The owner-operator’s insurance compliance process after onboarding Jones was well developed. They were collecting third-party insurance documents, everything was being reviewed for compliance by Jones within 24 hours, and coverage gaps were being highlighted and explained to third-parties in emails. This process helped them almost double their insurance compliance percentage…but then it plateaued at around 40 percent.

It became clear that in order to boost insurance compliance rates further, the company needed to make changes to their insurance risk strategy.

In situations like this, Jones Risk and Compliance team is available for strategy calls, where they conduct deep dives into portfolio insurance compliance data, make best practice recommendations, and suggest alterations to insurance risk strategy. Some recommendations may include adding/removing requirements, or implementing a more lenient waiver plan.

The company booked a call with Jessica Lopes, Director of Risk and Compliance at Jones, to understand why their portfolio’s insurance compliance percentage had stopped moving upwards.

Note: interested in exploring how Jones can help you automate your compliance management end-to-end and de-risk your buildings? Talk to our team of experts today!

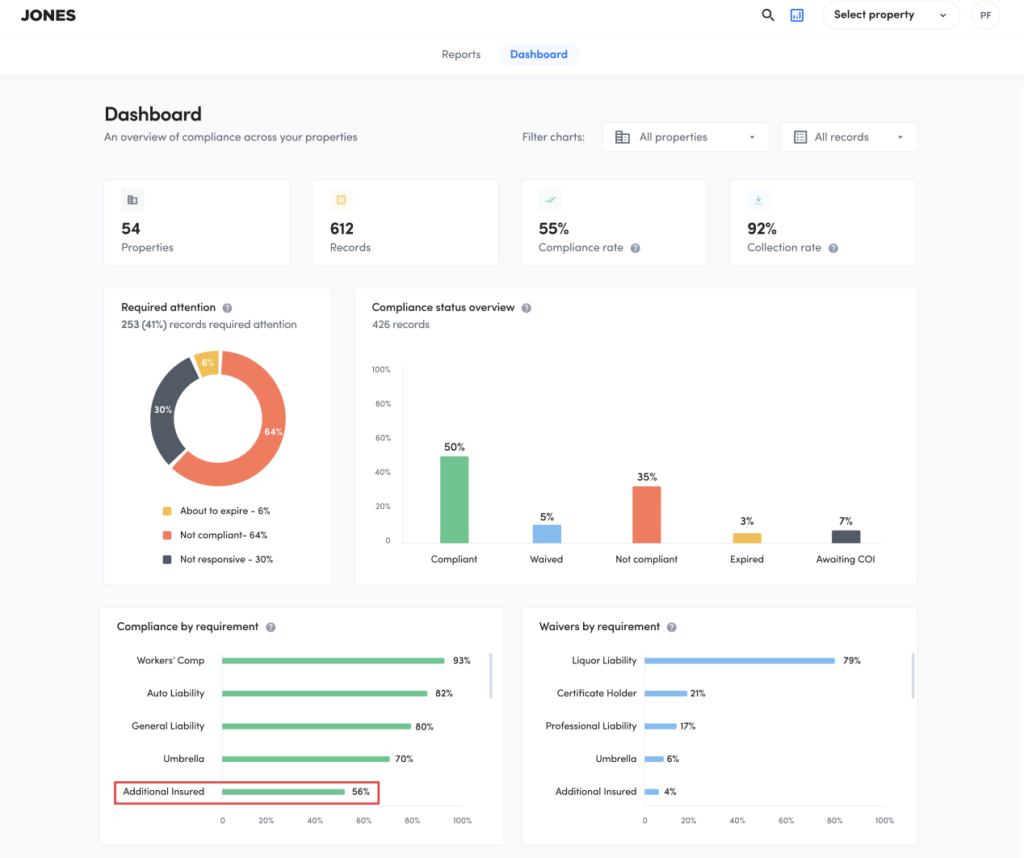

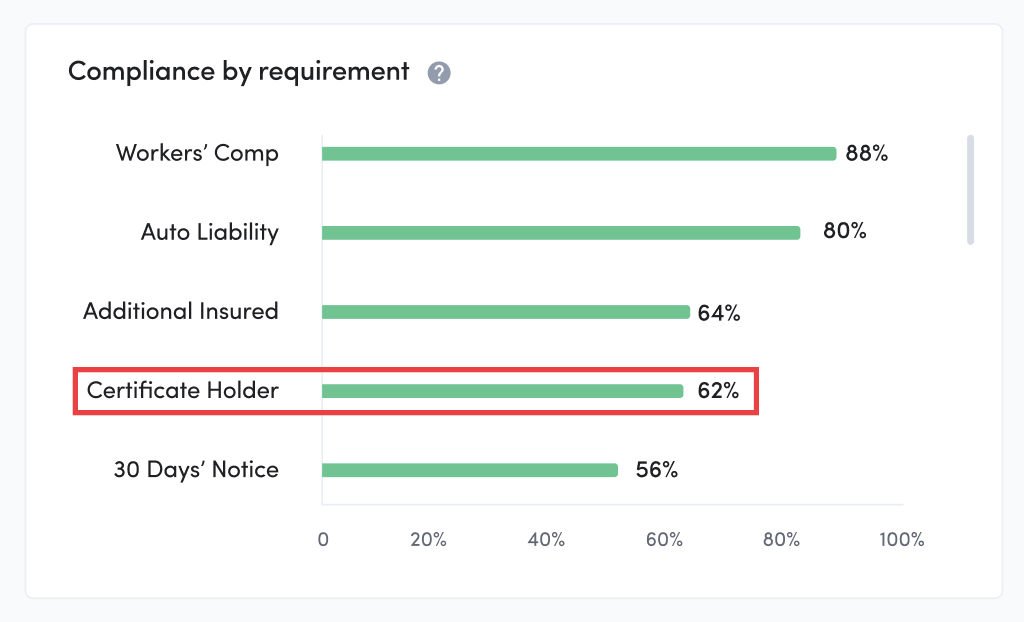

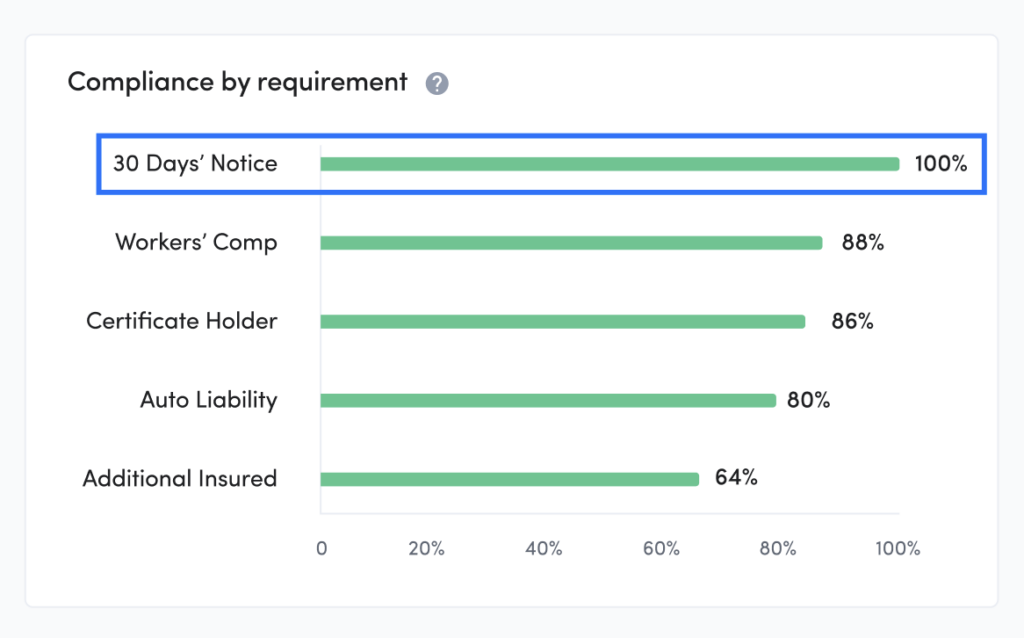

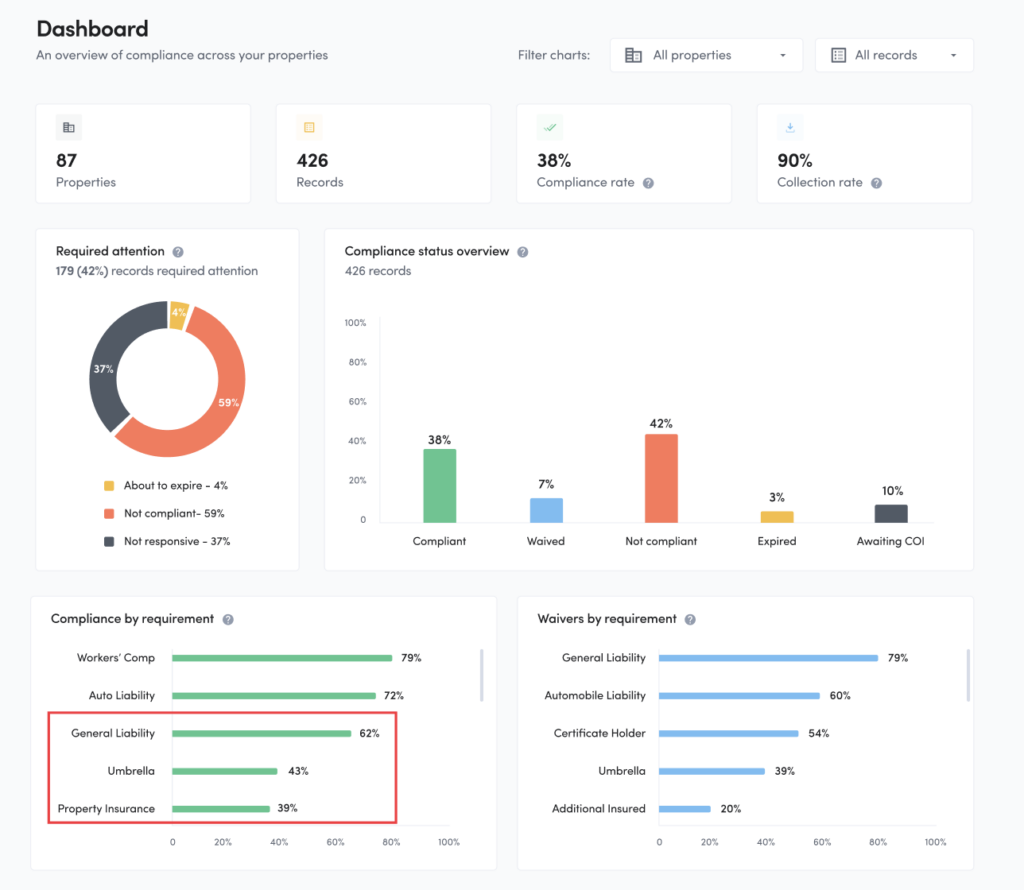

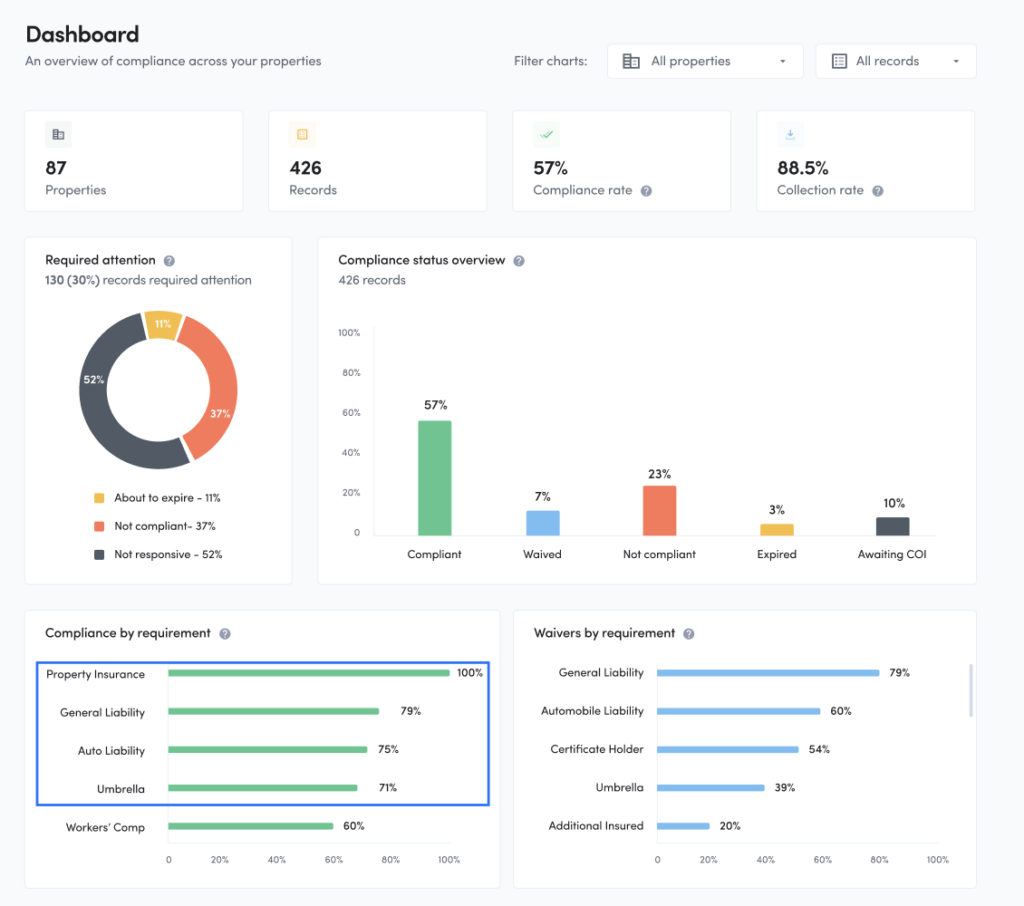

How Their Initial Portfolio Compliance Looked

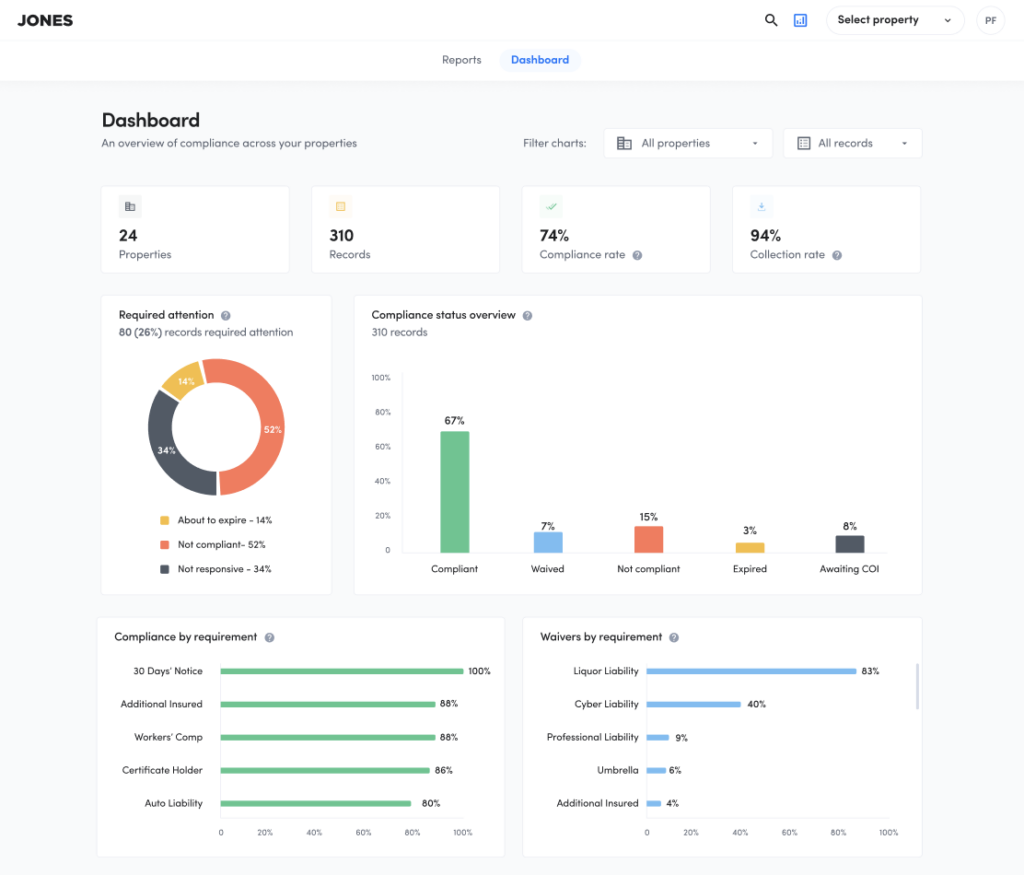

From the company’s analytics dashboard, Jessica quickly identified three main culprits for the lower than hoped compliance stats:

- Property Insurance and Umbrella Liability: Compliance rates below 50 percent.

- Commercial General Liability: Compliance rate was also lower than ideal at only 62 percent.

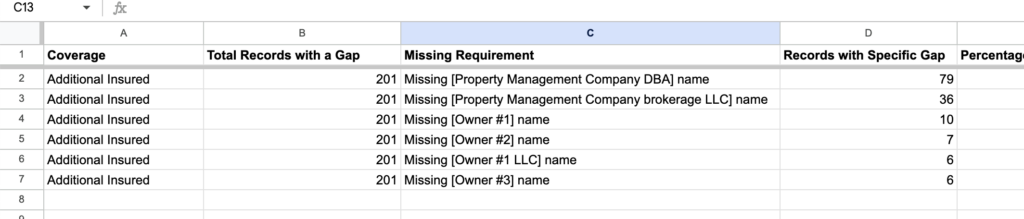

From there, she dove deeper into the breakdown of reasons for noncompliance per requirement to make her recommendations for improvement. Here’s what she found out.

