct an Auditing Standards Review call to align on the review rules and how strictly your company wants to enforce compliance.

How how we customize review rules for Additional Insured:

Client 1’s rules: Checkbox in the AI column must be marked

Client 2’s rules: AI must appear on all three places:

The Description of Operations

AI Endorsement for Ongoing Operations

AI Endorsement for Completed Operations

Once the requirements and process are established, Jones will review COIs, endorsements, and insurance policies for compliance, flagging every missing detail.

Where COI Workflows Break Down

Superficial Review

Many firms rely on a basic checklist (expiration date, General Liability, and Workers’ Comp), and approve subcontractors without checking limits or endorsements. But if the named insured doesn’t match, or the endorsements are missing, the document may be meaningless during a claim or an external audit.

Jones addresses this by applying a two-level full compliance verification for all our customers. It includes OCR technology and a review by the Jones COI review experts who are trained in construction-specific policies and forms. In these blog posts, you can learn more about how we train our COI review experts and how we approach verification of endorsements.

No Review Standards

In some firms, internal teams are not fully aligned on how to interpret insurance requirements.

Jones enforces uniformity so that your organization’s compliance standards are enforced consistently.

No Audit Trail

Without documentation detailing who approved a COI and why, teams are left vulnerable. Verbal sign-offs and email chains don’t cut it.

Jones creates a clear, timestamped record of every COI submission, review, and approval, giving risk leaders full visibility and defensibility.

COI Compliance = Operational Discipline

A true COI compliance program isn’t about collecting paper. It’s about:

- Complementing it with other risk transfer strategies such as full policy verification and enforcement of contract terms

- Systematizing document review

- Tracking and surfacing exceptions

- Demonstrating due diligence

Jones makes this possible without adding headcount by centralizing intake, enabling fast, accurate verification for compliance, and enabling jobsite-to-backoffice visibility.

Instead of digging through emails or spreadsheets, teams can log into Jones and see which vendors are cleared, which are pending, and which are non compliant and need to provide an updated COI before being allowed to a jobsite.

How Jones Powers a Modern COI Workflow

Here’s how leading general contractors (such as Harvey-Cleary, Manhattan Construction, and others) are using Jones to upgrade their COI process:

Structured and Easy COI collection

Vendors upload their COIs to Jones without having to login. The process is frictionless to ensure that the fastest collection of insurance documents. (As of May 2025, Jones also offers a guaranteed 90% collection to customers on our Jones Operator AKA Concierge plan).

Full-Service Compliance Checks

Jones verifies every detail on subcontractors’ COIs and endorsements, including expiration dates, coverage limits, and required policy types. It flags inconsistencies, expired policies, and mismatched names. We use OCR technology and AI, but every set of insurance documents is also routed to Jones’ expert reviewers. Our SLA to review a subcontractor’s insurance is under 24 hours (although in practice it’s oftentimes under 5 hours), and our accuracy is at 99.96%.

