Understand the Role of a Commercial Insurance Broker

Briefly, a commercial insurance broker is an intermediary between you (the buyer) and the insurer. Their job is to make the buying experience as seamless as possible by identifying risks and mitigating them with the appropriate coverage. In short, they are your personal policy shopper, not to be confused with insurance agents. Brokers represent the buyer, while agents represent the insurer — an essential distinction.

Insurance brokers often provide continuing education and support in benchmarking tools, market analyses, and other valuable resources. They also assist with claims, update you on noteworthy market trends, and provide policy renewal guidance.

5 Tips to Get the Most Out of Your Insurance Broker Relationship

Knowing what an insurance broker potentially offers, how do you maximize the partnership? Perks don’t typically fall in your lap, after all — few great things do. We have a few tips for getting the most out of this relationship.

1. Empower Your Insurance Broker With Information

Regardless of how savvy a commercial insurance broker is to your industry, they fly blind without essential information about your organization. Brokers aim to build customized insurance plans with your budget in mind. However, missing details about your operations, financial stability (or history), and risk management plans could derail their efforts.

Instead, empower your broker with crucial information to help them help you. Provide your broker with comprehensive data, such as:

- Financial statements

- Loss runs

- Property list

- Employees information

- Building details (i.e., dimensions)

For example, certain multifamily buildings have Federal Pacific Electric Panel Breakers aka FPE Stab Lok Panels. When that is the case, without empowering your broker with this knowledge, you may learn that your policy has a clause excluding buildings with Stab Lok panels upon either inspection or at closing.

Avoid that last-minute scenario by providing your broker with comprehensive information upfront. Equipped with this information, your broker can better find the most competitive pricing for you and the coverage you genuinely need.

2. Keep the Lines of Communication Open with Your Insurance Broker

Gone are the days when talking with your insurance broker once per year was the epitome of the relationship. Brokers take a multi-channel approach nowadays, connecting with clients on various platforms. Whether it’s an automated reminder or a quick app login to shoot a random question toward your broker, facilitate open communication.

On that note, do your part in understanding the process of buying and maintaining insurance. Sure, much of the jargon might seem foreign initially, but you don’t have to become an insurance expert to get on the same page as your broker.