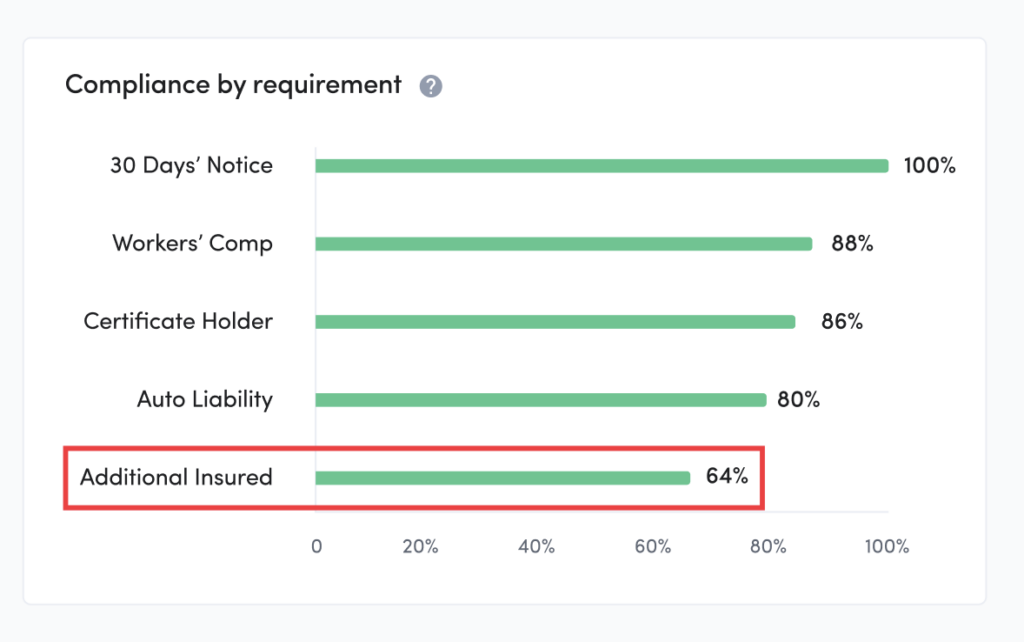

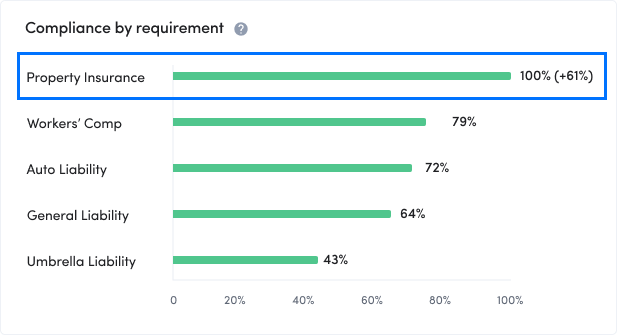

Suggestion #1: Remove Property Insurance Requirements

Jessica started with Property Insurance, which had the highest percentage of gaps. When Jessica dove into the causes for noncompliance she saw a variety of common gaps. However, the most glaring issue gap was the first one–almost half of the vendors were missing Property Insurance entirely.

Impact on Compliance:

46 percent of vendors and tenants are missing Property Insurance

Jessica’s (Director of Risk and Compliance) Suggestion:

Consider removing the Property Insurance requirement entirely.

“In some cases, real estate companies shouldn’t be that too concerned with Property Insurance for vendors because vendors are insuring their own personal property. This is exactly the case with this customer. A provision within their indemnity agreement with vendors already prevents them from subrogating the owner-operator. This makes Property Insurance unnecessary.”

—Jessica Lopes, Director of Risk and Compliance at Jones

Decision:

The compliance impact of requiring Property Insurance for vendors insurance outweighed the insurance risk it prevented, and the owner-operator’s indemnity agreement covers subrogation by vendors. With that in mind, this requirement was removed.

Results:

As soon as the Property Insurance requirement was removed, the compliance rate automatically went up to 100 percent.

Feel like this recommendation might make sense for your company? Consult with your risk team, because each real estate company has their own insurance risk tolerance. But if you are considering making a change, here’s the questions Jessica asked to help diagnose the Property Insurance issue:

- Is Property Insurance a gap for over 30 percent of your vendors?

- What insurance risk are you trying to mitigate with this coverage?

- Do you have an indemnity agreement in place with vendors?

- Does it have verbiage that prevents them from subrogating against you?

You may want to consider dropping your Property Insurance requirement if you answered yes to all these questions, but check with your risk team first.

