In this guide on how to read a certificate of insurance:

—Why You Need to Know How to Read a Certificate of Insurance

—Getting Started

—Policy Basics

—Policy by Policy

—Additional Information

—Bonus: How to Read Endorsements

Why You Need to Know How to Read a Certificate of Insurance

Certificates of insurance play a pivotal role in supporting the risk transfer process. They allow you to get a comprehensive overview of a third-parties’ insurance coverages, with a variety of policies that cover the risks that come with running a business or doing work on a building. It’s important to note that the COI itself is not a copy of these insurance policies but rather a proof of insurance, given as evidence by an insurance broker that the coverages are in place at the time the COI was issued. A COI itself does not replace an insurance policy, and says right on top of the form that they are “issued as a matter of information only and confer no rights on the certificate holder.”

So, why do you have to make sure you know how to read a COI? Well, checking that your vendors and tenants have the right insurance is crucial in the event there’s an injury or lawsuit as a result of their actions or in their rented space. If the third-parties that come onto your properties to work aren’t insured, you run the risk of your organization being forced to step in and defend a claim that would otherwise be the responsibility of the vendor or tenant’s insurer. Being able to ensure that their policies meet required limits, extend coverage to all the right parties, and contain all the right types of coverage is a key part of any property manager’s job.

Let’s turn our attention to the ACORD 25 form (another name for standard COI form you’re probably used to seeing) and start unpacking the different sections.

Note: Would you rather have Jones manage the collection and review of your COIs and endorsements? Talk to our team of experts today!

How to Read a Certificate of Insurance: Getting Started

The first thing you should do when you read a certificate of insurance is check the insured name located in the box near the top left of the document.

When checking the insured name it’s crucial that the insured name matches the vendor or tenant’s name on the contract your organization signed with them. If it doesn’t exactly match, you should consult your organization’s guidelines on how to handle these cases. A completely wrong insured name could result in coverage for a claim being denied, so being specific when you check is crucial.

What if I see a DBA name on a certificate of insurance?

Some businesses use a “DBA,” or “Doing business as” name, in their outward facing business rather than their legal corporate name. There’s a variety of reasons a company may do this, but what’s important for you to know is that if the DBA matches the name in the contract you can mark it compliant.

Let’s move onto a trickier part of the review process: checking insurance policy coverages and limits.

How to Read a Certificate of Insurance: Policy Basics

Let’s go over some basic details you’ll want to review for every policy.

- Policy Number: While you won’t necessarily be able to tell much about a policy by its number, each policy should have one. You should request a new COI with a valid policy number if any policy number is TBD, Pending, Quote, or something similar.

- Effective Date: If the effective date is later than the date you are reviewing the COI, it means that the coverage is not yet effective. In this case, any claims that occurred before the effective date would not be covered.

- Expiration Date: The expiration date should not have already passed, as that would make the policy expired.

- Policy Limits: Put simply, the policy limits should be higher than or equal to the required limits in a vendor’s contract or tenant’s lease. If the limit is below what’s required, it’s not compliant.

Follow these basic guidelines for each coverage to tell if they’re compliant or not. Now we’ll look at the different coverages you’ll find evidenced on an ACORD 25.

How to Read a Certificate of Insurance: Policy by Policy

The ACORD 25 has four main structured policy sections, as well as one free text section at the bottom for other miscellaneous coverages. The first section contains details on Commercial General Liability coverage, policies that cover a lot of the standard risks that come with running a business.

Certificate of Insurance Policy #1: Commercial General Liability

When checking Commercial General Liability (CGL) coverage, you’re going to encounter a variety of terms and concepts that you might not be familiar with. One such example is the checkboxes labeled “Claims Made” and “Occur” on the left side. What do these mean? In short, claims-made policies cover claims filed within the policy period, whereas occurrence-based (what Occur is short for) policies cover incidents during the policy period, regardless of when claims are filed. These may or may not be something your company is concerned with, depending on how your leases and contracts are structured, so consult with your risk team for what to look for here.

For CGL, the most important limits for you to review are “Each Occurrence” and “General Aggregate.” “Each Occurrence” refers to the amount an insurer is willing to pay out for any one claim, whereas “General Aggregate” is the total amount an insurer will pay over the life of a policy. With that in mind, “Each Occurrence” should be higher than “General Aggregate.”