Procore, CMiC, Sage Integrations

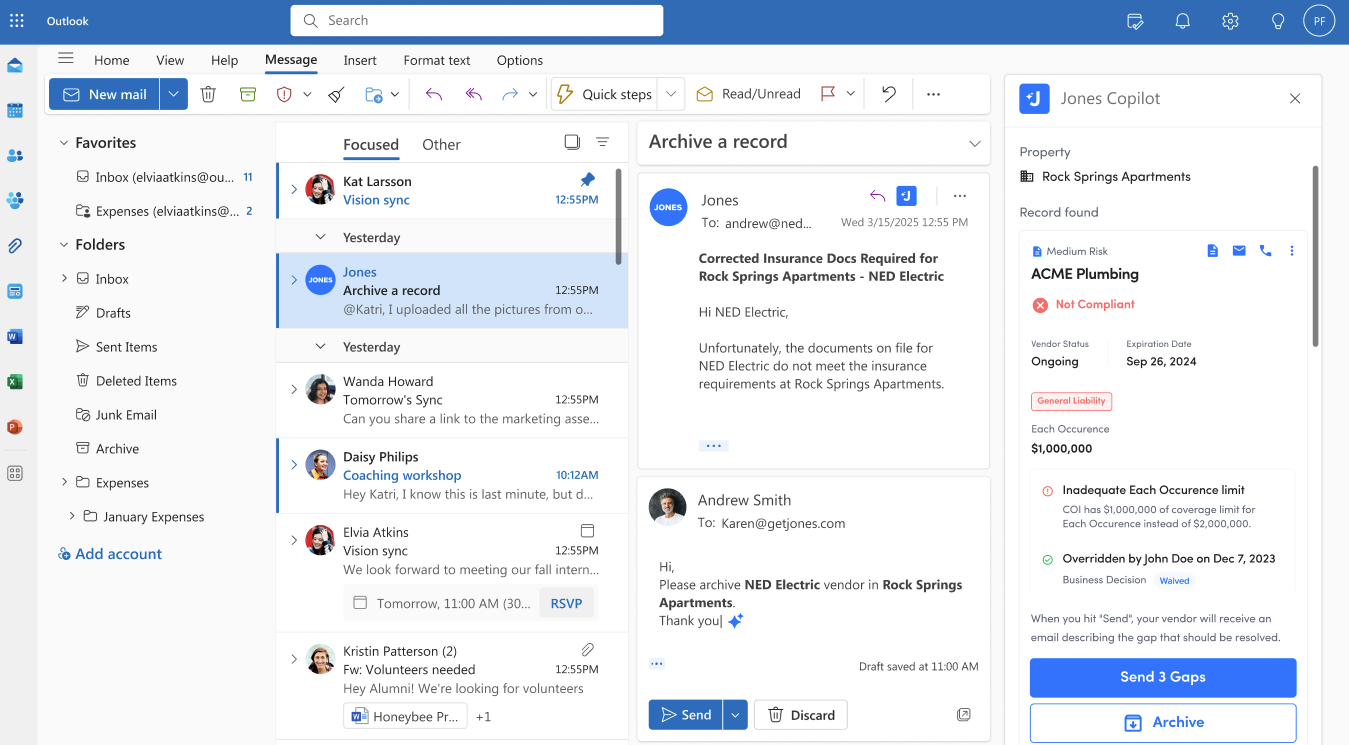

Jones connects directly to the tools your teams already use, so no duplicate data entry is needed. Our latest product updates include Procore Side Panel and Microsoft Outlook Copilot – these tools let you take key insurance compliance actions such as Request a COI without having to log into Jones.

Microsoft Outlook Copilot enables clients to instantly view compliance reports, gaps, and issues—all without leaving Outlook:

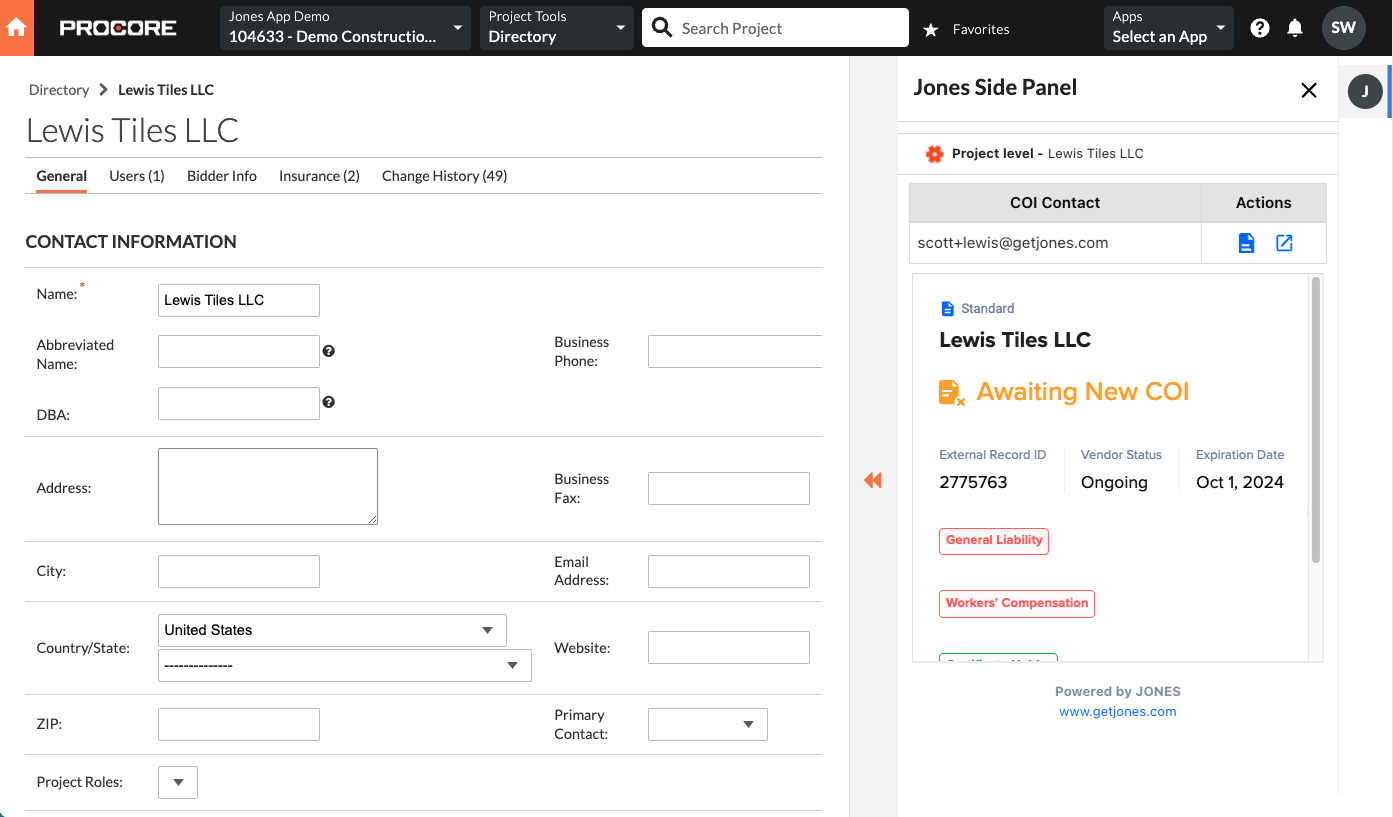

Procore users can manage compliance via Jones Side Panel app:

Full Audit Logging

Every action – COI submissions, review results, waivers, and approvals – is logged, creating a bulletproof compliance trail for internal or external review.

Real-World Results from Jones Customers

Manhattan Construction sped up payments to subcontractors by a week, improved insurance compliance to 90%+, and reduced time spent on COI-related tasks by 50%.

Bogard Construction saved almost 2,000 hours a year and dramatically reduced their risk exposure thanks to Jones.

Tired of Reviewing COIs and Endorsements Manually?

Jones automates the collection and review of COIs for property management companies, owner-operators, and general contractors across the US. Reach out to us via the form below to find out more about how Jones can help your organization manage your insurance documents.