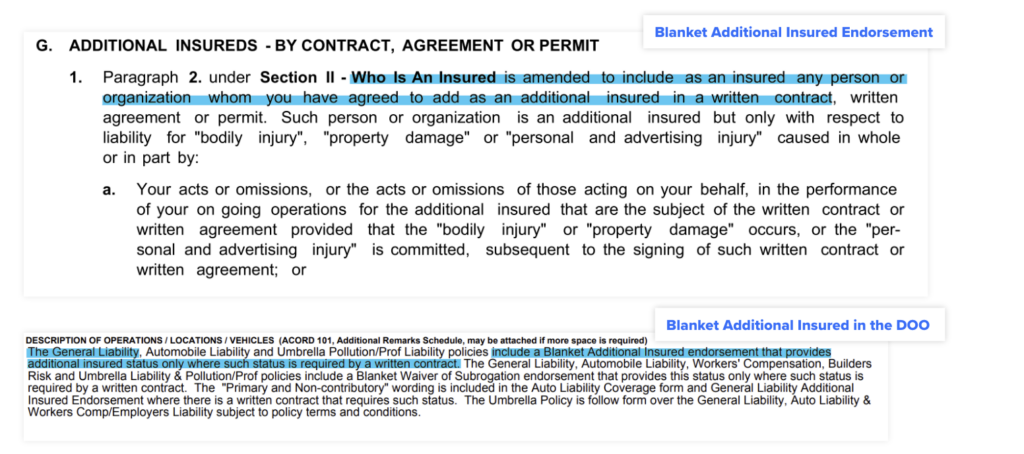

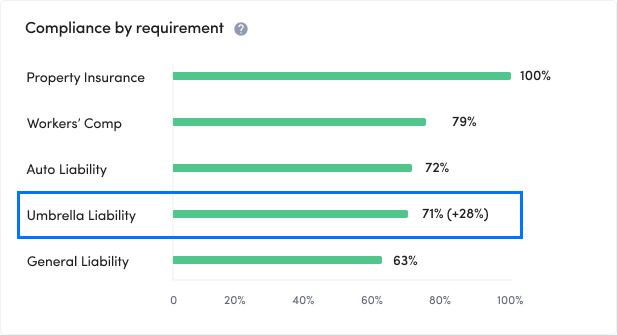

Suggestion #2: Remove Waiver of Subrogation and Primary & Noncontributory Endorsements for Umbrella Liability

Jessica turned her attention to the requirement with the second highest noncompliance rate, Umbrella Liability. She noticed two requirements with high noncompliance rates–missing Waiver of Subrogation and Primary & Noncontributory. She also noticed that inadequate aggregate limit was another frequent gap.

Impact on Compliance:

Over 50 percent of vendors and tenants missing either a Waiver of Subrogation, Primary and Noncontributory, or both for Umbrella Liability

Jessica’s Recommendation:

Retain existing Umbrella Liability limits, but remove WoS and PNC endorsement requirements.

“We typically find that Umbrella Liability is on a follow-form basis, meaning it takes on the coverage and endorsements of the policy it’s supplementing. As this company required WoS and PNC coverages for General Liability (which we highly recommend), the Umbrella Liability would take on those provisions in the event of a claim. We recommended against lowering the aggregate limit as it’s important to ensure Umbrella Liability can adequately supplement CGL and auto liability.”

-Jessica Lopes Director of Risk and Compliance at Jones

Decision:

Follow form coverage made the owner-operator drop their Waiver of Subrogation and Primary and Noncontributory requirements for Umbrella Liability.

Results:

Removing these provisions caused Umbrella Liability compliance to go up by 28 percent.

Trying to understand if a similar change could benefit your organization? Discuss these questions with your risk team:

- Do more than 50 percent of vendors not fulfill a WoS and PNC for Umbrella Liability?

- Do we require follow-form coverage for Umbrella Liability?

- Do we require WoS and PNC for general liability?

These are all factors to take into consideration when examining what you require for Umbrella Liability coverage.