If the required limits in your vendors’ contracts or tenants’ leases aren’t met by the “Each Occurrence” and “General Aggregate” limits, the COI is not compliant. However, depending on your company’s guidelines an insufficient “General Aggregate” limit can potentially be supplemented with umbrella liability insurance (more to come later).

Certificate of Insurance Policy #2: Automobile Liability

Automobile liability insurance covers damages from any claims arising out of incidents or accidents involving vehicles. The “Combined Single Limit” is what you should look to compare your limits against when checking compliance for auto liability.

What about those checkboxes underneath automobile liability on the left? They give you crucial information about what vehicles are and aren’t covered under the automobile liability policy. Here’s what they mean:

- “Any Auto” means all categories of automobiles are covered

- “Owned Autos Only” refers to coverage for vehicles owned by the tenant or vendor’s business

- “Non-Owned Autos” refers to employees using personal vehicles for business

- “Scheduled Autos” refers to a select group of automobiles that you’ll find listed on a separate schedule form

- “Hired Autos Only” covers leased or rented vehicles

Depending on your company’s risk tolerance and requirements, some of these coverage categories may or may not be acceptable. “Any Auto” offers the widest coverage, whereas the other ones may have gaps in coverage that could result in claims. With this in mind, confirm what is acceptable with your organization’s risk management team.

Certificate of Insurance Policy #3: Umbrella/Excess Liability

Umbrella and excess liability coverages come into play when the limits set for CGL, auto liability, and Workers’ Compensation limits are exceeded as a result of a claim. In these cases, Umbrella coverage would step in to cover any shortfall. When checking umbrella for compliance, you’re going to want to compare the limits with those required in your contracts and leases.

Umbrella can also potentially come into play when covering shortfalls for additional coverages like crime, pollution, and professional liability, but make sure to discuss this with your risk team before assuming that’s the case.

Certificate of Insurance Policy #4: Workers’ Compensation

Workers’ Compensation covers an employee’s lost wages and medical expenses as a result of an injury without the need for a lawsuit. This coverage is no-fault, meaning it is paid out regardless of the circumstances of the injury.

Depending on the state you are located in, you may have some special considerations when checking Workers’ Compensation. Ohio, North Dakota, Wyoming, and Washington all require Workers’ Compensation to be purchased through a state-run fund, so if you see a private insurance company listed as the insurer you may have an issue.

While leases and contracts generally set the limits for other policies, state governments are responsible for setting Workers’ Compensation limits. If the checkbox next to the limits marked “Per Statute” has an X, it means that the coverage exceeds the state mandated amount. If not, it might be too low.

Certificate of Insurance Miscellaneous Policies

The final coverage section you’ll find on an ACORD 25 is a free text section where brokers will list out other coverages, which could include policies like Professional Liability, Crime, Pollution, or Property Insurance. Depending on the unique risk appetite of your organization and the type of work different vendors are doing, you may find some non-standard coverages evidenced in this row.

How to Read a Certificate of Insurance: Additional Information

Certificate Holder

Certificate holder can be a topic of confusion for some property managers. While it’s important to check and confirm that the certificate holder matches the one in your insurance requirements, it’s also just as important to understand that being a certificate holder confers no rights or legal status.

Additional Insured

Getting all the right Additional Insured names listed on a COI is key, as it extends the coverage from the policy to the names or entities listed. Chances are your property owner and property management company name are required to be listed as AIs, which would allow you to tender claims to a third-party insurer.

Additional Insureds are often listed in the Description of Operations section of a COI, located towards the bottom. Ensure all the entities required in your insurance requirements agreement are listed without any typos and that they were explicitly conferred Additional Insured status.

Some organizations accept Blanket Additional Insured verbiage that extends coverage to all required parties based on existing contracts or leases. You’ll have to check if this is something accepted by your organization.

Miscellaneous Coverage

You might find other assorted policy details in the Description of Operations box, or DoO. Sometimes, if there’s not enough room, brokers might add a form called ACORD 101 to give more space for this information. Look in the DOO first if you’re searching for specific provisions like a Waiver of Subrogation or Primary & Non-Contributory.