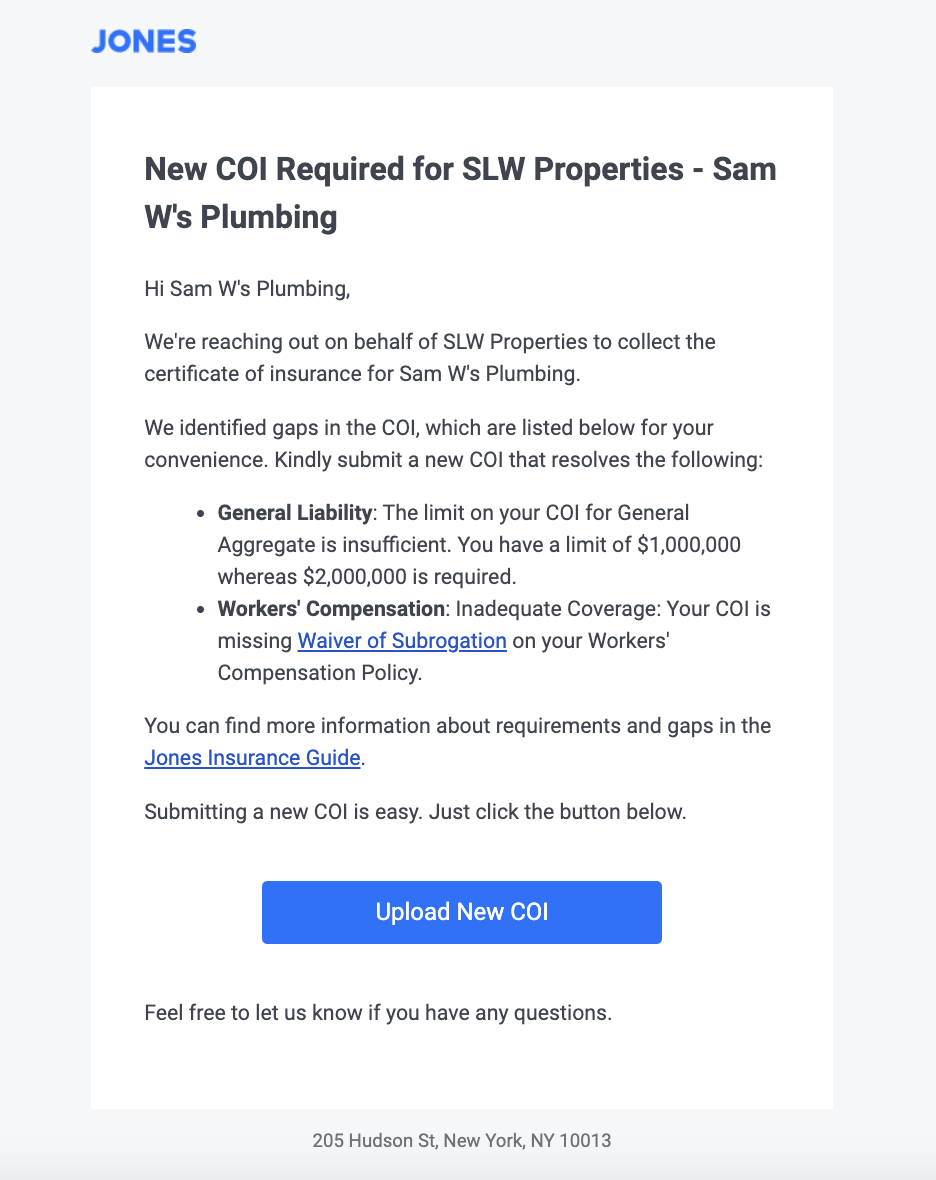

Consider learning how to navigate insurance with the Jones Insurance Guide. No longer will you be googling terms or asking Siri what something means. With a greater understanding of the insurance processes, you can amp up communication with your broker and stay more connected year-round.

3. Tap Into Your Insurance Broker’s Resources

The insurance industry is transforming from archaic operations to user-friendly digital processes. For example, artificial intelligence (AI) and machine learning in the underwriting process now streamline the entire insurance buying experience. And that’s just for starters.

Insurance brokers can now provide customized quotes much faster, giving clients access to coverage with less hassle within hours. Tap into those resources. Additionally, take advantage of your broker’s other risk management tools, from downloadable checklists to free whitepapers to easy-to-use apps.

4. Unify Your Core Goals

Effective communication goes a long way in establishing a solid working relationship with your broker, not to mention how you benefit from your broker’s well-suited policies. Although your broker might champion policy placement, remember that you are ever-growing and changing. So, your insurance needs will change, as well.

An excellent approach is to make your core values and goals well-known to your broker. For example, a prospective client had five different property insurance policies and renewal dates across their Texas multifamily real estate portfolio, and their main concern was efficiency. We brought this client to ReShield by wrapping their portfolio under a master policy with a single effective date. As a result, the renewal process was once per year, and a more efficient risk management process was in place.

Remember, brokers will base their strategy around your mission. But this endeavor must be a two-way street, and here’s why.

Many people assume that they must work with several brokers to get the most competitive rates. However, market blocking will ruin that particular strategy. This archaic tradition allows an insurance proposal to only a single broker, preventing all others from accessing that market. Engaging with more than one broker roadblocks them and prevents you from getting the best deal.

5. Trust Your Insurance Broker’s Expertise

As mentioned earlier, successful relationships are built on trust and respect. If, after your due diligence shopping for a broker, you landed on your current one, trust that you made the best decision. Also, trust them.

Second-guessing your broker’s guidance will likely cause a rift in the relationship. You might notice less engagement and a spiral down in communication. So, talk candidly about your business, and ask thoughtful questions. Of course, you want to be sure your bases are covered.

However, your broker is also invested in your business now. They will likely bend over backward to ensure your company is protected. If they don’t, it’s time to draft a broker of record letter and end the professional relationship. But while you’re on the same team, extend your trust to them.

Show Tenants Your Insurance Broker Is an Asset

It’s not uncommon for people to consider insurance folks as the “bad guys,” per se. It’s an understandable mindset since insurance is only used during times of loss. So, those negative feelings tend to trickle down onto the insurance world, including brokers.

Despite the fundamental purpose of insurance — protection from financial loss — you can shine a brighter light on your broker for tenants to see. In other words, you can show tenants how much of an asset your broker genuinely is.

For example, your broker can tailor insurance policies specifically designed to benefit you and your tenants, protecting you from financial loss. Without this innovative customization, a one-size-fits-all approach might have left you high and dry. Understanding the relationship from this angle helps tenants realize that brokers are in their corner.

Additionally, a broker’s available resources are often designed for tenants to use. Staying updated on current regulations, market trends, or weather patterns can make a risk management trifecta out of you three: client, broker, and tenants.

We encourage you to follow these tips to maximize your insurance broker relationship. Also, spotlight a broker’s helping hands. This approach encourages tenants to see them as assets and valuable strong points instead of merely the person called when something bad happens.