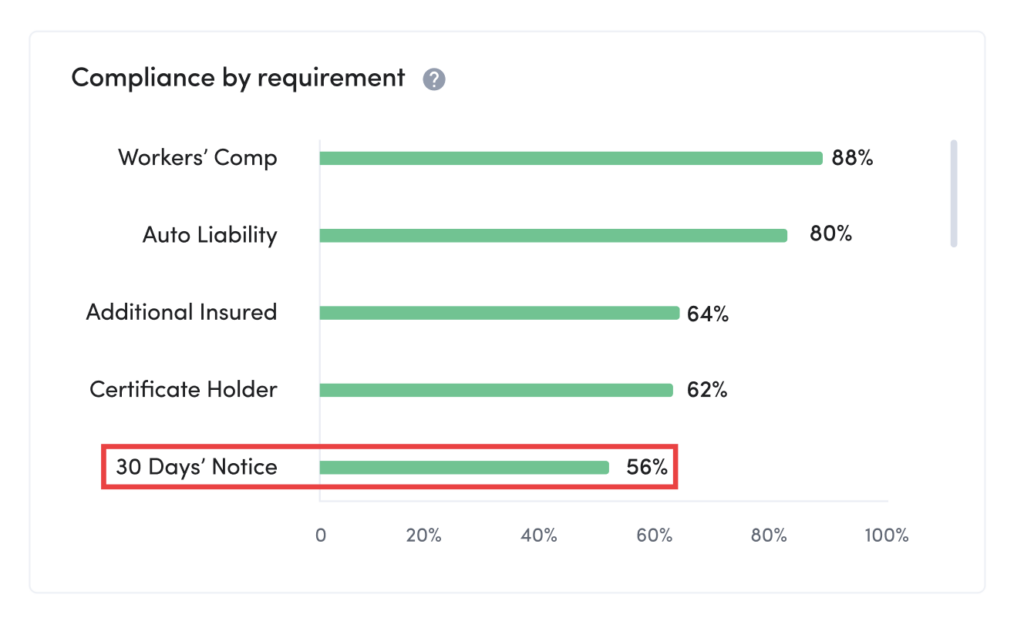

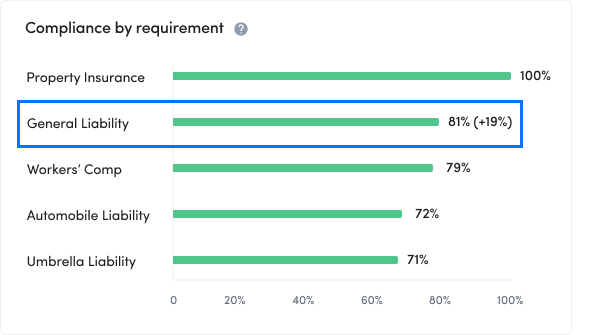

Suggestion #3: Remove 30 Days Notice of Cancellation Requirement for Commercial General Liability

When Jessica started to review common gaps for Commercial General Liability, one immediately jumped out at her—Missing 30 Days Notice of Cancellation.

Impact on Compliance:

Roughly 30 percent of vendors were missing the 30 Days Notice of Cancellation requirement for Commercial General Liability.

Jessica’s Recommendation:

Retain all other requirements, remove 30 Days Notice of Cancellation.

“30 Days Notice of Cancellation is the insurance coverage gap we see most frequently at Jones. While the purpose of this provision is to protect landlords by ensuring they’re alerted about vendor or tenant insurance policies being canceled, we see that insurers regularly fail to send out notices of cancellation. Verbiage in the cancellation endorsements often labels this service as a ‘courtesy’ and states an insurer will not be held liable should the notice not go out. With this in mind, the effort of trying to get a 30 Days Notice is often not worth it, as our coverage gap waived demonstrates.”

-Jessica Lopes, Director of Risk and Compliance at Jones

Decision:

30 Days Notice of Cancellation is rarely provided and has a high percentage of gaps, so the real estate company removed it from their requirements.

Results:

Commercial General Liability compliance went up by 18 percent.

Here’s the questions Jessica asked when diagnosing this coverage gap:=

- How frequently is the 30 Days Notice of Cancellation requirement waived?

- Is this the only coverage gap for most of your Commercial General Liability coverages?

If 30 Days Notice of Cancellation is lowering your compliance rate, dive into your data with these questions in mind.