Signature

Lastly, every COI must be signed to be valid. This signature can be electronic or by hand, but if it’s not signed you shouldn’t accept it as compliant.

And with that, we’ve made our way through every section of the ACORD 25 form!

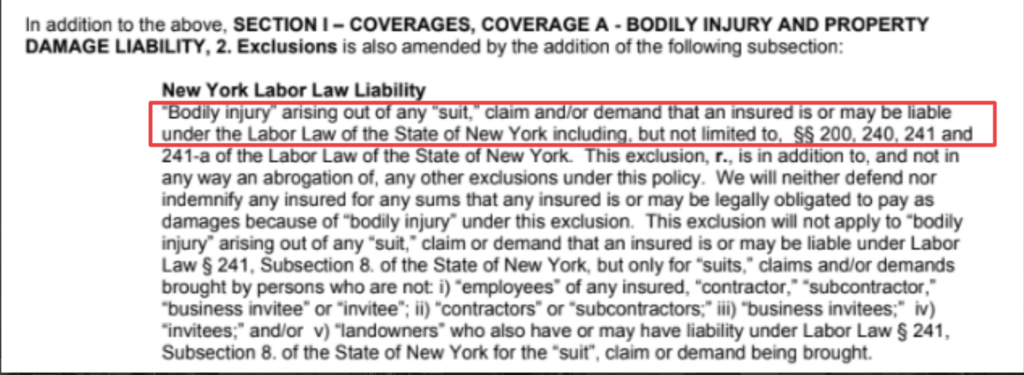

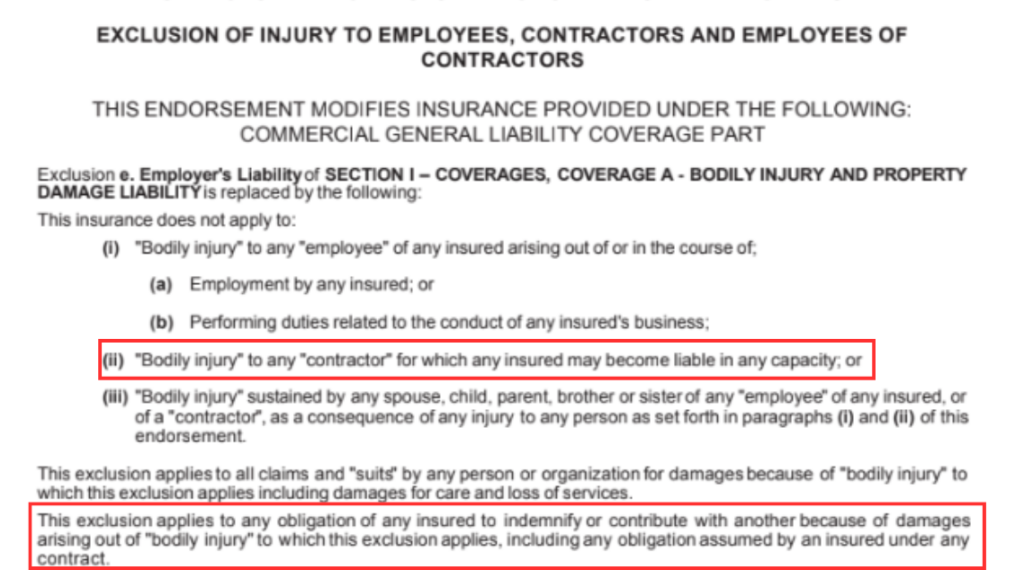

Bonus: How to Check Endorsements for Compliance

Want to learn how to go beyond just reviewing COIs for compliance? Download our comprehensive “How to Review COIs and Endorsements” blueprint for a deep dive into checking common endorsements, including:

- Waivers of Subrogation

- Primary and Noncontributory Coverage

- Additional Insured Endorsements, including schedule vs. blanket forms and ongoing and completed operations

- 30 Days Notice of Cancellation

Tired of Reviewing COIs and Endorsements Manually?

Jones automates the collection and review of COIs for property management companies, owner-operators, and general contractors across the US. Reach out to us via the form below to find out more about how Jones can help your organization manage your insurance documents.