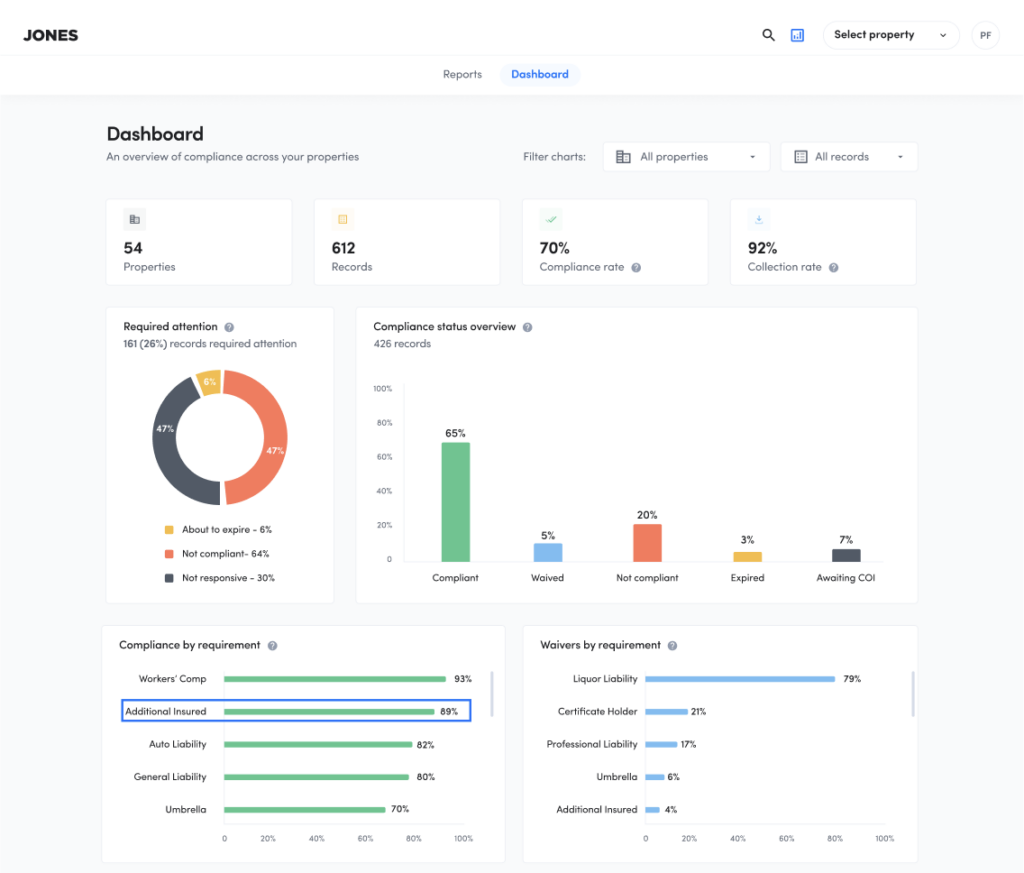

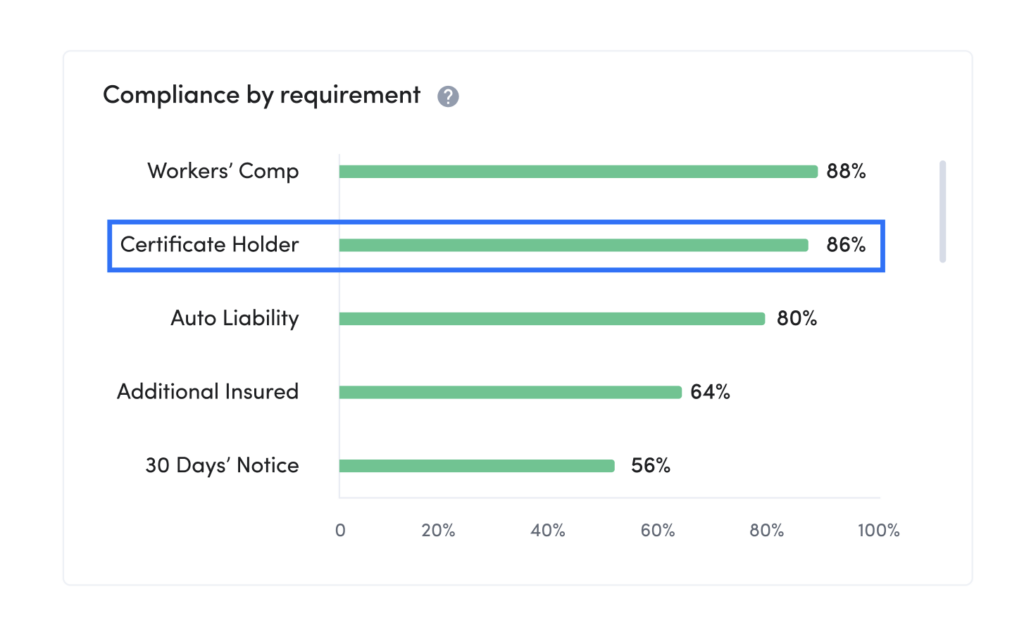

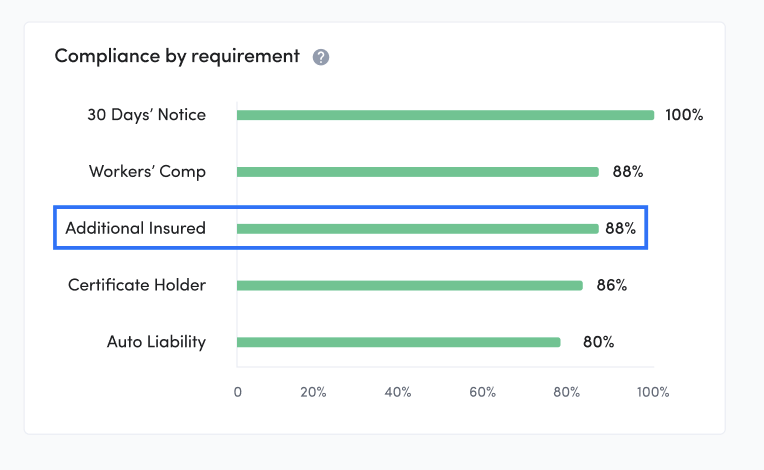

How Their Portfolio Compliance Looked After Three Changes

By eliminating three requirements that were negatively impacting their insurance compliance rates, this real estate company reduced their noncompliance by 20%. Through examining their data, and consulting with both Jones and their internal risk team, they made smart changes that reduced friction with vendors and tenants.

Interested in learning more about how Jones can help you boost compliance rates and reduce insurance risk for your portfolio? Get in touch with us via the form below to find out more.